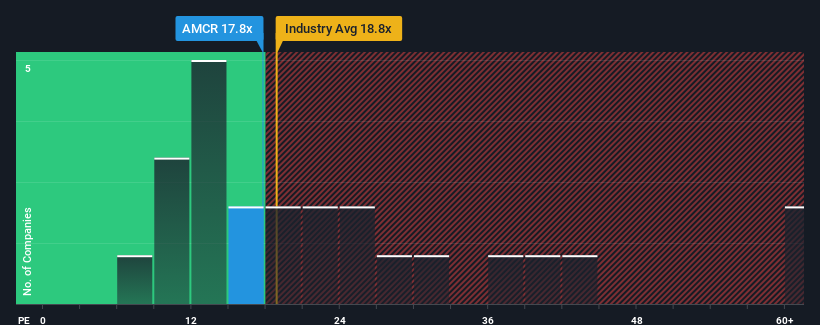

There wouldn't be many who think Amcor plc's (NYSE:AMCR) price-to-earnings (or "P/E") ratio of 17.8x is worth a mention when the median P/E in the United States is similar at about 18x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

While the market has experienced earnings growth lately, Amcor's earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

NYSE:AMCR Price to Earnings Ratio vs Industry December 19th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Amcor.

What Are Growth Metrics Telling Us About The P/E?

The only time you'd be comfortable seeing a P/E like Amcor's is when the company's growth is tracking the market closely.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 19%. As a result, earnings from three years ago have also fallen 13% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 12% per year during the coming three years according to the analysts following the company. With the market predicted to deliver 11% growth per year, the company is positioned for a comparable earnings result.

In light of this, it's understandable that Amcor's P/E sits in line with the majority of other companies. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Bottom Line On Amcor's P/E

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Amcor's analyst forecasts revealed that its market-matching earnings outlook is contributing to its current P/E. At this stage investors feel the potential for an improvement or deterioration in earnings isn't great enough to justify a high or low P/E ratio. It's hard to see the share price moving strongly in either direction in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Amcor that you should be aware of.

If you're unsure about the strength of Amcor's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 19%. As a result, earnings from three years ago have also fallen 13% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 19%. As a result, earnings from three years ago have also fallen 13% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

回顧一下,公司的每股收益增長在去年並沒有什麼令人興奮的表現,出現了令人失望的19%的下降。因此,三年前的收益總體上也下降了13%。因此,可以合理地說,公司最近的收益增長並不理想。

回顧一下,公司的每股收益增長在去年並沒有什麼令人興奮的表現,出現了令人失望的19%的下降。因此,三年前的收益總體上也下降了13%。因此,可以合理地說,公司最近的收益增長並不理想。