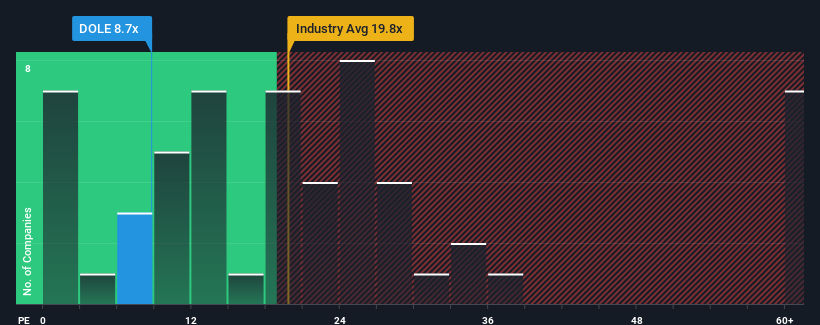

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") above 19x, you may consider Dole plc (NYSE:DOLE) as a highly attractive investment with its 8.7x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

There hasn't been much to differentiate Dole's and the market's earnings growth lately. It might be that many expect the mediocre earnings performance to degrade, which has repressed the P/E. If not, then existing shareholders have reason to be optimistic about the future direction of the share price.

NYSE:DOLE Price to Earnings Ratio vs Industry December 23rd 2024 Keen to find out how analysts think Dole's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Any Growth For Dole?

The only time you'd be truly comfortable seeing a P/E as depressed as Dole's is when the company's growth is on track to lag the market decidedly.

If we review the last year of earnings growth, the company posted a worthy increase of 3.0%. Pleasingly, EPS has also lifted 230% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Turning to the outlook, the next year should bring diminished returns, with earnings decreasing 10% as estimated by the three analysts watching the company. Meanwhile, the broader market is forecast to expand by 15%, which paints a poor picture.

In light of this, it's understandable that Dole's P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From Dole's P/E?

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Dole maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Dole (1 is a bit unpleasant) you should be aware of.

If these risks are making you reconsider your opinion on Dole, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?擔心內容嗎?直接聯繫我們。或者,發送電子郵件給編輯組(網址爲)simplywallst.com。 Simply Wall ST 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

If we review the last year of earnings growth, the company posted a worthy increase of 3.0%. Pleasingly, EPS has also lifted 230% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

If we review the last year of earnings growth, the company posted a worthy increase of 3.0%. Pleasingly, EPS has also lifted 230% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

如果我們回顧一下去年的收益增長,該公司公佈了3.0%的可觀增長。令人高興的是,每股收益也比三年前增長了230%,這在一定程度上要歸功於過去12個月的增長。因此,我們可以首先確認該公司在這段時間內在增加收益方面做得很好。

如果我們回顧一下去年的收益增長,該公司公佈了3.0%的可觀增長。令人高興的是,每股收益也比三年前增長了230%,這在一定程度上要歸功於過去12個月的增長。因此,我們可以首先確認該公司在這段時間內在增加收益方面做得很好。