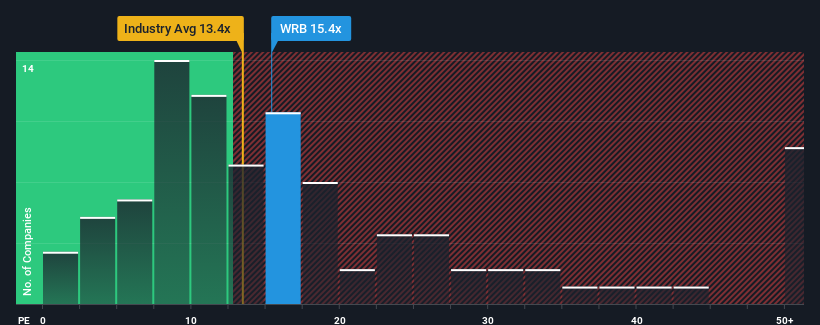

W. R. Berkley Corporation's (NYSE:WRB) price-to-earnings (or "P/E") ratio of 15.4x might make it look like a buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 20x and even P/E's above 36x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for W. R. Berkley as its earnings have been rising faster than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

NYSE:WRB Price to Earnings Ratio vs Industry December 5th 2024 Keen to find out how analysts think W. R. Berkley's future stacks up against the industry? In that case, our free report is a great place to start.

How Is W. R. Berkley's Growth Trending?

W. R. Berkley's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 18% last year. The strong recent performance means it was also able to grow EPS by 66% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 2.5% per annum as estimated by the ten analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 11% per annum, which is noticeably more attractive.

In light of this, it's understandable that W. R. Berkley's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of W. R. Berkley's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You always need to take note of risks, for example - W. R. Berkley has 1 warning sign we think you should be aware of.

If these risks are making you reconsider your opinion on W. R. Berkley, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

W. R.伯克利公司(紐交所:WRB)的市盈率爲15.4倍,與美國市場相比可能看起來像是一個買入的時機,因爲約一半的公司市盈率超過20倍,甚至超過36倍的公司並不少見。然而,市盈率可能之所以低是有原因的,需要進一步調查來判斷是否合理。

Taking a look back first, we see that the company grew earnings per share by an impressive 18% last year. The strong recent performance means it was also able to grow EPS by 66% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Taking a look back first, we see that the company grew earnings per share by an impressive 18% last year. The strong recent performance means it was also able to grow EPS by 66% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

首先回顧一下,我們發現該公司去年每股收益增長了驚人的18%。近期強勁的表現意味着過去三年它也能夠使每股收益總體增長了66%。因此,股東們可能會對這些中期盈利增速感到歡迎。

首先回顧一下,我們發現該公司去年每股收益增長了驚人的18%。近期強勁的表現意味着過去三年它也能夠使每股收益總體增長了66%。因此,股東們可能會對這些中期盈利增速感到歡迎。