Green Plains (NASDAQ:GPRE Shareholders Incur Further Losses as Stock Declines 6.9% This Week, Taking Three-year Losses to 71%

Green Plains (NASDAQ:GPRE Shareholders Incur Further Losses as Stock Declines 6.9% This Week, Taking Three-year Losses to 71%

Over three years, Green Plains grew revenue at 0.09% per year. Given it's losing money in pursuit of growth, we are not really impressed with that. Nonetheless, it's fair to say the rapidly declining share price (down 19%, compound, over three years) suggests the market is very disappointed with this level of growth. We generally don't try to 'catch the falling knife'. Of course, revenue growth is nice but generally speaking the lower the profits, the riskier the business - and this business isn't making steady profits.

Over three years, Green Plains grew revenue at 0.09% per year. Given it's losing money in pursuit of growth, we are not really impressed with that. Nonetheless, it's fair to say the rapidly declining share price (down 19%, compound, over three years) suggests the market is very disappointed with this level of growth. We generally don't try to 'catch the falling knife'. Of course, revenue growth is nice but generally speaking the lower the profits, the riskier the business - and this business isn't making steady profits. As an investor, mistakes are inevitable. But really bad investments should be rare. So spare a thought for the long term shareholders of Green Plains Inc. (NASDAQ:GPRE); the share price is down a whopping 71% in the last three years. That would certainly shake our confidence in the decision to own the stock. And more recent buyers are having a tough time too, with a drop of 57% in the last year. Shareholders have had an even rougher run lately, with the share price down 11% in the last 90 days.

作爲投資者,錯誤是不可避免的。但真正糟糕的投資應該是少數。所以請爲綠色平原能源(納斯達克: GPRE)的長期股東考慮一下;在過去三年裏,股價下跌了驚人的71%。這無疑動搖了我們對持有該股票決策的信心。而且,最近的買家也面臨着艱難的處境,去年股價下跌了57%。股東們最近的處境更爲艱難,過去90天股價下跌了11%。

Since Green Plains has shed US$50m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

由於綠色平原能源在過去7天內損失了5000萬美元,讓我們看看長期衰退是否是由業務經濟驅動的。

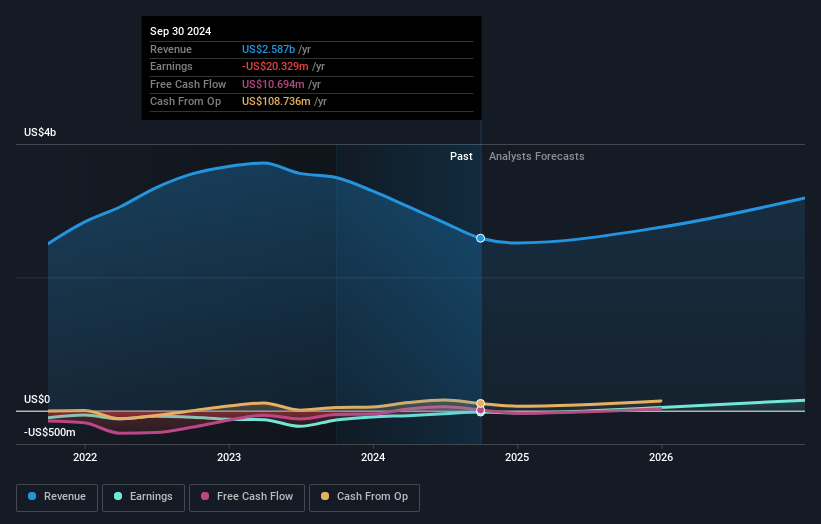

Because Green Plains made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually desire strong revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

因爲綠色平原能源在過去12個月裏出現了虧損,我們認爲市場現在可能更關注營業收入和營業收入增長。無盈利公司的股東通常希望獲得強勁的營業收入增長。這是因爲快速的營業收入增長可以很容易地用於預測利潤,通常規模可觀。

Over three years, Green Plains grew revenue at 0.09% per year. Given it's losing money in pursuit of growth, we are not really impressed with that. Nonetheless, it's fair to say the rapidly declining share price (down 19%, compound, over three years) suggests the market is very disappointed with this level of growth. We generally don't try to 'catch the falling knife'. Of course, revenue growth is nice but generally speaking the lower the profits, the riskier the business - and this business isn't making steady profits.

在三年裏,綠色平原能源的營業收入年增長率爲0.09%。考慮到它在追求增長的過程中正在虧損,這讓我們並不特別印象深刻。不過,可以公平地說,快速下降的股價(在三年內下降19%,compound)表明市場對這種增長水平非常失望。我們通常不試圖「接住下跌的刀」。當然,營業收入增長是好的,但一般而言,利潤越少,業務的風險就越大,而這項業務並沒有穩定的利潤。

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

以下圖像顯示了公司的營業收入和盈利(隨時間變化)(單擊以查看準確的數字)。

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. If you are thinking of buying or selling Green Plains stock, you should check out this free report showing analyst profit forecasts.

我們認爲內部人士在過去一年進行了大量購買是一個積極的信號。儘管如此,未來的盈利將對當前股東盈利的重要性遠超。假如你考慮購買或賣出綠色平原能源的股票,你應該查看這份免費的報告,報告中顯示了分析師的盈利預測。

A Different Perspective

另一種看法

While the broader market gained around 34% in the last year, Green Plains shareholders lost 57%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 6% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Green Plains , and understanding them should be part of your investment process.

在過去一年裏,整體市場上漲了約34%,而綠色平原能源的股東卻損失了57%。即使是優秀股票的股價有時也會下跌,但在我們過於關注之前,我們希望看到業務基本指標的改善。不幸的是,去年的表現可能表明尚未解決的挑戰,因爲它比過去五年的年化損失6%還要糟糕。我們意識到,巴倫·羅斯柴爾德曾說過投資者應該在「街頭流血時買入」,但我們提醒投資者首先要確保自己購買的是高質量的業務。 我發現從長遠來看觀察股票價格作爲業務績效的代理指標非常有趣。但爲了真正獲得洞察力,我們需要考慮其他信息。舉個例子,投資風險這個無處不在的幽靈。我們已經識別出綠色平原能源的一個警示信號,理解它們應該是你投資過程的一部分。

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of undervalued small cap companies that insiders are buying.

還有很多其他的公司,公司的內部人士正在購買股票。你可能不想錯過這個免費的小市值公司的低估列表。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

請注意,本文所引述的市場回報反映了目前在美國交易所上市的股票的市場加權平均回報。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。