Edison International's (NYSE:EIX) Returns On Capital Are Heading Higher

Edison International's (NYSE:EIX) Returns On Capital Are Heading Higher

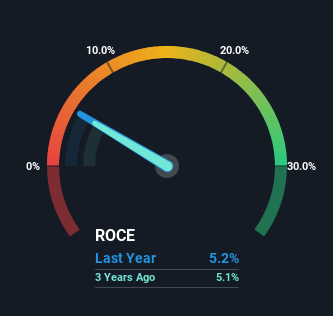

0.052 = US$3.9b ÷ (US$85b - US$8.5b)

0.052 = US$3.9b ÷ (US$85b - US$8.5b) If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Speaking of which, we noticed some great changes in Edison International's (NYSE:EIX) returns on capital, so let's have a look.

如果我們想找到一個潛在的多倍回報股票,通常會有一些潛在趨勢可以提供線索。在完美世界中,我們希望看到一家公司向其業務投資更多的資本,並且理想情況下,從這些資本中賺取的回報也在增加。簡單來說,這些類型的業務是複合增長機器,這意味着他們不斷以越來越高的回報率再投資他們的收益。提到這一點,我們注意到愛迪生國際(紐交所:EIX)在資本回報方面的一些巨大變化,所以讓我們來看一看。

Return On Capital Employed (ROCE): What Is It?

資本利用率(ROCE)是什麼?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Edison International:

爲了澄清如果你不確定,ROCE是一個評估公司在其業務中投資的資本所獲得的稅前收入(以百分比形式)多少的指標。分析師使用這個公式來計算愛迪生國際的ROCE:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

資本利用率 = 利息和稅前利潤(EBIT) ÷ (總資產 - 流動負債)

0.052 = US$3.9b ÷ (US$85b - US$8.5b) (Based on the trailing twelve months to September 2024).

0.052 = 39億美元 ÷ (850億美元 - 85億)(基於截至2024年9月的過去十二個月)

Thus, Edison International has an ROCE of 5.2%. Even though it's in line with the industry average of 4.7%, it's still a low return by itself.

因此,愛迪生國際的資本回報率爲5.2%。儘管這與行業平均水平4.7%相符,但就其本身而言,仍然是較低的回報。

Above you can see how the current ROCE for Edison International compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Edison International .

上面您可以看到愛迪生國際目前的資本回報率(ROCE)與之前的資本回報相比,但從過去只能了解這麼多。如果您想看看分析師對未來的預測,您應該查看我們爲愛迪生國際提供的免費分析師報告。

So How Is Edison International's ROCE Trending?

那麼愛迪生國際的資本回報率(ROCE)趨勢如何?

Even though ROCE is still low in absolute terms, it's good to see it's heading in the right direction. Over the last five years, returns on capital employed have risen substantially to 5.2%. The amount of capital employed has increased too, by 31%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

儘管從絕對值來看,ROCE仍然較低,但看到它朝着正確的方向發展是件好事。在過去五年中,使用資本的回報率大幅上升至5.2%。使用的資本量也增加了31%。在不斷增長的資本基礎上,回報的增加在多重回報投資者中很常見,這就是我們感到印象深刻的原因。

The Bottom Line On Edison International's ROCE

關於愛迪生國際的資本回報率(ROCE)的結論

In summary, it's great to see that Edison International can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. Since the stock has returned a solid 53% to shareholders over the last five years, it's fair to say investors are beginning to recognize these changes. In light of that, we think it's worth looking further into this stock because if Edison International can keep these trends up, it could have a bright future ahead.

總的來說,很高興看到愛迪生國際能夠通過不斷以不斷增長的回報率再投資資本來複合收益,因爲這些是那些備受追捧的多重回報投資者的一些關鍵要素。考慮到過去五年股票爲股東帶來了53%的穩固回報,可以公平地說,投資者開始認識到這些變化。鑑於此,我們認爲值得進一步關注這隻股票,因爲如果愛迪生國際能夠保持這些趨勢,未來可能會非常輝煌。

Edison International does have some risks, we noticed 3 warning signs (and 2 which are a bit unpleasant) we think you should know about.

愛迪生國際確實面臨一些風險,我們注意到3個警告信號(還有2個稍微不太愉快的信號)我們認爲您應該了解。

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

如果您想尋找財務狀況良好、回報卓越的實力強企業,可以免費查看以下公司列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。