What trends should we look for it we want to identify stocks that can multiply in value over the long term? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. With that in mind, we've noticed some promising trends at Toll Brothers (NYSE:TOL) so let's look a bit deeper.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Toll Brothers:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.19 = US$2.0b ÷ (US$13b - US$2.6b) (Based on the trailing twelve months to July 2024).

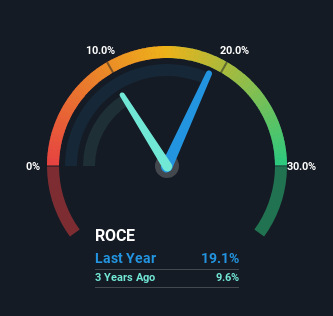

So, Toll Brothers has an ROCE of 19%. On its own, that's a standard return, however it's much better than the 14% generated by the Consumer Durables industry.

NYSE:TOL Return on Capital Employed December 2nd 2024

Above you can see how the current ROCE for Toll Brothers compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Toll Brothers .

What Can We Tell From Toll Brothers' ROCE Trend?

Toll Brothers has not disappointed with their ROCE growth. More specifically, while the company has kept capital employed relatively flat over the last five years, the ROCE has climbed 107% in that same time. Basically the business is generating higher returns from the same amount of capital and that is proof that there are improvements in the company's efficiencies. On that front, things are looking good so it's worth exploring what management has said about growth plans going forward.

The Key Takeaway

To bring it all together, Toll Brothers has done well to increase the returns it's generating from its capital employed. And a remarkable 324% total return over the last five years tells us that investors are expecting more good things to come in the future. Therefore, we think it would be worth your time to check if these trends are going to continue.

One more thing to note, we've identified 1 warning sign with Toll Brothers and understanding it should be part of your investment process.

While Toll Brothers isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?擔心內容嗎?直接聯繫我們。或者,發送電子郵件給編輯組(網址爲)simplywallst.com。 Simply Wall St 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

0.19 = US$2.0b ÷ (US$13b - US$2.6b)

0.19 = US$2.0b ÷ (US$13b - US$2.6b)  0.19 = 20億美元 ÷(130億美元至26億美元)(基於截至2024年7月的過去十二個月)。

0.19 = 20億美元 ÷(130億美元至26億美元)(基於截至2024年7月的過去十二個月)。