The Navitas Semiconductor Corporation (NASDAQ:NVTS) share price has done very well over the last month, posting an excellent gain of 60%. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 50% share price drop in the last twelve months.

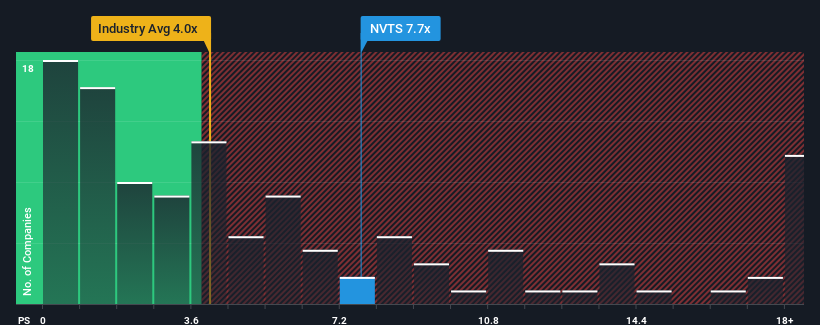

Following the firm bounce in price, Navitas Semiconductor may be sending strong sell signals at present with a price-to-sales (or "P/S") ratio of 7.7x, when you consider almost half of the companies in the Semiconductor industry in the United States have P/S ratios under 4x and even P/S lower than 1.5x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

NasdaqGM:NVTS Price to Sales Ratio vs Industry December 6th 2024

How Has Navitas Semiconductor Performed Recently?

Recent times haven't been great for Navitas Semiconductor as its revenue has been rising slower than most other companies. It might be that many expect the uninspiring revenue performance to recover significantly, which has kept the P/S ratio from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on Navitas Semiconductor will help you uncover what's on the horizon.

What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Navitas Semiconductor's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 39%. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the eight analysts covering the company suggest revenue should grow by 22% each year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 26% each year, which is noticeably more attractive.

With this information, we find it concerning that Navitas Semiconductor is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

Navitas Semiconductor's P/S has grown nicely over the last month thanks to a handy boost in the share price. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've concluded that Navitas Semiconductor currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. At these price levels, investors should remain cautious, particularly if things don't improve.

You should always think about risks. Case in point, we've spotted 4 warning signs for Navitas Semiconductor you should be aware of, and 1 of them shouldn't be ignored.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Navitas Semiconductor's to be considered reasonable.

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Navitas Semiconductor's to be considered reasonable.

有一種固有的假設,即公司應該遠遠超越行業,像Navitas Semiconductor這樣的市銷率才能被視爲合理。

有一種固有的假設,即公司應該遠遠超越行業,像Navitas Semiconductor這樣的市銷率才能被視爲合理。