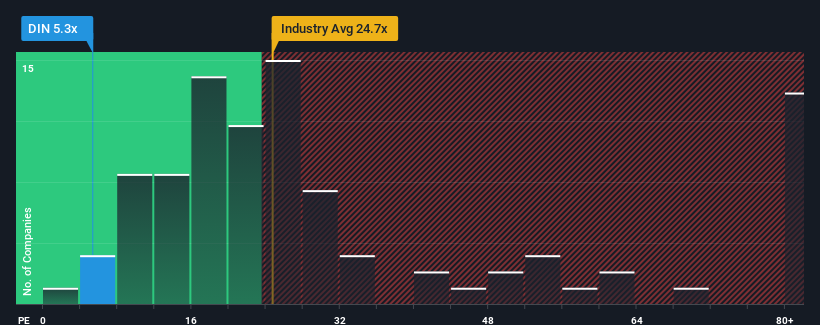

Dine Brands Global, Inc.'s (NYSE:DIN) price-to-earnings (or "P/E") ratio of 5.3x might make it look like a strong buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 20x and even P/E's above 35x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for Dine Brands Global as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

NYSE:DIN Price to Earnings Ratio vs Industry December 10th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Dine Brands Global.

Is There Any Growth For Dine Brands Global?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Dine Brands Global's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 25% last year. The strong recent performance means it was also able to grow EPS by 32% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to slump, contracting by 17% during the coming year according to the eight analysts following the company. Meanwhile, the broader market is forecast to expand by 15%, which paints a poor picture.

With this information, we are not surprised that Dine Brands Global is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Bottom Line On Dine Brands Global's P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Dine Brands Global's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you take the next step, you should know about the 3 warning signs for Dine Brands Global (2 are potentially serious!) that we have uncovered.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Dine Brands Global, Inc.(紐交所:DIN)的市盈率(或稱"P/E")爲5.3倍,可能讓它在美國市場上看起來像是一個強勁的買入選擇,而在美國,大約一半的公司市盈率超過20倍,甚至超過35倍的市盈率也相當普遍。然而,市盈率可能較低是有原因的,需要進一步調查以判斷這種情況是否合理。

Taking a look back first, we see that the company grew earnings per share by an impressive 25% last year. The strong recent performance means it was also able to grow EPS by 32% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Taking a look back first, we see that the company grew earnings per share by an impressive 25% last year. The strong recent performance means it was also able to grow EPS by 32% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

通常情況下,我們會警告在做出投資決策時不要過度解讀市盈率,儘管它能揭示出其他市場參與者對公司的看法。

通常情況下,我們會警告在做出投資決策時不要過度解讀市盈率,儘管它能揭示出其他市場參與者對公司的看法。