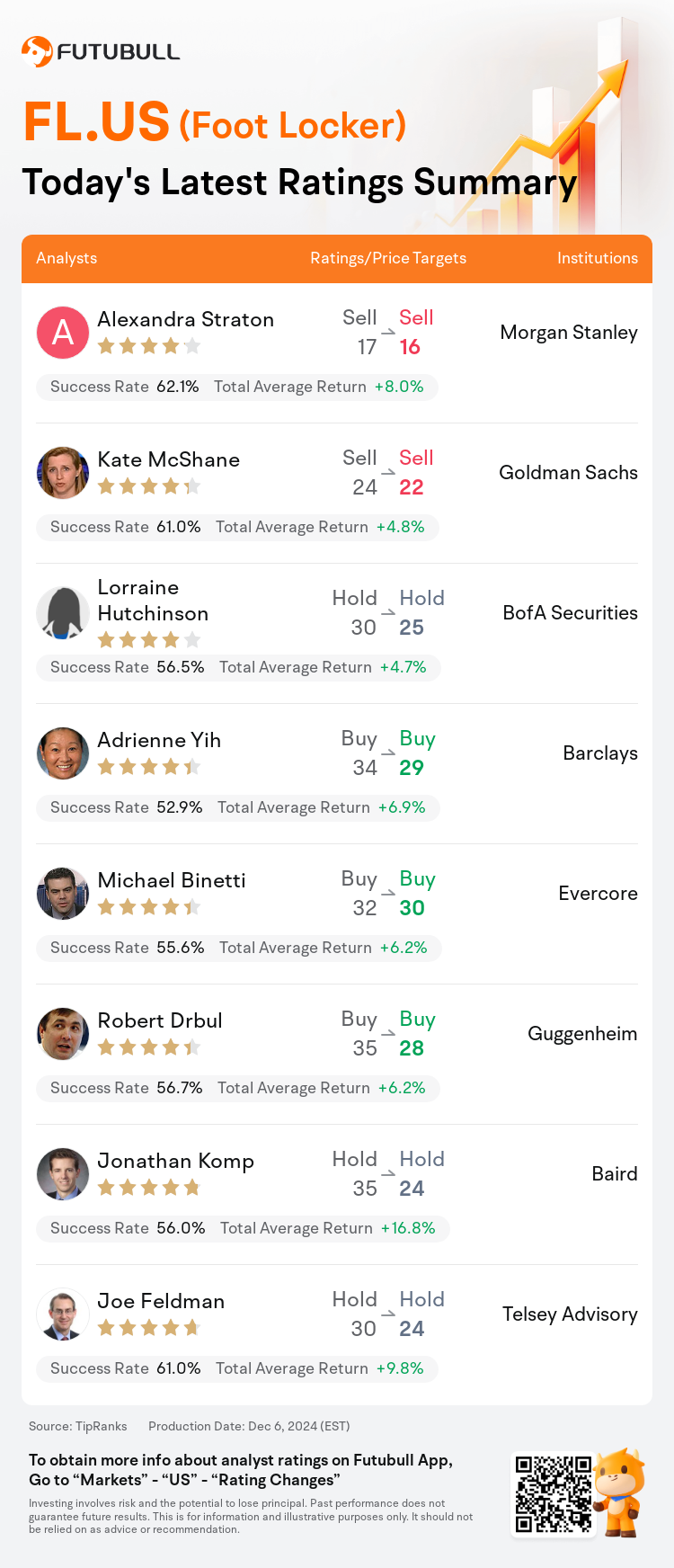

On Dec 06, major Wall Street analysts update their ratings for $Foot Locker (FL.US)$, with price targets ranging from $16 to $30.

Morgan Stanley analyst Alexandra Straton maintains with a sell rating, and adjusts the target price from $17 to $16.

Goldman Sachs analyst Kate McShane maintains with a sell rating, and adjusts the target price from $24 to $22.

