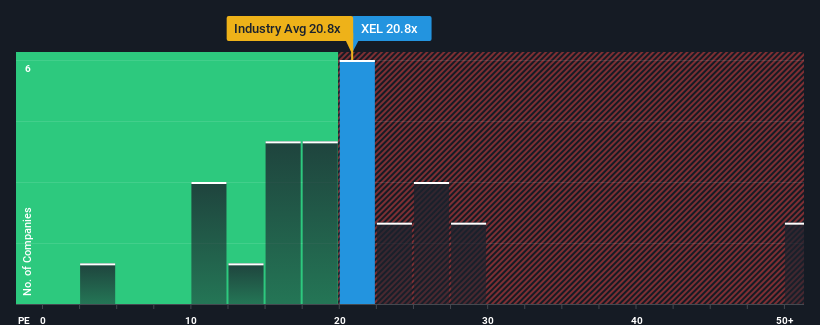

With a median price-to-earnings (or "P/E") ratio of close to 19x in the United States, you could be forgiven for feeling indifferent about Xcel Energy Inc.'s (NASDAQ:XEL) P/E ratio of 20.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Recent times have been advantageous for Xcel Energy as its earnings have been rising faster than most other companies. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

NasdaqGS:XEL Price to Earnings Ratio vs Industry December 14th 2024 Want the full picture on analyst estimates for the company? Then our free report on Xcel Energy will help you uncover what's on the horizon.

What Are Growth Metrics Telling Us About The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Xcel Energy's to be considered reasonable.

If we review the last year of earnings growth, the company posted a worthy increase of 6.6%. EPS has also lifted 12% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 8.8% per annum over the next three years. With the market predicted to deliver 11% growth per year, the company is positioned for a weaker earnings result.

With this information, we find it interesting that Xcel Energy is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

What We Can Learn From Xcel Energy's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Xcel Energy's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

You should always think about risks. Case in point, we've spotted 3 warning signs for Xcel Energy you should be aware of, and 1 of them is significant.

You might be able to find a better investment than Xcel Energy. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of earnings growth, the company posted a worthy increase of 6.6%. EPS has also lifted 12% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

If we review the last year of earnings growth, the company posted a worthy increase of 6.6%. EPS has also lifted 12% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

如果我們回顧過去一年的收益增長,公司實現了值得稱讚的6.6%的增長。每股收益也在過去三年中累計提升了12%,部分得益於過去12個月的增長。因此,我們可以先確認公司在這段時間內確實做得很好,收益增長表現良好。

如果我們回顧過去一年的收益增長,公司實現了值得稱讚的6.6%的增長。每股收益也在過去三年中累計提升了12%,部分得益於過去12個月的增長。因此,我們可以先確認公司在這段時間內確實做得很好,收益增長表現良好。