What are the early trends we should look for to identify a stock that could multiply in value over the long term? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Looking at Philip Morris International (NYSE:PM), it does have a high ROCE right now, but lets see how returns are trending.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Philip Morris International is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.31 = US$14b ÷ (US$67b - US$23b) (Based on the trailing twelve months to September 2024).

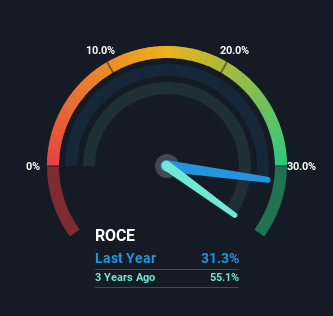

Therefore, Philip Morris International has an ROCE of 31%. That's a fantastic return and not only that, it outpaces the average of 22% earned by companies in a similar industry.

NYSE:PM Return on Capital Employed December 3rd 2024

In the above chart we have measured Philip Morris International's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Philip Morris International .

How Are Returns Trending?

When we looked at the ROCE trend at Philip Morris International, we didn't gain much confidence. While it's comforting that the ROCE is high, five years ago it was 47%. Meanwhile, the business is utilizing more capital but this hasn't moved the needle much in terms of sales in the past 12 months, so this could reflect longer term investments. It may take some time before the company starts to see any change in earnings from these investments.

What We Can Learn From Philip Morris International's ROCE

Bringing it all together, while we're somewhat encouraged by Philip Morris International's reinvestment in its own business, we're aware that returns are shrinking. Yet to long term shareholders the stock has gifted them an incredible 106% return in the last five years, so the market appears to be rosy about its future. However, unless these underlying trends turn more positive, we wouldn't get our hopes up too high.

If you'd like to know about the risks facing Philip Morris International, we've discovered 2 warning signs that you should be aware of.

High returns are a key ingredient to strong performance, so check out our free list ofstocks earning high returns on equity with solid balance sheets.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?擔心內容嗎?直接聯繫我們。或者,發送電子郵件給編輯組(網址爲)simplywallst.com。 Simply Wall St 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

0.31 = US$14b ÷ (US$67b - US$23b)

0.31 = US$14b ÷ (US$67b - US$23b)  0.31 = 140億美元 ÷(670億美元至230億美元)(基於截至2024年9月的過去十二個月)。

0.31 = 140億美元 ÷(670億美元至230億美元)(基於截至2024年9月的過去十二個月)。