Semler Scientific, Inc. (NASDAQ:SMLR) shares have continued their recent momentum with a 41% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 48% in the last year.

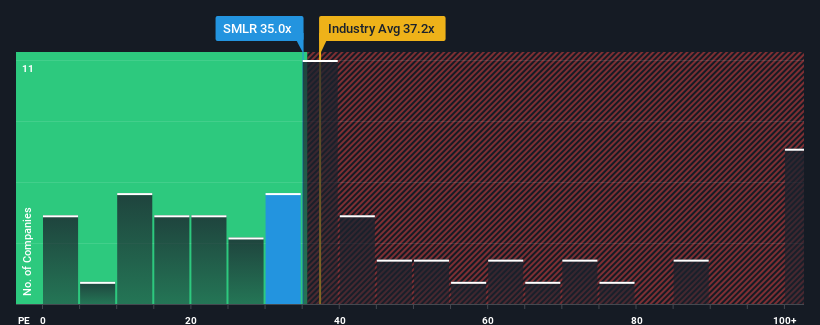

Since its price has surged higher, Semler Scientific's price-to-earnings (or "P/E") ratio of 35x might make it look like a strong sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 19x and even P/E's below 11x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

For instance, Semler Scientific's receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

NasdaqCM:SMLR Price to Earnings Ratio vs Industry December 14th 2024 We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Semler Scientific's earnings, revenue and cash flow.

Does Growth Match The High P/E?

Semler Scientific's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Retrospectively, the last year delivered a frustrating 21% decrease to the company's bottom line. As a result, earnings from three years ago have also fallen 39% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 15% shows it's an unpleasant look.

In light of this, it's alarming that Semler Scientific's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

What We Can Learn From Semler Scientific's P/E?

Semler Scientific's P/E is flying high just like its stock has during the last month. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Semler Scientific currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the high P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you take the next step, you should know about the 3 warning signs for Semler Scientific (2 make us uncomfortable!) that we have uncovered.

Of course, you might also be able to find a better stock than Semler Scientific. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Semler Scientific's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Semler Scientific's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Semler Scientific的市盈率對於一家被期望能實現非常強勁增長的公司來說是典型的,並且更重要的是,表現遠超市場。

Semler Scientific的市盈率對於一家被期望能實現非常強勁增長的公司來說是典型的,並且更重要的是,表現遠超市場。