HealthEquity, Inc.'s (NASDAQ:HQY) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

HealthEquity, Inc.'s (NASDAQ:HQY) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity Most readers would already be aware that HealthEquity's (NASDAQ:HQY) stock increased significantly by 20% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. Specifically, we decided to study HealthEquity's ROE in this article.

大多數讀者應該已經知道,HealthEquity(納斯達克:HQY)的股票在過去三個月內顯著上漲了20%。鑑於股票價格通常與公司的長期財務表現保持一致,我們決定更深入地研究其財務指標,以查看它們是否在最近的價格變動中發揮了作用。 具體來說,我們決定在本文中研究HealthEquity的ROE。

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

股東需要考慮的一個重要因素是股本回報率或ROE,因爲它告訴他們資本是如何有效地再投資的。換句話說,它是一個盈利能力比率,衡量公司股東提供的資本的回報率。

How Is ROE Calculated?

淨資產收益率怎麼計算?

The formula for return on equity is:

股東權益回報率的公式是:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

股東權益回報率 = 凈利潤(來自持續運營)÷ 股東權益

So, based on the above formula, the ROE for HealthEquity is:

因此,根據上述公式,HealthEquity的ROE爲:

4.6% = US$97m ÷ US$2.1b (Based on the trailing twelve months to October 2024).

4.6% = 9700萬美元 ÷ 21億(基於截至2024年10月的過去十二個月)。

The 'return' refers to a company's earnings over the last year. So, this means that for every $1 of its shareholder's investments, the company generates a profit of $0.05.

「收益」指的是公司過去一年的盈利。因此,這意味着每投資1美元,公司的利潤爲0.05美元。

Why Is ROE Important For Earnings Growth?

ROE爲什麼對凈利潤增長很重要?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company's earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

到目前爲止,我們已經了解到ROE是衡量公司盈利能力的一個指標。根據公司將這些利潤再投資或「保留」的比例,以及其有效性,我們能夠評估公司的盈利增長潛力。在其他條件相同的情況下,與沒有相同特徵的公司相比,具有更高股本回報率和更高利潤保留的公司通常具有更高的增長率。

HealthEquity's Earnings Growth And 4.6% ROE

HealthEquity的盈利增長和4.6%的ROE

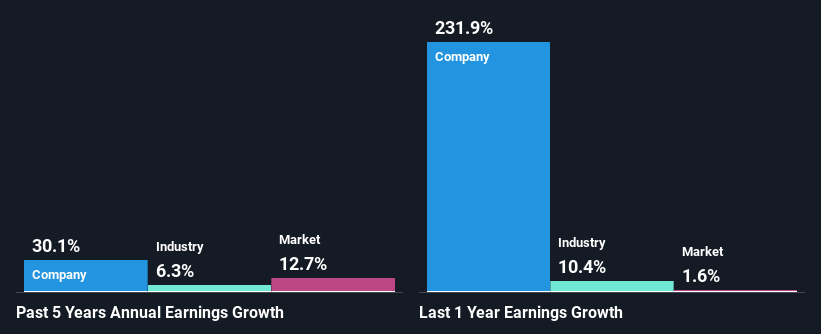

It is hard to argue that HealthEquity's ROE is much good in and of itself. Even when compared to the industry average of 13%, the ROE figure is pretty disappointing. However, we we're pleasantly surprised to see that HealthEquity grew its net income at a significant rate of 30% in the last five years. Therefore, there could be other reasons behind this growth. For instance, the company has a low payout ratio or is being managed efficiently.

很難爭辯HealthEquity的ROE本身就很好。即使與行業平均的13%相比,ROE數字也讓人失望。然而,我們欣喜地發現,HealthEquity在過去五年中,其凈利潤以30%的顯著速度增長。因此,這種增長背後可能還有其他原因。例如,公司有低的分紅派息率或管理效率高。

As a next step, we compared HealthEquity's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 6.3%.

作爲下一步,我們將HealthEquity的凈利潤增長與行業進行了比較,令人高興的是,我們發現公司的增長高於行業平均增長的6.3%。

Earnings growth is an important metric to consider when valuing a stock. It's important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Has the market priced in the future outlook for HQY? You can find out in our latest intrinsic value infographic research report.

盈利增長是評估股票時一個重要的指標。投資者需要了解市場是否已經考慮到公司的預期盈利增長(或下降)。這將幫助他們判斷該股票未來是光明還是黯淡。市場是否已經考慮到HQY的未來展望?您可以在我們的最新內在價值信息圖研究報告中找到答案。

Is HealthEquity Making Efficient Use Of Its Profits?

HealthEquity是否有效利用了其利潤?

Given that HealthEquity doesn't pay any regular dividends to its shareholders, we infer that the company has been reinvesting all of its profits to grow its business.

考慮到HealthEquity並未向其股東支付任何定期分紅,我們可以推斷該公司一直在將所有利潤用於再投資以壯大業務。

Conclusion

結論

In total, it does look like HealthEquity has some positive aspects to its business. With a high rate of reinvestment, albeit at a low ROE, the company has managed to see a considerable growth in its earnings. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

總體來看,HealthEquity的業務確實有一些積極的方面。儘管ROE較低,但憑藉高再投資率,公司已經實現了可觀的盈利增長。儘管如此,最新的分析師預測顯示該公司將繼續實現盈利擴張。這些分析師的預期是基於行業的廣泛期望,還是基於公司的基本面?請點擊這裏訪問我們分析師關於該公司的預測頁面。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?對內容有疑慮?請直接與我們聯繫。或者,發送電子郵件至 editorial-team (at) simplywallst.com。

這篇來自Simply Wall ST的文章是一般性的。我們根據歷史數據和分析師預測提供評論,採用無偏見的方法,我們的文章並不旨在提供財務建議。它不構成對任何股票的買入或賣出建議,也未考慮到您的目標或財務狀況。我們旨在爲您提供以基本數據驅動的長期分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall ST在提到的任何股票中均沒有持倉。

譯文內容由第三人軟體翻譯。