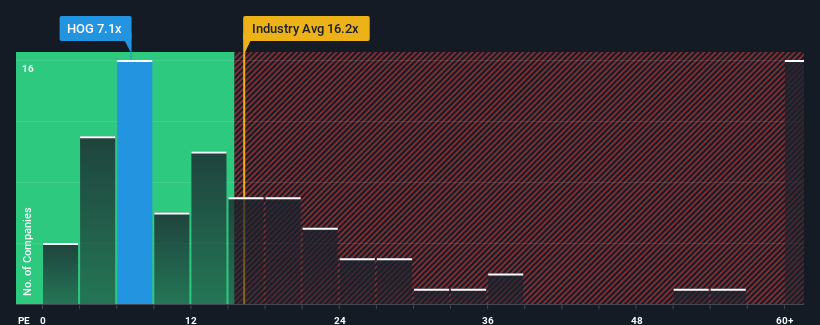

Harley-Davidson, Inc.'s (NYSE:HOG) price-to-earnings (or "P/E") ratio of 7.1x might make it look like a strong buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 20x and even P/E's above 36x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Harley-Davidson hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

NYSE:HOG Price to Earnings Ratio vs Industry December 5th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Harley-Davidson.

How Is Harley-Davidson's Growth Trending?

In order to justify its P/E ratio, Harley-Davidson would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered a frustrating 11% decrease to the company's bottom line. Even so, admirably EPS has lifted 36% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Shifting to the future, estimates from the twelve analysts covering the company suggest earnings should grow by 5.3% per year over the next three years. With the market predicted to deliver 11% growth each year, the company is positioned for a weaker earnings result.

In light of this, it's understandable that Harley-Davidson's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Harley-Davidson's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Harley-Davidson (of which 1 is a bit concerning!) you should know about.

You might be able to find a better investment than Harley-Davidson. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a frustrating 11% decrease to the company's bottom line. Even so, admirably EPS has lifted 36% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Retrospectively, the last year delivered a frustrating 11% decrease to the company's bottom line. Even so, admirably EPS has lifted 36% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

回顧過去一年,對公司的底線造成了令人沮喪的11%下降。儘管如此,令人欽佩的是,每股收益從三年前開始累計上漲了36%,儘管過去12個月有所不同。儘管經歷了曲折,但仍然可以說最近的收益增長對公司來說已經足夠。

回顧過去一年,對公司的底線造成了令人沮喪的11%下降。儘管如此,令人欽佩的是,每股收益從三年前開始累計上漲了36%,儘管過去12個月有所不同。儘管經歷了曲折,但仍然可以說最近的收益增長對公司來說已經足夠。