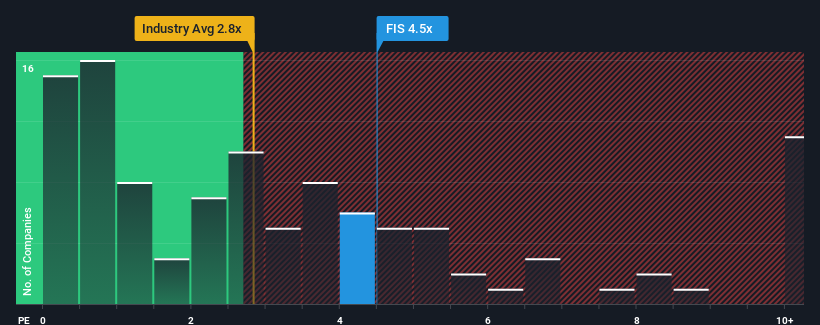

Fidelity National Information Services, Inc.'s (NYSE:FIS) price-to-sales (or "P/S") ratio of 4.5x may not look like an appealing investment opportunity when you consider close to half the companies in the Diversified Financial industry in the United States have P/S ratios below 2.8x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

NYSE:FIS Price to Sales Ratio vs Industry December 10th 2024

What Does Fidelity National Information Services' Recent Performance Look Like?

Recent times haven't been great for Fidelity National Information Services as its revenue has been rising slower than most other companies. Perhaps the market is expecting future revenue performance to undergo a reversal of fortunes, which has elevated the P/S ratio. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on Fidelity National Information Services will help you uncover what's on the horizon.

Is There Enough Revenue Growth Forecasted For Fidelity National Information Services?

In order to justify its P/S ratio, Fidelity National Information Services would need to produce impressive growth in excess of the industry.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. The lack of growth did nothing to help the company's aggregate three-year performance, which is an unsavory 26% drop in revenue. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 4.1% each year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 8.7% per annum, which is noticeably more attractive.

With this in consideration, we believe it doesn't make sense that Fidelity National Information Services' P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Final Word

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Despite analysts forecasting some poorer-than-industry revenue growth figures for Fidelity National Information Services, this doesn't appear to be impacting the P/S in the slightest. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

There are also other vital risk factors to consider before investing and we've discovered 3 warning signs for Fidelity National Information Services that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. The lack of growth did nothing to help the company's aggregate three-year performance, which is an unsavory 26% drop in revenue. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. The lack of growth did nothing to help the company's aggregate three-year performance, which is an unsavory 26% drop in revenue. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

回顧去年營業收入,公司發佈的結果幾乎沒有與去年相比的偏差。增長的缺乏對公司整體三年的表現沒有幫助,導致營業收入下降了26%。因此,可以公平地說,公司最近的營業收入增長令人不滿意。

回顧去年營業收入,公司發佈的結果幾乎沒有與去年相比的偏差。增長的缺乏對公司整體三年的表現沒有幫助,導致營業收入下降了26%。因此,可以公平地說,公司最近的營業收入增長令人不滿意。