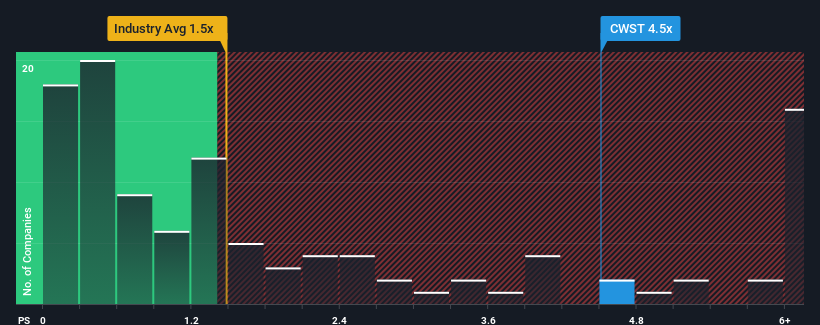

When close to half the companies in the Commercial Services industry in the United States have price-to-sales ratios (or "P/S") below 1.5x, you may consider Casella Waste Systems, Inc. (NASDAQ:CWST) as a stock to avoid entirely with its 4.5x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

NasdaqGS:CWST Price to Sales Ratio vs Industry December 16th 2024

What Does Casella Waste Systems' P/S Mean For Shareholders?

Casella Waste Systems certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. If not, then existing shareholders might be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Casella Waste Systems will help you uncover what's on the horizon.

How Is Casella Waste Systems' Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Casella Waste Systems' to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 27% last year. The strong recent performance means it was also able to grow revenue by 76% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 11% each year during the coming three years according to the nine analysts following the company. With the industry only predicted to deliver 8.4% each year, the company is positioned for a stronger revenue result.

With this information, we can see why Casella Waste Systems is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Casella Waste Systems' P/S?

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Casella Waste Systems maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Commercial Services industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Having said that, be aware Casella Waste Systems is showing 4 warning signs in our investment analysis, you should know about.

If you're unsure about the strength of Casella Waste Systems' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company grew revenue by an impressive 27% last year. The strong recent performance means it was also able to grow revenue by 76% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Taking a look back first, we see that the company grew revenue by an impressive 27% last year. The strong recent performance means it was also able to grow revenue by 76% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

回顧一下,我們看到該公司去年營業收入增長了令人印象深刻的27%。強勁的近期表現意味着它在過去三年裏總共能夠增長76%的營業收入。因此,可以公平地說,最近營業收入的增長對公司來說非常出色。

回顧一下,我們看到該公司去年營業收入增長了令人印象深刻的27%。強勁的近期表現意味着它在過去三年裏總共能夠增長76%的營業收入。因此,可以公平地說,最近營業收入的增長對公司來說非常出色。