Is T-Mobile US, Inc.'s (NASDAQ:TMUS) 16% ROE Better Than Average?

Is T-Mobile US, Inc.'s (NASDAQ:TMUS) 16% ROE Better Than Average?

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity Many investors are still learning about the various metrics that can be useful when analysing a stock. This article is for those who would like to learn about Return On Equity (ROE). To keep the lesson grounded in practicality, we'll use ROE to better understand T-Mobile US, Inc. (NASDAQ:TMUS).

許多投資者仍在學習分析股票時的各種指標。本文爲那些想要了解股東權益回報率(ROE)的人準備。爲了保持課堂的實用性,我們將使用ROE來更好地理解T-Mobile US, Inc.(納斯達克:TMUS)。

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors' money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

股本回報率(ROE)是衡量公司如何有效地增長其價值和管理投資者資金的指標。簡單來說,它衡量公司的盈利能力相對於股東權益的情況。

How Is ROE Calculated?

淨資產收益率怎麼計算?

The formula for ROE is:

ROE的公式是:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

股東權益回報率 = 凈利潤(來自持續運營)÷ 股東權益

So, based on the above formula, the ROE for T-Mobile US is:

因此,根據上述公式,T-Mobile US的ROE爲:

16% = US$10b ÷ US$64b (Based on the trailing twelve months to September 2024).

16% = 100億美元 ÷ 640億美元(基於截至2024年9月的過去十二個月)。

The 'return' refers to a company's earnings over the last year. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.16 in profit.

「回報」是指公司在過去一年中的收益。可以這樣理解:對於每1美元的股東資本,公司的利潤爲0.16美元。

Does T-Mobile US Have A Good ROE?

T-Mobile US的ROE好嗎?

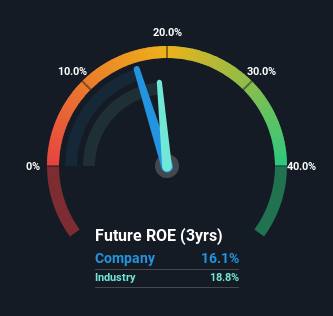

Arguably the easiest way to assess company's ROE is to compare it with the average in its industry. The limitation of this approach is that some companies are quite different from others, even within the same industry classification. If you look at the image below, you can see T-Mobile US has a similar ROE to the average in the Wireless Telecom industry classification (19%).

評估公司的ROE最簡單的方法無疑是將其與行業的平均水平進行比較。 這種方法的侷限性在於,有些公司雖然在同一行業分類中但彼此差異很大。 如果你查看下面的圖片,你會看到T-Mobile US的ROE與無線電信行業分類的平均水平相似(19%)。

So while the ROE is not exceptional, at least its acceptable. Even if the ROE is respectable when compared to the industry, its worth checking if the firm's ROE is being aided by high debt levels. If a company takes on too much debt, it is at higher risk of defaulting on interest payments. You can see the 2 risks we have identified for T-Mobile US by visiting our risks dashboard for free on our platform here.

因此,儘管ROE並不特別優秀,但至少還是可以接受的。 即使與行業相比ROE還算可以,但值得檢查一下公司的ROE是否受到高債務水平的影響。如果一家公司承擔過多的債務,它就面臨更高的未能支付利息的風險。 你可以查看我們爲T-Mobile US確定的兩種風險,免費訪問我們的風險儀表板,點擊這裏就能在我們的平台上看到。

The Importance Of Debt To Return On Equity

債務對淨資產收益率的重要性

Virtually all companies need money to invest in the business, to grow profits. The cash for investment can come from prior year profits (retained earnings), issuing new shares, or borrowing. In the first two cases, the ROE will capture this use of capital to grow. In the latter case, the debt required for growth will boost returns, but will not impact the shareholders' equity. In this manner the use of debt will boost ROE, even though the core economics of the business stay the same.

幾乎所有公司都需要資金來投資於業務,以實現利潤增長。 投資的資金可以來自前年的利潤(留存收益),發行新股,或者借款。在前兩種情況下,ROE將反映這種資本使用來實現增長。 在後者情況下,所需的增長債務將提高回報,但不會影響股東權益。 這樣使用債務就會提高ROE,即使業務的核心經濟狀況保持不變。

T-Mobile US' Debt And Its 16% ROE

T-Mobile US的債務和16%的ROE

T-Mobile US does use a high amount of debt to increase returns. It has a debt to equity ratio of 1.25. While its ROE is respectable, it is worth keeping in mind that there is usually a limit as to how much debt a company can use. Debt increases risk and reduces options for the company in the future, so you generally want to see some good returns from using it.

T-Mobile US確實使用大量債務來增加收益。它的債務與股本比率爲1.25。雖然它的ROE很可觀,但值得注意的是,通常公司可以使用的債務是有上限的。債務增加了風險,並減少了未來公司的選擇,因此通常希望看到使用債務能帶來良好的收益。

Conclusion

結論

Return on equity is one way we can compare its business quality of different companies. Companies that can achieve high returns on equity without too much debt are generally of good quality. If two companies have the same ROE, then I would generally prefer the one with less debt.

股東權益回報率是我們比較不同公司業務質量的一種方式。能夠在不借太多債務的情況下實現高股東權益回報率的公司通常質量不錯。如果兩家公司有相同的ROE,我通常會更傾向於選擇債務較少的那一家公司。

Having said that, while ROE is a useful indicator of business quality, you'll have to look at a whole range of factors to determine the right price to buy a stock. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So you might want to take a peek at this data-rich interactive graph of forecasts for the company.

話雖如此,儘管ROE是評估企業質量的有用指標,但要判斷買入股票的正確價格,你還需要考慮一系列因素。利潤增長率與股票價格中反映的預期相比特別重要。因此,你可能想看看這幅富含數據的公司預測交互式圖表。

If you would prefer check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

如果你更願意查看另一家公司——一家潛在的財務狀況優秀的公司——那麼一定不要錯過這份有趣公司的免費列表,這些公司有高股本回報率和低負債。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?對內容有疑慮?請直接與我們聯繫。或者,發送電子郵件至 editorial-team (at) simplywallst.com。

這篇來自Simply Wall ST的文章是一般性的。我們根據歷史數據和分析師預測提供評論,採用無偏見的方法,我們的文章並不旨在提供財務建議。它不構成對任何股票的買入或賣出建議,也未考慮到您的目標或財務狀況。我們旨在爲您提供以基本數據驅動的長期分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall ST在提到的任何股票中均沒有持倉。

譯文內容由第三人軟體翻譯。