We Think FLEX LNG (NYSE:FLNG) Is Taking Some Risk With Its Debt

We Think FLEX LNG (NYSE:FLNG) Is Taking Some Risk With Its Debt

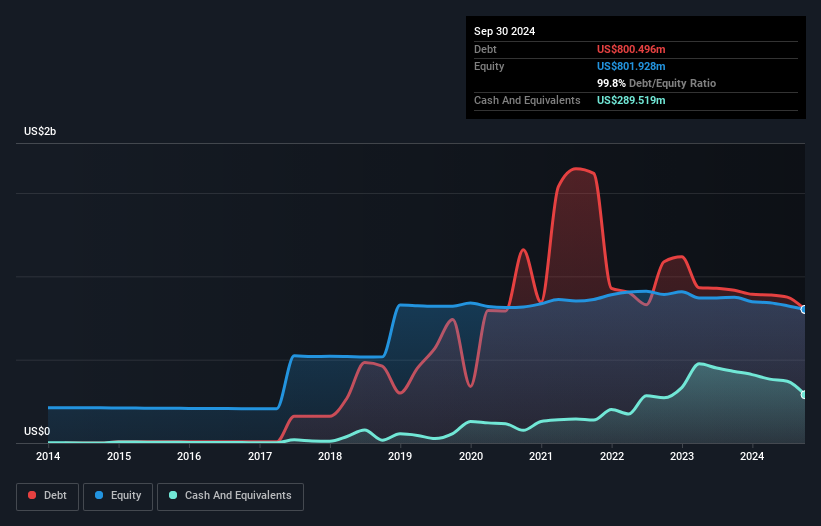

The latest balance sheet data shows that FLEX LNG had liabilities of US$150.1m due within a year, and liabilities of US$1.58b falling due after that. Offsetting these obligations, it had cash of US$289.5m as well as receivables valued at US$28.1m due within 12 months. So it has liabilities totalling US$1.41b more than its cash and near-term receivables, combined.

The latest balance sheet data shows that FLEX LNG had liabilities of US$150.1m due within a year, and liabilities of US$1.58b falling due after that. Offsetting these obligations, it had cash of US$289.5m as well as receivables valued at US$28.1m due within 12 months. So it has liabilities totalling US$1.41b more than its cash and near-term receivables, combined. Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, FLEX LNG Ltd. (NYSE:FLNG) does carry debt. But is this debt a concern to shareholders?

禾倫·巴菲特曾 famously表示:'波動性遠非風險的同義詞。' 當我們考慮一家公司有多大風險時,我們總是喜歡查看其債務的使用情況,因爲債務負擔過重可能導致毀滅。 重要的是,Flex LNG Ltd. (紐交所:FLNG) 確實有債務。 但這筆債務對股東來說是個問題嗎?

Why Does Debt Bring Risk?

爲什麼債務帶來風險?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

債務是幫助企業成長的工具,但如果企業無法償還其債權人,那麼它就只能任人擺佈。 在最壞的情況下,如果公司無法支付其債權人,它可能會破產。然而,更常見(但仍然代價高昂)的情況是,公司只爲控制債務而必須以低廉的股價稀釋股東。 然而,通過替代稀釋,債務對於那些需要資本以高回報率投資於增長的企業來說,可以是極好的工具。 在我們審查債務水平時,首先考慮現金和債務水平。

What Is FLEX LNG's Debt?

Flex LNG的債務是多少?

As you can see below, FLEX LNG had US$800.5m of debt at September 2024, down from US$916.2m a year prior. However, because it has a cash reserve of US$289.5m, its net debt is less, at about US$511.0m.

如您所見,Flex LNG在2024年9月的債務爲80050萬美元,低於一年前的91620萬美元。 然而,由於它有28950萬美元的現金儲備,其淨債務更少,約爲51100萬美元。

How Healthy Is FLEX LNG's Balance Sheet?

Flex LNG的資產負債表健康狀況如何?

The latest balance sheet data shows that FLEX LNG had liabilities of US$150.1m due within a year, and liabilities of US$1.58b falling due after that. Offsetting these obligations, it had cash of US$289.5m as well as receivables valued at US$28.1m due within 12 months. So it has liabilities totalling US$1.41b more than its cash and near-term receivables, combined.

