Is Quantum-Si (NASDAQ:QSI) In A Good Position To Invest In Growth?

Is Quantum-Si (NASDAQ:QSI) In A Good Position To Invest In Growth?

Whilst it's great to see that Quantum-Si has already begun generating revenue from operations, last year it only produced US$2.3m, so we don't think it is generating significant revenue, at this point. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. As it happens, the company's cash burn reduced by 13% over the last year, which suggests that management are maintaining a fairly steady rate of business development, albeit with a slight decrease in spending. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Whilst it's great to see that Quantum-Si has already begun generating revenue from operations, last year it only produced US$2.3m, so we don't think it is generating significant revenue, at this point. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. As it happens, the company's cash burn reduced by 13% over the last year, which suggests that management are maintaining a fairly steady rate of business development, albeit with a slight decrease in spending. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company. There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

毫無疑問,擁有不盈利企業的股份是可以賺錢的。例如,雖然軟體即服務公司Salesforce.com在多年內虧損,但其持續獲得營業收入,如果你在2005年就持有了其股份,你無疑會收穫頗豐。但嚴酷的現實是,許多虧損的公司最終會耗盡所有現金並破產。

Given this risk, we thought we'd take a look at whether Quantum-Si (NASDAQ:QSI) shareholders should be worried about its cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let's start with an examination of the business' cash, relative to its cash burn.

考慮到這一風險,我們認爲應該看看Quantum-Si(納斯達克:QSI)股東是否應該擔心其現金消耗。爲了本文的目的,現金消耗是指不盈利公司爲資助其增長而支出的現金的年率;它的負自由現金流。讓我們首先檢查一下該業務的現金情況,相對於其現金消耗。

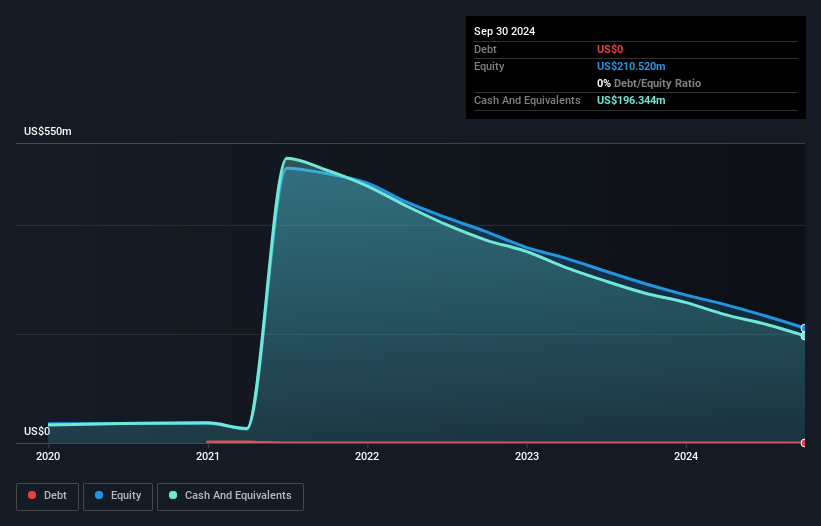

Does Quantum-Si Have A Long Cash Runway?

Quantum-Si有較長的現金運行期嗎?

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In September 2024, Quantum-Si had US$196m in cash, and was debt-free. Importantly, its cash burn was US$89m over the trailing twelve months. Therefore, from September 2024 it had 2.2 years of cash runway. That's decent, giving the company a couple years to develop its business. Depicted below, you can see how its cash holdings have changed over time.

公司的現金運行期是通過將其現金儲備除以現金消耗來計算的。到2024年9月,Quantum-Si擁有19600萬美元現金,並且沒有債務。重要的是,它在過去十二個月的現金消耗爲8900萬美元。因此,從2024年9月起,它有2.2年的現金運行期。這是不錯的,給公司提供了幾年的業務發展時間。下圖顯示了其現金持有量隨時間的變化。

How Is Quantum-Si's Cash Burn Changing Over Time?

Quantum-Si的現金消耗是如何隨時間變化的?

Whilst it's great to see that Quantum-Si has already begun generating revenue from operations, last year it only produced US$2.3m, so we don't think it is generating significant revenue, at this point. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. As it happens, the company's cash burn reduced by 13% over the last year, which suggests that management are maintaining a fairly steady rate of business development, albeit with a slight decrease in spending. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

雖然看到Quantum-Si已經開始從運營中產生營業收入是件好事,但去年它僅產生了230萬美元的收入,所以我們認爲目前它還未產生顯著的收入。因此,我們認爲關注收入增長還爲時尚早,我們將把重點限制在現金消耗如何隨時間變化上。實際上,該公司的現金消耗在過去一年減少了13%,這表明管理層保持着相對穩定的業務發展速度,儘管開支略有減少。雖然過去值得研究,但未來才最爲重要。因此,查看我們對公司的分析師預測是非常有意義的。

How Hard Would It Be For Quantum-Si To Raise More Cash For Growth?

量子硅公司在籌集更多資金以促進增長方面會有多困難?

Even though it has reduced its cash burn recently, shareholders should still consider how easy it would be for Quantum-Si to raise more cash in the future. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

儘管它最近減少了現金消耗,但股東仍應考慮量子硅在未來籌集更多現金的難易程度。 發行新股或承擔債務是上市公司爲其業務籌集更多資金的最常見方式。 通常,企業會出售新股以籌集現金並推動增長。 通過比較公司的年現金消耗與其總市值,我們可以大致估算出它需要發行多少股票,以便在同樣的消耗率下再運營一年。

Quantum-Si has a market capitalisation of US$186m and burnt through US$89m last year, which is 48% of the company's market value. From this perspective, it seems that the company spent a huge amount relative to its market value, and we'd be very wary of a painful capital raising.

量子硅的市值爲18600萬美元,去年消耗了8900萬美元,佔公司市值的48%。 從這個角度來看,似乎公司相對於其市值消耗了大量資金,我們對此次痛苦的融資會非常警惕。

Is Quantum-Si's Cash Burn A Worry?

量子硅的現金消耗是否令人擔憂?

Even though its cash burn relative to its market cap makes us a little nervous, we are compelled to mention that we thought Quantum-Si's cash runway was relatively promising. We don't think its cash burn is particularly problematic, but after considering the range of factors in this article, we do think shareholders should be monitoring how it changes over time. Separately, we looked at different risks affecting the company and spotted 3 warning signs for Quantum-Si (of which 1 can't be ignored!) you should know about.

儘管相對於市值的現金消耗讓我們有些緊張,但我們必須提到我們認爲量子硅的現金週轉相對有前景。 我們認爲其現金消耗並特別不成問題,但在考慮到本文中的各種因素後,我們確實認爲股東應當監控其隨時間的變化。 另外,我們看到了影響公司的不同風險,並發現量子硅有3個警告信號(其中1個不容忽視!)你應該知道。

Of course Quantum-Si may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

當然,量子硅可能不是最佳的買入股票。因此,您可能希望查看這份擁有高股本回報率公司的免費集合,或這份高內部人持股的股票名單。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?對內容有疑慮?請直接與我們聯繫。或者,發送電子郵件至 editorial-team (at) simplywallst.com。

這篇來自Simply Wall ST的文章是一般性的。我們根據歷史數據和分析師預測提供評論,採用無偏見的方法,我們的文章並不旨在提供財務建議。它不構成對任何股票的買入或賣出建議,也未考慮到您的目標或財務狀況。我們旨在爲您提供以基本數據驅動的長期分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall ST在提到的任何股票中均沒有持倉。

譯文內容由第三人軟體翻譯。