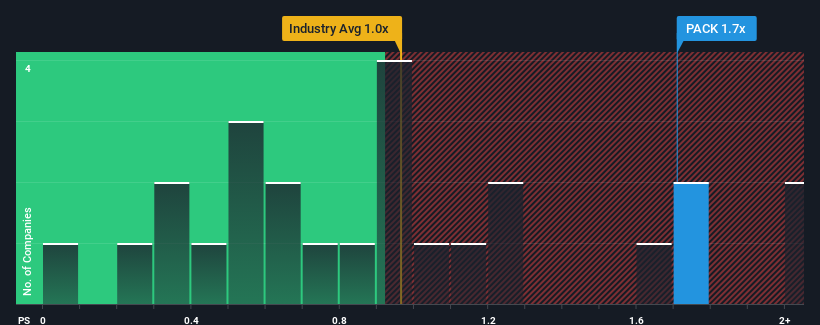

When close to half the companies in the Packaging industry in the United States have price-to-sales ratios (or "P/S") below 0.9x, you may consider Ranpak Holdings Corp. (NYSE:PACK) as a stock to potentially avoid with its 1.7x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

NYSE:PACK Price to Sales Ratio vs Industry December 19th 2024

How Has Ranpak Holdings Performed Recently?

Recent times have been advantageous for Ranpak Holdings as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. If not, then existing shareholders might be a little nervous about the viability of the share price.

Keen to find out how analysts think Ranpak Holdings' future stacks up against the industry? In that case, our free report is a great place to start.

Is There Enough Revenue Growth Forecasted For Ranpak Holdings?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Ranpak Holdings' to be considered reasonable.

Retrospectively, the last year delivered a decent 8.9% gain to the company's revenues. However, this wasn't enough as the latest three year period has seen an unpleasant 3.4% overall drop in revenue. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to climb by 10% during the coming year according to the dual analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 16%, which is noticeably more attractive.

With this information, we find it concerning that Ranpak Holdings is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

It comes as a surprise to see Ranpak Holdings trade at such a high P/S given the revenue forecasts look less than stellar. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Ranpak Holdings you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?擔心內容嗎?直接聯繫我們。或者,發送電子郵件給編輯組(網址爲)simplywallst.com。 Simply Wall ST 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

Retrospectively, the last year delivered a decent 8.9% gain to the company's revenues. However, this wasn't enough as the latest three year period has seen an unpleasant 3.4% overall drop in revenue. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Retrospectively, the last year delivered a decent 8.9% gain to the company's revenues. However, this wasn't enough as the latest three year period has seen an unpleasant 3.4% overall drop in revenue. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

回顧過去,去年的公司收入實現了8.9%的可觀增長。但是,這還不夠,因爲在最近三年中,總收入下降了3.4%,令人不快。因此,可以公平地說,最近的收入增長對公司來說是不可取的。

回顧過去,去年的公司收入實現了8.9%的可觀增長。但是,這還不夠,因爲在最近三年中,總收入下降了3.4%,令人不快。因此,可以公平地說,最近的收入增長對公司來說是不可取的。