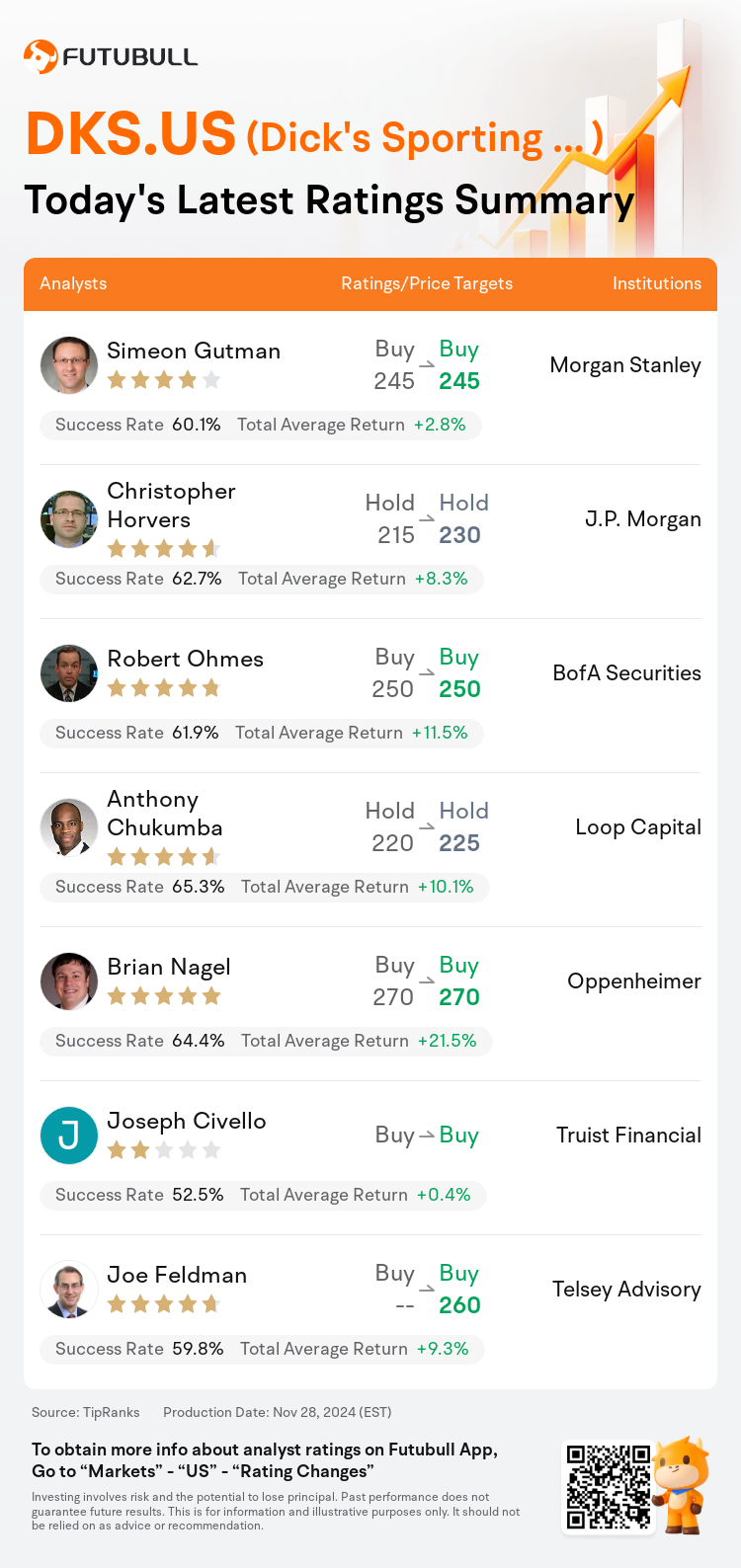

On Nov 28, major Wall Street analysts update their ratings for $Dick's Sporting Goods (DKS.US)$, with price targets ranging from $225 to $270.

Morgan Stanley analyst Simeon Gutman maintains with a buy rating, and maintains the target price at $245.

J.P. Morgan analyst Christopher Horvers maintains with a hold rating, and adjusts the target price from $215 to $230.

BofA Securities analyst Robert Ohmes maintains with a buy rating, and maintains the target price at $250.

BofA Securities analyst Robert Ohmes maintains with a buy rating, and maintains the target price at $250.

Loop Capital analyst Anthony Chukumba maintains with a hold rating, and adjusts the target price from $220 to $225.

Oppenheimer analyst Brian Nagel maintains with a buy rating, and maintains the target price at $270.

Furthermore, according to the comprehensive report, the opinions of $Dick's Sporting Goods (DKS.US)$'s main analysts recently are as follows:

Dick's Sporting is poised to generate more sustainable earnings growth moving forward compared to its historical performance, which has not yet been fully reflected in its stock value. Analysts forecast an 8% annual earnings growth over the next five years, contrasting with a 5% average growth in the five years before the pandemic. Recent structural improvements in the company are expected to yield benefits in the form of higher margins, enhanced free cash flow generation, and increased returns for the foreseeable future.

Dick's Sporting excelled in its third quarter, achieving a third consecutive quarter with over 4% in comparable sales growth, surpassing earnings expectations, and raising its 2024 guidance for the third time this fiscal year.

Execution in Q3 was again characterized by strong comp and gross margin performance. Although revenue and EPS projections are again revised upwards, significant capital investments for the rollout of the House of Sport and tighter free cash flow remain cautionary factors regarding valuation.

