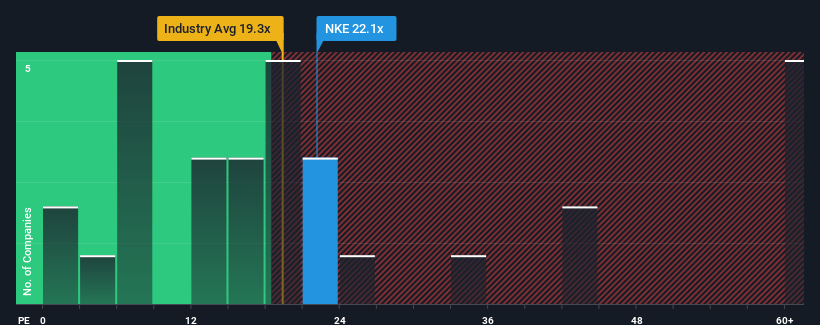

NIKE, Inc.'s (NYSE:NKE) price-to-earnings (or "P/E") ratio of 22.1x might make it look like a sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 19x and even P/E's below 11x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

With earnings growth that's superior to most other companies of late, NIKE has been doing relatively well. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

NYSE:NKE Price to Earnings Ratio vs Industry December 2nd 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on NIKE.

Is There Enough Growth For NIKE?

There's an inherent assumption that a company should outperform the market for P/E ratios like NIKE's to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 7.2% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with EPS shrinking 7.6% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 2.9% each year over the next three years. Meanwhile, the rest of the market is forecast to expand by 11% per year, which is noticeably more attractive.

In light of this, it's alarming that NIKE's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of NIKE's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for NIKE with six simple checks.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 7.2% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with EPS shrinking 7.6% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 7.2% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with EPS shrinking 7.6% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

回顧一下,我們看到公司去年每股收益增長了7.2%。然而,最終它沒能扭轉前一時期的糟糕表現,過去三年每股收益總共下降了7.6%。因此,股東們對中期的收益增長速度感到失望。

回顧一下,我們看到公司去年每股收益增長了7.2%。然而,最終它沒能扭轉前一時期的糟糕表現,過去三年每股收益總共下降了7.6%。因此,股東們對中期的收益增長速度感到失望。