We Think Prothena (NASDAQ:PRTA) Can Afford To Drive Business Growth

We Think Prothena (NASDAQ:PRTA) Can Afford To Drive Business Growth

Prothena boosted investment sharply in the last year, with cash burn ramping by 74%. As if that's not bad enough, the operating revenue also dropped by 5.4%, making us very wary indeed. Considering both these metrics, we're a little concerned about how the company is developing. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years.

Prothena boosted investment sharply in the last year, with cash burn ramping by 74%. As if that's not bad enough, the operating revenue also dropped by 5.4%, making us very wary indeed. Considering both these metrics, we're a little concerned about how the company is developing. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years. Just because a business does not make any money, does not mean that the stock will go down. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

僅因企業不盈利並不意味着股票會下跌。例如,生物科技和採礦勘探公司經常在發現新治療方法或礦物質之前多年虧損。然而,只有愚不可及之人才會忽視一家輸錢的公司很快就會耗盡其資金的風險。

So should Prothena (NASDAQ:PRTA) shareholders be worried about its cash burn? For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

那麼Prothena(納斯達克:PRTA)的股東是否應該擔心其現金消耗?在本文中,我們將現金消耗定義爲公司每年用於資助其增長的現金數額(也稱爲其負的自由現金流)。首先,我們將通過比較其現金消耗與現金儲備來判斷其現金持續時間。

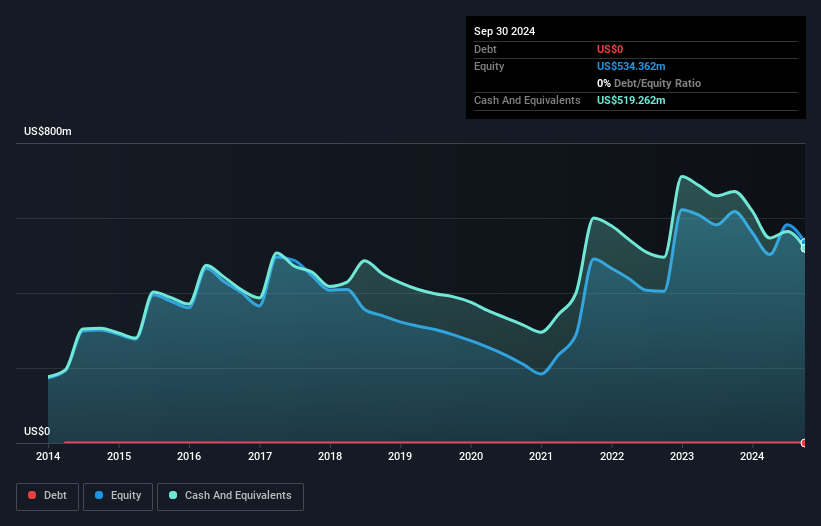

Does Prothena Have A Long Cash Runway?

Prothena的現金持續時間長嗎?

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. As at September 2024, Prothena had cash of US$519m and no debt. In the last year, its cash burn was US$155m. That means it had a cash runway of about 3.3 years as of September 2024. Notably, analysts forecast that Prothena will break even (at a free cash flow level) in about 4 years. So there's a very good chance it won't need more cash, when you consider the burn rate will be reducing in that period. The image below shows how its cash balance has been changing over the last few years.

您可以通過將公司擁有的現金量除以其花費現金的速度來計算公司的現金持續時間。截至2024年9月,Prothena的現金爲51900萬美元,無債務。去年,它的現金消耗爲15500萬美元。這意味着截至2024年9月,它的現金持續時間約爲3.3年。值得注意的是,分析師預測Prothena將在約4年內實現收支平衡(在自由現金流水平上)。因此,考慮到在此期間消耗率將減少,它很有可能不再需要更多現金。下圖顯示了過去幾年來其現金餘額的變化情況。

How Well Is Prothena Growing?

Prothena的增長情況如何?

Prothena boosted investment sharply in the last year, with cash burn ramping by 74%. As if that's not bad enough, the operating revenue also dropped by 5.4%, making us very wary indeed. Considering both these metrics, we're a little concerned about how the company is developing. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years.

Prothena在過去一年中大幅增加投資,現金消耗增長了74%。更糟糕的是,營業收入也下降了5.4%,這讓我們非常警惕。考慮到這兩個指標,我們對公司的發展有些擔憂。雖然過去總是值得研究,但未來才是最重要的。所以您可能想看看公司的預期增長情況。

How Hard Would It Be For Prothena To Raise More Cash For Growth?

Prothena籌集更多資金以促進增長會有多困難?

Prothena seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Prothena的現金消耗情況相對良好,但我們認爲考慮它如果想籌集更多資金會有多容易還是值得的。公司可以通過債務或股權籌集資本。通常,業務會出售新股以籌集現金並推動增長。通過將公司年度現金消耗與其總市值進行比較,我們可以大致估算出公司爲維持運營而需要發行多少股份(以相同的消耗率)。

Prothena has a market capitalisation of US$741m and burnt through US$155m last year, which is 21% of the company's market value. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

Prothena的市值爲74100萬美元,去年消耗了15500萬美元,佔公司市場價值的21%。這是相當顯著的現金消耗,因此如果公司必須出售股份來覆蓋另一年運營的成本,股東將遭受一定的稀釋損失。

Is Prothena's Cash Burn A Worry?

Prothena的現金消耗令人擔憂嗎?

On this analysis of Prothena's cash burn, we think its cash runway was reassuring, while its increasing cash burn has us a bit worried. One real positive is that analysts are forecasting that the company will reach breakeven. Cash burning companies are always on the riskier side of things, but after considering all of the factors discussed in this short piece, we're not too worried about its rate of cash burn. Readers need to have a sound understanding of business risks before investing in a stock, and we've spotted 2 warning signs for Prothena that potential shareholders should take into account before putting money into a stock.

在對Prothena現金消耗的分析中,我們認爲其現金儲備令人安心,而其不斷增加的現金消耗讓我們有些擔憂。一個真正的積極因素是,分析師預測該公司將實現盈虧平衡。現金消耗的公司總是處於風險較高的一方,但在考慮到本文討論的所有因素後,我們對其現金消耗率並不太擔心。讀者在投資股票之前需要對業務風險有充分的了解,我們發現Prothena有兩個警示信號,潛在的股東在投資股票之前應予以考慮。

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

當然,您可能會在其他地方尋找到一個出色的投資機會。因此,瞥一眼這個有趣公司的免費名單,和這個股票成長股的(根據分析師預測)。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。