Honeywell International (NASDAQ:HON) Ticks All The Boxes When It Comes To Earnings Growth

Honeywell International (NASDAQ:HON) Ticks All The Boxes When It Comes To Earnings Growth

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Honeywell International maintained stable EBIT margins over the last year, all while growing revenue 4.0% to US$38b. That's a real positive.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Honeywell International maintained stable EBIT margins over the last year, all while growing revenue 4.0% to US$38b. That's a real positive. For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

對於初學者來說,買一個向投資者講述好故事的公司似乎是一個好主意(也是一個令人興奮的前景),即使它目前缺少營業收入和利潤的記錄。不幸的是,這些高風險投資往往很少有可能產生回報,許多投資者付出代價來學習他們的教訓。虧損的公司可以像吸取資本的海綿一樣 - 所以投資者應謹慎,不要把好錢投進去。

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Honeywell International (NASDAQ:HON). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

如果這種公司不符合你的風格,而你喜歡那些創造營收,甚至盈利的公司,那麼你可能會對霍尼韋爾國際(納斯達克:HON)感興趣。雖然利潤並不是投資時唯一應考慮的指標,但值得注意的是那些能夠持續產生利潤的企業。

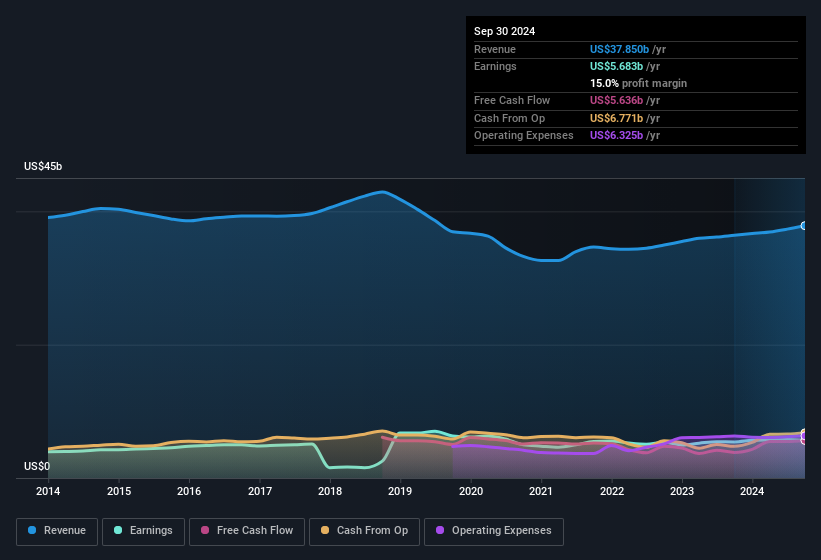

Honeywell International's Improving Profits

霍尼韋爾國際利潤改善

Even when EPS earnings per share (EPS) growth is unexceptional, company value can be created if this rate is sustained each year. So it's no surprise that some investors are more inclined to invest in profitable businesses. Over the last year, Honeywell International increased its EPS from US$8.12 to US$8.74. That's a fair increase of 7.6%.

即使每股收益(EPS)增長未達預期,若增長率每年持續,公司價值仍可增加。因此,一些投資者更傾向於投資盈利的企業也就不奇怪了。過去一年,霍尼韋爾國際的每股收益從8.12美元增加到8.74美元,增長了7.6%。

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Honeywell International maintained stable EBIT margins over the last year, all while growing revenue 4.0% to US$38b. That's a real positive.

仔細考慮營收增長和利潤增長前利潤(EBIT)利潤率,可以幫助判斷最近利潤增長的可持續性。霍尼韋爾國際在過去一年中保持穩定的EBIt利潤率,同時實現了營收增長4.0%,達到380億美元。這是一個真正的正面信號。

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

下面的表格顯示了公司的營收和淨利潤如何隨着時間的推移的變化。點擊圖表可以查看準確的數字。

The trick, as an investor, is to find companies that are going to perform well in the future, not just in the past. While crystal balls don't exist, you can check our visualization of consensus analyst forecasts for Honeywell International's future EPS 100% free.

作爲投資者的訣竅在於找到未來表現良好的公司,而不僅僅是過去。雖然不存在水晶球,但您可以免費查看我們對霍尼韋爾國際未來每股收益的共識分析師預測的可視化。

Are Honeywell International Insiders Aligned With All Shareholders?

霍尼韋爾國際內部人與所有股東是否保持一致?

Since Honeywell International has a market capitalisation of US$149b, we wouldn't expect insiders to hold a large percentage of shares. But we do take comfort from the fact that they are investors in the company. Notably, they have an enviable stake in the company, worth US$129m. This comes in at 0.09% of shares in the company, which is a fair amount of a business of this size. This should still be a great incentive for management to maximise shareholder value.

由於霍尼韋爾國際的市值爲1490億美元,我們不會指望內部人擁有大量股份。但我們對他們作爲公司投資者的事實感到欣慰。值得注意的是,他們在公司中擁有一大比例股權,價值爲12900萬美元。這佔公司股份的0.09%,對於這樣規模的企業來說是一個相當大的數額。這應該仍然是管理層最大化股東價值的巨大激勵。

Is Honeywell International Worth Keeping An Eye On?

霍尼韋爾國際值得密切關注嗎?

One important encouraging feature of Honeywell International is that it is growing profits. To add an extra spark to the fire, significant insider ownership in the company is another highlight. These two factors are a huge highlight for the company which should be a strong contender your watchlists. Still, you should learn about the 1 warning sign we've spotted with Honeywell International.

霍尼韋爾國際一個重要的鼓舞人心的特點是其利潤增長。爲了給火上添油,公司內部人持有大量股權也是另一亮點。這兩個因素是該公司的重要亮點,應該成爲您關注的公司之一。不過,您應該了解我們發現的關於霍尼韋爾國際的一個警示信號。

Although Honeywell International certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with more skin in the game, then check out this handpicked selection of companies that not only boast of strong growth but have strong insider backing.

儘管霍尼韋爾國際看起來不錯,但如果內部人員正在大量買入股票,可能會吸引更多投資者。如果您喜歡看到更多內部人員參與的公司,那麼請查看這些精選公司,它們不僅擁有強勁的增長,而且有着強勁的內部支持。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

請注意,本文討論的內部交易是指在相關司法管轄區中報告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。