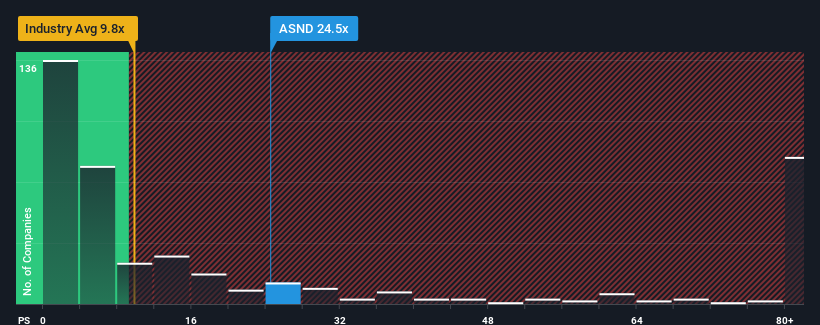

You may think that with a price-to-sales (or "P/S") ratio of 24.5x Ascendis Pharma A/S (NASDAQ:ASND) is a stock to avoid completely, seeing as almost half of all the Biotechs companies in the United States have P/S ratios under 9.8x and even P/S lower than 3x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

NasdaqGS:ASND Price to Sales Ratio vs Industry December 24th 2024

How Ascendis Pharma Has Been Performing

With revenue growth that's inferior to most other companies of late, Ascendis Pharma has been relatively sluggish. Perhaps the market is expecting future revenue performance to undergo a reversal of fortunes, which has elevated the P/S ratio. If not, then existing shareholders may be very nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Ascendis Pharma will help you uncover what's on the horizon.

Is There Enough Revenue Growth Forecasted For Ascendis Pharma?

The only time you'd be truly comfortable seeing a P/S as steep as Ascendis Pharma's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, we see that the company grew revenue by an impressive 116% last year. This great performance means it was also able to deliver immense revenue growth over the last three years. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 62% per annum as estimated by the analysts watching the company. That's shaping up to be materially lower than the 115% per year growth forecast for the broader industry.

With this in consideration, we believe it doesn't make sense that Ascendis Pharma's P/S is outpacing its industry peers. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What We Can Learn From Ascendis Pharma's P/S?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

It comes as a surprise to see Ascendis Pharma trade at such a high P/S given the revenue forecasts look less than stellar. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Having said that, be aware Ascendis Pharma is showing 2 warning signs in our investment analysis, and 1 of those is potentially serious.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company grew revenue by an impressive 116% last year. This great performance means it was also able to deliver immense revenue growth over the last three years. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Taking a look back first, we see that the company grew revenue by an impressive 116% last year. This great performance means it was also able to deliver immense revenue growth over the last three years. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

首先回顧一下,我們看到公司去年的營業收入增長了令人印象深刻的116%。這出色的表現也意味着它在過去三年中實現了巨大的營業收入增長。所以我們可以開始確認,公司在這段時間內在營業收入的增長上做得非常出色。

首先回顧一下,我們看到公司去年的營業收入增長了令人印象深刻的116%。這出色的表現也意味着它在過去三年中實現了巨大的營業收入增長。所以我們可以開始確認,公司在這段時間內在營業收入的增長上做得非常出色。