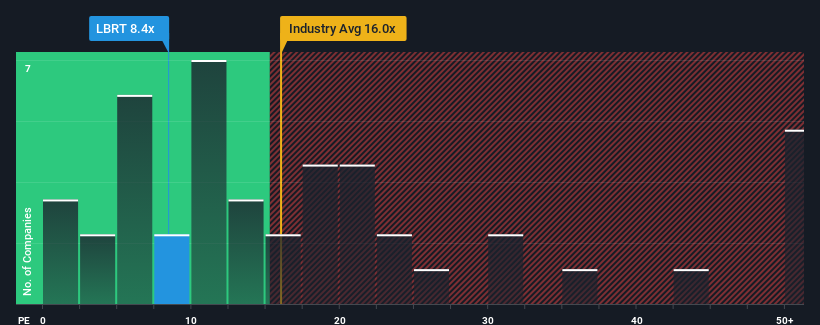

Liberty Energy Inc.'s (NYSE:LBRT) price-to-earnings (or "P/E") ratio of 8.4x might make it look like a strong buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 20x and even P/E's above 36x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Liberty Energy could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

NYSE:LBRT Price to Earnings Ratio vs Industry November 30th 2024 Want the full picture on analyst estimates for the company? Then our free report on Liberty Energy will help you uncover what's on the horizon.

Is There Any Growth For Liberty Energy?

In order to justify its P/E ratio, Liberty Energy would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered a frustrating 39% decrease to the company's bottom line. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 2.1% per year over the next three years. With the market predicted to deliver 11% growth per year, the company is positioned for a weaker earnings result.

With this information, we can see why Liberty Energy is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Bottom Line On Liberty Energy's P/E

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Liberty Energy maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Plus, you should also learn about these 3 warning signs we've spotted with Liberty Energy (including 1 which is a bit concerning).

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Liberty Energy Inc.(紐交所:LBRT)的市盈率爲8.4倍,與美國市場相比,這可能讓它看起來是一個強勁的買入機會,而美國市場大約一半的公司市盈率超過20倍,甚至超過36倍的市盈率也相當普遍。然而,市盈率可能低是有原因的,需要進一步調查以判斷其合理性。

Liberty Energy的表現可能更好,因爲其收益最近一直在下滑,而大多數其他公司則在實現正增長。市盈率可能低是因爲投資者認爲這種糟糕的收益表現不會有所改善。如果你仍然喜歡這家公司,你會希望情況不是這樣,以便你可以在股票被冷落時潛在地買入一些股份。

Retrospectively, the last year delivered a frustrating 39% decrease to the company's bottom line. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Retrospectively, the last year delivered a frustrating 39% decrease to the company's bottom line. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

回顧過去,去年公司底線下降了令人沮喪的39%。 至少得益於早期的增長,每股收益在整體上未完全倒退於三年前。 因此,可以公平地說,最近公司的盈利增長一直不穩定。

回顧過去,去年公司底線下降了令人沮喪的39%。 至少得益於早期的增長,每股收益在整體上未完全倒退於三年前。 因此,可以公平地說,最近公司的盈利增長一直不穩定。