Here are the latest investment ratings and price targets for $Dick's Sporting Goods (DKS.US)$ from 7 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

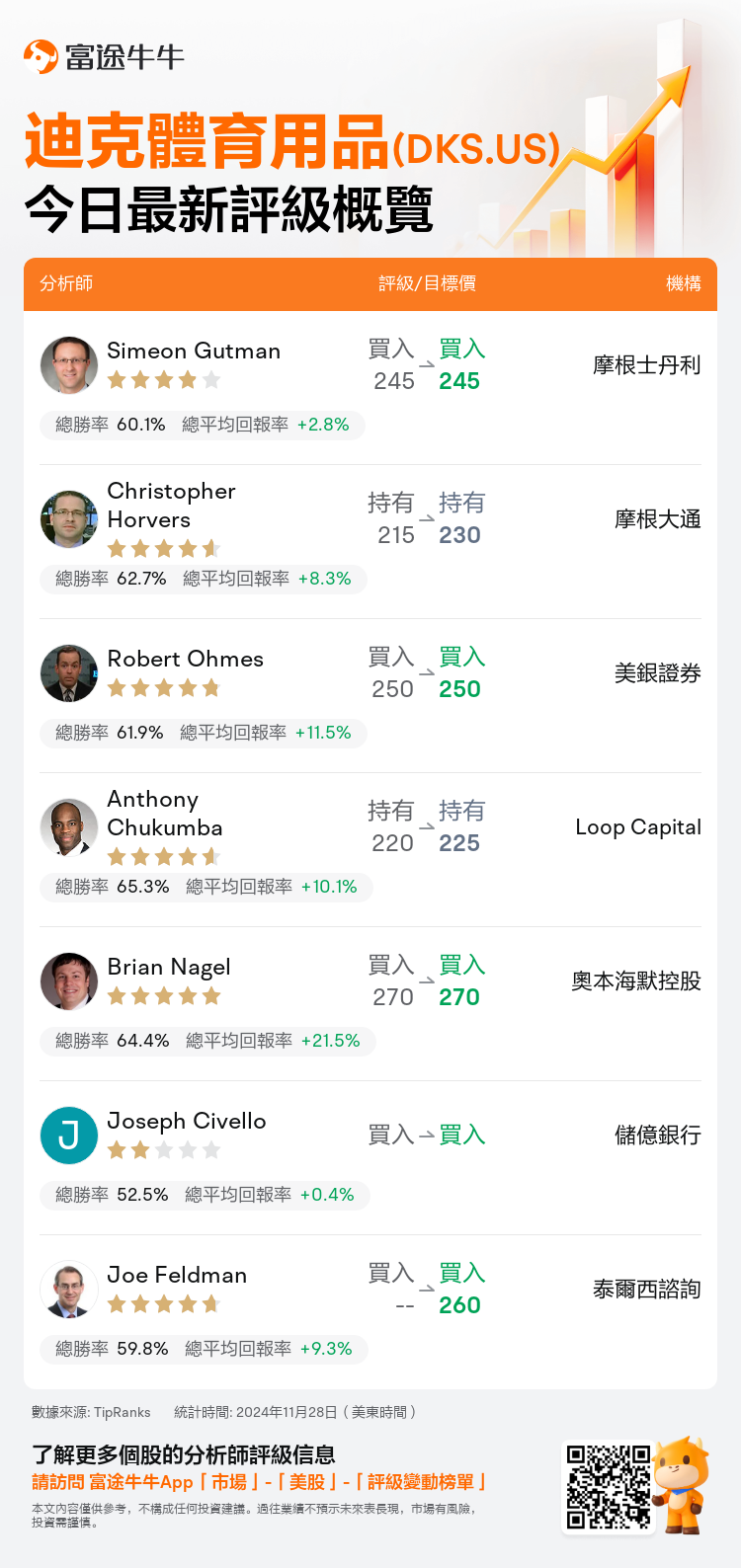

美東時間11月28日,多家華爾街大行更新了$迪克體育用品 (DKS.US)$的評級,目標價介於225美元至270美元。

摩根士丹利分析師Simeon Gutman維持買入評級,維持目標價245美元。

摩根大通分析師Christopher Horvers維持持有評級,並將目標價從215美元上調至230美元。

美銀證券分析師Robert Ohmes維持買入評級,維持目標價250美元。

美銀證券分析師Robert Ohmes維持買入評級,維持目標價250美元。

Loop Capital分析師Anthony Chukumba維持持有評級,並將目標價從220美元上調至225美元。

奧本海默控股分析師Brian Nagel維持買入評級,維持目標價270美元。

此外,綜合報道,$迪克體育用品 (DKS.US)$近期主要分析師觀點如下:

迪克體育有望在未來實現更可持續的盈利增長,相較於其歷史表現,這一點尚未完全反映在其股票價值中。分析師預測未來五年的年盈利增長將達到8%,而疫情前五年的平均增長僅爲5%。公司近期的結構性改善預計將帶來更高的毛利率、增強的自由現金流生成,以及在可預見的未來增加的回報。

迪克體育在第三季度表現出色,實現了連續第三個季度超過4%的可比銷售增長,超出了盈利預期,並且在本財年第三次上調2024年的指導。

第三季度的執行再次表現出強勁的可比銷售和毛利率表現。儘管營業收入和每股收益的預測再次上調,但爲了推出運動之家而進行的大規模資本投資以及緊縮的自由現金流仍然是對估值的警示因素。

以下爲今日7位分析師對$迪克體育用品 (DKS.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。