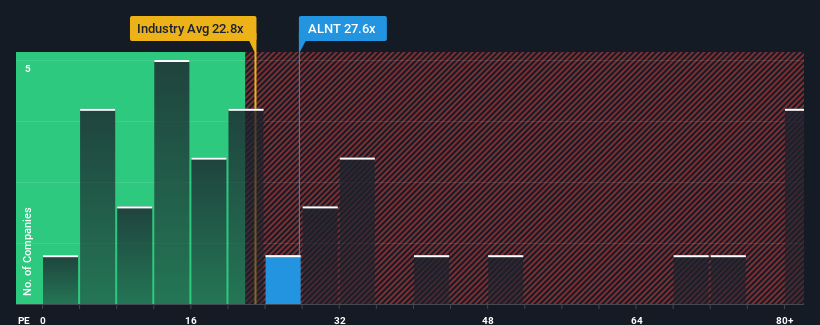

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 18x, you may consider Allient Inc. (NASDAQ:ALNT) as a stock to avoid entirely with its 27.6x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Allient could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

NasdaqGM:ALNT Price to Earnings Ratio vs Industry December 19th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Allient.

Is There Enough Growth For Allient?

The only time you'd be truly comfortable seeing a P/E as steep as Allient's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 40% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 51% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 29% each year during the coming three years according to the three analysts following the company. With the market only predicted to deliver 11% per year, the company is positioned for a stronger earnings result.

With this information, we can see why Allient is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Allient's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you take the next step, you should know about the 3 warning signs for Allient (1 is significant!) that we have uncovered.

Of course, you might also be able to find a better stock than Allient. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a frustrating 40% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 51% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Retrospectively, the last year delivered a frustrating 40% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 51% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

回顧過去,去年公司的淨利潤下降了令人失望的40%。最近三年情況也不樂觀,公司的每股收益整體減少了51%。因此,不幸的是,我們不得不承認公司在這段時間內未能有效地提高盈利能力。

回顧過去,去年公司的淨利潤下降了令人失望的40%。最近三年情況也不樂觀,公司的每股收益整體減少了51%。因此,不幸的是,我們不得不承認公司在這段時間內未能有效地提高盈利能力。