When you buy and hold a stock for the long term, you definitely want it to provide a positive return. Better yet, you'd like to see the share price move up more than the market average. But Pinterest, Inc. (NYSE:PINS) has fallen short of that second goal, with a share price rise of 77% over five years, which is below the market return. Unfortunately the share price is down 8.7% in the last year.

On the back of a solid 7-day performance, let's check what role the company's fundamentals have played in driving long term shareholder returns.

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

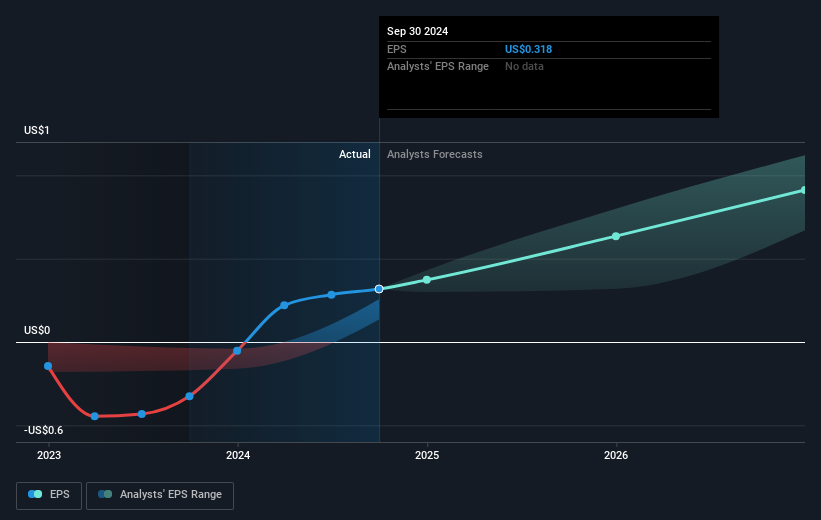

During the five years of share price growth, Pinterest moved from a loss to profitability. That's generally thought to be a genuine positive, so investors may expect to see an increasing share price.

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

NYSE:PINS Earnings Per Share Growth December 9th 2024

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. Dive deeper into the earnings by checking this interactive graph of Pinterest's earnings, revenue and cash flow.

A Different Perspective

Pinterest shareholders are down 8.7% for the year, but the market itself is up 34%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. On the bright side, long term shareholders have made money, with a gain of 12% per year over half a decade. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. You might want to assess this data-rich visualization of its earnings, revenue and cash flow.

But note: Pinterest may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?擔心內容嗎?直接聯繫我們。或者,發送電子郵件給編輯組(網址爲)simplywallst.com。 Simply Wall St 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

During the five years of share price growth, Pinterest moved from a loss to profitability. That's generally thought to be a genuine positive, so investors may expect to see an increasing share price.

During the five years of share price growth, Pinterest moved from a loss to profitability. That's generally thought to be a genuine positive, so investors may expect to see an increasing share price.  在股價增長的五年中,Pinterest從虧損轉爲盈利。人們普遍認爲這是真正的積極因素,因此投資者可能會看到股價上漲。

在股價增長的五年中,Pinterest從虧損轉爲盈利。人們普遍認爲這是真正的積極因素,因此投資者可能會看到股價上漲。