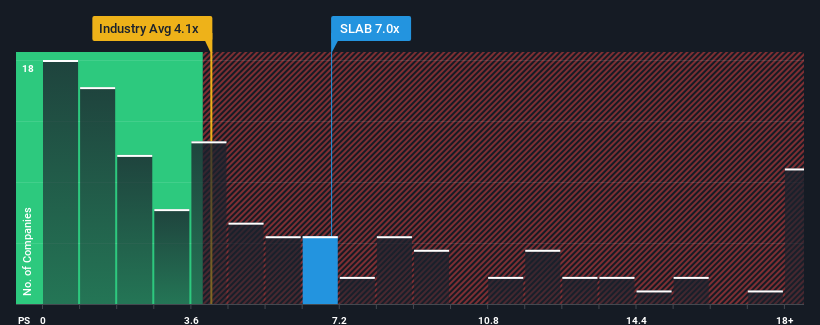

With a price-to-sales (or "P/S") ratio of 7x Silicon Laboratories Inc. (NASDAQ:SLAB) may be sending very bearish signals at the moment, given that almost half of all the Semiconductor companies in the United States have P/S ratios under 4.1x and even P/S lower than 1.5x are not unusual. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

NasdaqGS:SLAB Price to Sales Ratio vs Industry November 28th 2024

What Does Silicon Laboratories' P/S Mean For Shareholders?

Silicon Laboratories could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the market is expecting the poor revenue to reverse, justifying it's current high P/S.. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on Silicon Laboratories will help you uncover what's on the horizon.

How Is Silicon Laboratories' Revenue Growth Trending?

In order to justify its P/S ratio, Silicon Laboratories would need to produce outstanding growth that's well in excess of the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 47%. The last three years don't look nice either as the company has shrunk revenue by 23% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Shifting to the future, estimates from the eight analysts covering the company suggest revenue should grow by 48% over the next year. With the industry only predicted to deliver 40%, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Silicon Laboratories' P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Silicon Laboratories' analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Silicon Laboratories, and understanding should be part of your investment process.

If you're unsure about the strength of Silicon Laboratories' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 47%. The last three years don't look nice either as the company has shrunk revenue by 23% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 47%. The last three years don't look nice either as the company has shrunk revenue by 23% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

首先回顧一下,去年公司的營業收入增長並不令人興奮,因爲它錄得了令人失望的下降47%。 過去三年的情況也不容樂觀,公司已經累計減少了23%的營業收入。 因此,不幸的是,我們必須承認該公司在這段時間內並沒有做出很好的營收增長。

首先回顧一下,去年公司的營業收入增長並不令人興奮,因爲它錄得了令人失望的下降47%。 過去三年的情況也不容樂觀,公司已經累計減少了23%的營業收入。 因此,不幸的是,我們必須承認該公司在這段時間內並沒有做出很好的營收增長。