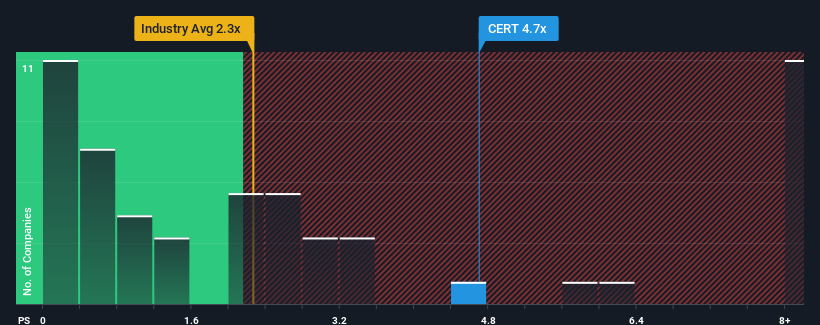

When close to half the companies in the Healthcare Services industry in the United States have price-to-sales ratios (or "P/S") below 2.3x, you may consider Certara, Inc. (NASDAQ:CERT) as a stock to avoid entirely with its 4.7x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

NasdaqGS:CERT Price to Sales Ratio vs Industry December 5th 2024

How Has Certara Performed Recently?

With revenue growth that's inferior to most other companies of late, Certara has been relatively sluggish. Perhaps the market is expecting future revenue performance to undergo a reversal of fortunes, which has elevated the P/S ratio. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Certara's future stacks up against the industry? In that case, our free report is a great place to start.

What Are Revenue Growth Metrics Telling Us About The High P/S?

In order to justify its P/S ratio, Certara would need to produce outstanding growth that's well in excess of the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 5.6%. Pleasingly, revenue has also lifted 35% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 9.2% per year during the coming three years according to the ten analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 11% per year, which is not materially different.

In light of this, it's curious that Certara's P/S sits above the majority of other companies. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. Although, additional gains will be difficult to achieve as this level of revenue growth is likely to weigh down the share price eventually.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Given Certara's future revenue forecasts are in line with the wider industry, the fact that it trades at an elevated P/S is somewhat surprising. The fact that the revenue figures aren't setting the world alight has us doubtful that the company's elevated P/S can be sustainable for the long term. A positive change is needed in order to justify the current price-to-sales ratio.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Certara with six simple checks on some of these key factors.

If you're unsure about the strength of Certara's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of revenue growth, the company posted a worthy increase of 5.6%. Pleasingly, revenue has also lifted 35% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

If we review the last year of revenue growth, the company posted a worthy increase of 5.6%. Pleasingly, revenue has also lifted 35% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

如果我們回顧去年的營業收入增長,公司實現了令人滿意的增長爲5.6%。令人高興的是,營業收入從三年前起總共增長了35%,部分得益於過去12個月的增長。因此,股東肯定會對這些中期營業收入增長率表示歡迎。

如果我們回顧去年的營業收入增長,公司實現了令人滿意的增長爲5.6%。令人高興的是,營業收入從三年前起總共增長了35%,部分得益於過去12個月的增長。因此,股東肯定會對這些中期營業收入增長率表示歡迎。