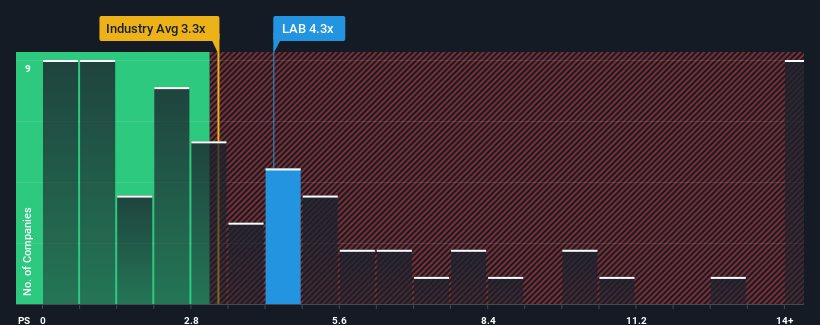

When close to half the companies in the Life Sciences industry in the United States have price-to-sales ratios (or "P/S") below 3.3x, you may consider Standard BioTools Inc. (NASDAQ:LAB) as a stock to potentially avoid with its 4.3x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

NasdaqGS:LAB Price to Sales Ratio vs Industry November 29th 2024

What Does Standard BioTools' Recent Performance Look Like?

Recent times have been advantageous for Standard BioTools as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Standard BioTools.

What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Standard BioTools' to be considered reasonable.

Retrospectively, the last year delivered an exceptional 48% gain to the company's top line. As a result, it also grew revenue by 14% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 17% per year during the coming three years according to the three analysts following the company. That's shaping up to be materially higher than the 7.1% per year growth forecast for the broader industry.

With this information, we can see why Standard BioTools is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What Does Standard BioTools' P/S Mean For Investors?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our look into Standard BioTools shows that its P/S ratio remains high on the merit of its strong future revenues. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless these conditions change, they will continue to provide strong support to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Standard BioTools (at least 1 which is a bit unpleasant), and understanding them should be part of your investment process.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered an exceptional 48% gain to the company's top line. As a result, it also grew revenue by 14% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Retrospectively, the last year delivered an exceptional 48% gain to the company's top line. As a result, it also grew revenue by 14% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

回顧過去一年,公司營業收入增長了令人矚目的48%。因此,過去三年總體上收入增長了14%。因此,我們可以開始確認公司在那段時間內實際上在增長營業收入方面做得很好。

回顧過去一年,公司營業收入增長了令人矚目的48%。因此,過去三年總體上收入增長了14%。因此,我們可以開始確認公司在那段時間內實際上在增長營業收入方面做得很好。