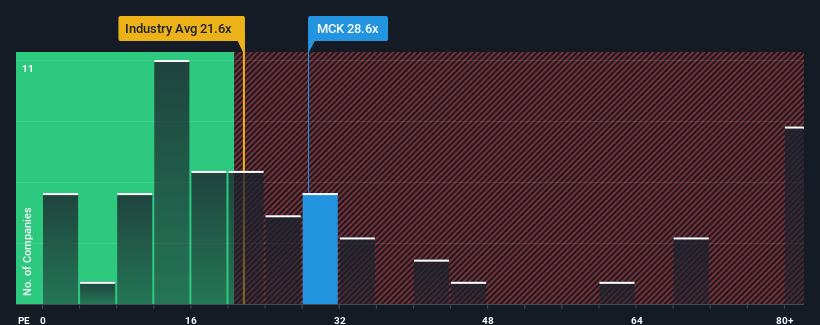

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 18x, you may consider McKesson Corporation (NYSE:MCK) as a stock to avoid entirely with its 28.6x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

While the market has experienced earnings growth lately, McKesson's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

NYSE:MCK Price to Earnings Ratio vs Industry December 19th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on McKesson.

Does Growth Match The High P/E?

In order to justify its P/E ratio, McKesson would need to produce outstanding growth well in excess of the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 24%. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 28% each year during the coming three years according to the analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 11% per annum, which is noticeably less attractive.

In light of this, it's understandable that McKesson's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On McKesson's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of McKesson's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with McKesson, and understanding them should be part of your investment process.

If these risks are making you reconsider your opinion on McKesson, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 24%. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 24%. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

回顧一下,公司的每股收益增長去年並沒有令人興奮,出現了令人失望的24%的下降。這抹去了過去三年中的任何增益,實際上的每股收益總的來說幾乎沒有變化。因此,我們認爲公司在這段時間內的盈利增長結果表現得相當混合。

回顧一下,公司的每股收益增長去年並沒有令人興奮,出現了令人失望的24%的下降。這抹去了過去三年中的任何增益,實際上的每股收益總的來說幾乎沒有變化。因此,我們認爲公司在這段時間內的盈利增長結果表現得相當混合。