BofA Securities analyst Lorraine Hutchinson maintains with a hold rating, and adjusts the target price from $30 to $25.

BofA Securities analyst Lorraine Hutchinson maintains with a hold rating, and adjusts the target price from $30 to $25.

Barclays analyst Adrienne Yih maintains with a buy rating, and adjusts the target price from $34 to $29.

Evercore analyst Michael Binetti maintains with a buy rating, and adjusts the target price from $32 to $30.

Furthermore, according to the comprehensive report, the opinions of $Foot Locker (FL.US)$'s main analysts recently are as follows:

Foot Locker's Q3 results fell short of expectations, as trends weakened over the quarter and promotional activities increased. The company revised its fiscal 2024 forecasts downwards for sales and earnings, anticipating continued promotions but with a strategic shift towards footwear in the fourth quarter.

Foot Locker's recent Q3 miss and subsequent reduction in FY guidance underscore ongoing concerns about the company's potential for recovery. This situation provides more evidence for bearish perspectives. Furthermore, perceived risks to full-year and mid-term street EPS projections persist, according to analysts.

The analyst indicated a reevaluation of expectations through a reduced fiscal year earnings forecast due to persisting margin pressures expected in the fourth quarter. This assessment considers that the current valuation of the stock mitigates the associated risks linked to sales revitalization and margin recuperation.

Despite a 30% decrease in stock value over the past three months, the current valuation of Foot Locker is still not considered attractive due to significant downside risks. Challenges include struggles faced by its primary brand partner and increasing competition from direct-to-consumer channels of other brands, as well as competitors like JD Sports.

Foot Locker's Q3 performance fell short of expectations, and the company has reduced its future guidance. Additionally, the revised fiscal 2024 gross margin guidance suggests a recovery of only 30% of the 300 basis point merchandise margin headwind experienced in fiscal 2023's gross margin, as opposed to the previously anticipated 60%.

Here are the latest investment ratings and price targets for $Foot Locker (FL.US)$ from 8 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