最新的資產負債表數據顯示,Flex LNG在一年內有15010萬美元的負債,而在此之後則有15.8億美元的負債。抵消這些義務後,它有現金28950萬美元以及在12個月內到期的應收賬款價值爲2810萬美元。因此,它的負債總額比現金和短期應收款加起來多出14.1億美元。

Given this deficit is actually higher than the company's market capitalization of US$1.14b, we think shareholders really should watch FLEX LNG's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

鑑於這一赤字實際上高於公司11.4億美元的市場資本化,我們認爲股東確實應該關注Flex LNG的債務水平,就像家長第一次看着自己的孩子騎自行車一樣。在這種情況下,如果公司不得不快速清理其資產負債表,似乎股東將遭受嚴重稀釋。

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

我們通過查看公司的淨負債與息稅折舊攤銷前利潤(EBITDA)的比例來衡量公司相對於其收益能力的債務負擔,以及計算其息稅前利潤(EBIT)覆蓋利息支出的能力(利息覆蓋率)。因此,我們在考慮收益時同時考慮了折舊與攤銷費用及不考慮這些費用的情況。

Even though FLEX LNG's debt is only 1.9, its interest cover is really very low at 1.8. This does have us wondering if the company pays high interest because it is considered risky. In any case, it's safe to say the company has meaningful debt. Sadly, FLEX LNG's EBIT actually dropped 6.7% in the last year. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine FLEX LNG's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

儘管Flex LNG的債務僅爲1.9,但其利息覆蓋率非常低,僅爲1.8。這讓我們懷疑公司是否因爲被認爲風險較高而支付高利息。無論如何,可以肯定的是,這家公司有相當的債務。可悲的是,Flex LNG的EBIT在去年實際上下降了6.7%。如果收益繼續下降,那麼管理這些債務將像騎獨輪車送熱湯一樣困難。在分析債務水平時,資產負債表顯然是一個明顯的起點。但未來的收益,更多的是,將判斷Flex LNG未來維持健康資產負債表的能力。因此,如果你想看看專業人士的看法,你可能會發現這個關於分析師利潤預測的免費報告很有趣。

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, FLEX LNG generated free cash flow amounting to a very robust 94% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

最後,一家公司只能用現金償還債務,而不是會計利潤。因此,邏輯上的步驟是查看EBIT與實際自由現金流的匹配比例。在過去三年中,Flex LNG的自由現金流佔其EBIT的比例高達94%,超過我們的預期。這使其處於償還債務的非常強大位置。

Our View

我們的觀點

On the face of it, FLEX LNG's level of total liabilities left us tentative about the stock, and its interest cover was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making FLEX LNG stock a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 3 warning signs for FLEX LNG (1 is significant) you should be aware of.

乍一看,Flex LNG 的總負債水平讓我們對該股票感到猶豫,且其利息覆蓋率並不比一年中最繁忙夜晚的唯一一家空餐廳更具吸引力。但從積極的一面看,它將EBIT轉化爲自由現金流的能力是一個好兆頭,這讓我們更加樂觀。考慮到資產負債表和所有這些因素,我們確實認爲債務讓 Flex LNG 的股票有些風險。這並不一定是壞事,但一般來說,我們會更願意看到更少的槓桿。資產負債表顯然是分析債務時需要關注的領域。但最終,每家公司都可能存在資產負債表之外的風險。例如,我們已確定 Flex LNG 有 3 個警示信號(其中 1 個非常重要),您應當注意。

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

無論最終結果如何,有時候更容易關注那些根本不需要債務的公司。讀者可以立即免費獲取一份淨債務爲零的成長股列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?對內容有疑慮?請直接與我們聯繫。或者,發送電子郵件至 editorial-team (at) simplywallst.com。

這篇來自Simply Wall ST的文章是一般性的。我們根據歷史數據和分析師預測提供評論,採用無偏見的方法,我們的文章並不旨在提供財務建議。它不構成對任何股票的買入或賣出建議,也未考慮到您的目標或財務狀況。我們旨在爲您提供以基本數據驅動的長期分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall ST在提到的任何股票中均沒有持倉。

譯文內容由第三人軟體翻譯。