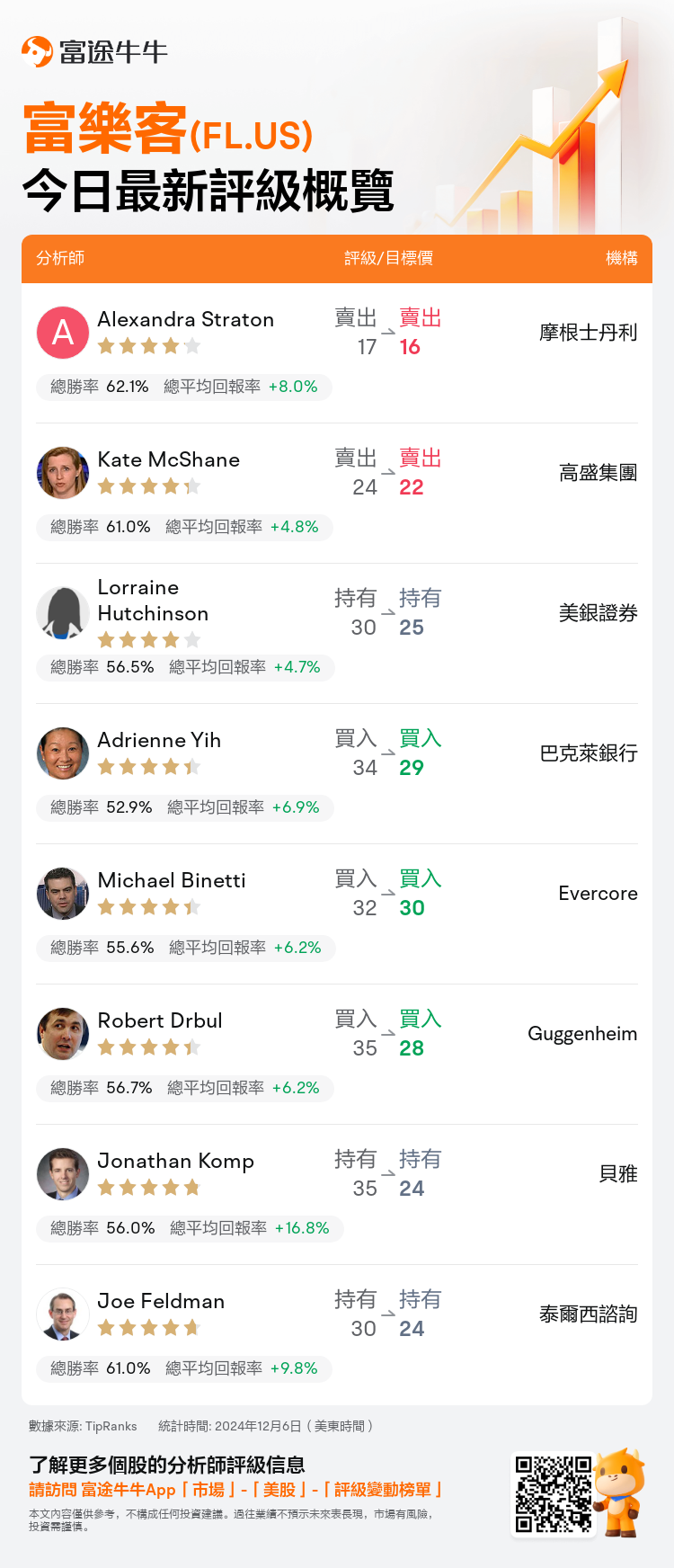

美東時間12月6日,多家華爾街大行更新了$富樂客 (FL.US)$的評級,目標價介於16美元至30美元。

摩根士丹利分析師Alexandra Straton維持賣出評級,並將目標價從17美元下調至16美元。

高盛集團分析師Kate McShane維持賣出評級,並將目標價從24美元下調至22美元。

美銀證券分析師Lorraine Hutchinson維持持有評級,並將目標價從30美元下調至25美元。

美銀證券分析師Lorraine Hutchinson維持持有評級,並將目標價從30美元下調至25美元。

巴克萊銀行分析師Adrienne Yih維持買入評級,並將目標價從34美元下調至29美元。

Evercore分析師Michael Binetti維持買入評級,並將目標價從32美元下調至30美元。

此外,綜合報道,$富樂客 (FL.US)$近期主要分析師觀點如下:

富樂客的第三季度業績不及預期,隨着季度內趨勢走弱和促銷活動增加。 公司下調了2024財年的銷售和收益預期,預計繼續促銷但在第四季度將戰略轉向鞋類。

富樂客最近的第三季度業績不佳以及隨後降低的全年指導,凸顯了對公司復甦潛力持續關注的擔憂。 這種情況爲看淡觀點提供了更多證據。 此外,根據分析師,全年和中期街頭EPS預測所面臨的風險被認爲存在。

分析師表示,通過降低財年盈利預測來重新評估預期,因爲預計第四季度仍將面臨持續的毛利率壓力。 該評估考慮到,目前股票的估值有助於緩解銷售復甦和利潤恢復所帶來的風險。

儘管過去三個月股價下跌了30%,但由於存在重大下行風險,富樂客的當前估值仍不被視爲有吸引力。 挑戰包括該公司主要品牌合作伙伴面臨的困境,以及來自其他品牌直銷渠道和競爭對手(如JD Sports)的競爭日益激烈。

富樂客第三季度表現不佳,未達預期,並已調低未來指導。 另外,修訂後的2024財年毛利率指導意味着只有在財年2023毛利率經歷的300個點子商品毛利率不利因素的恢復中恢復了30%,而不是先前預期的60%。

以下爲今日8位分析師對$富樂客 (FL.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。