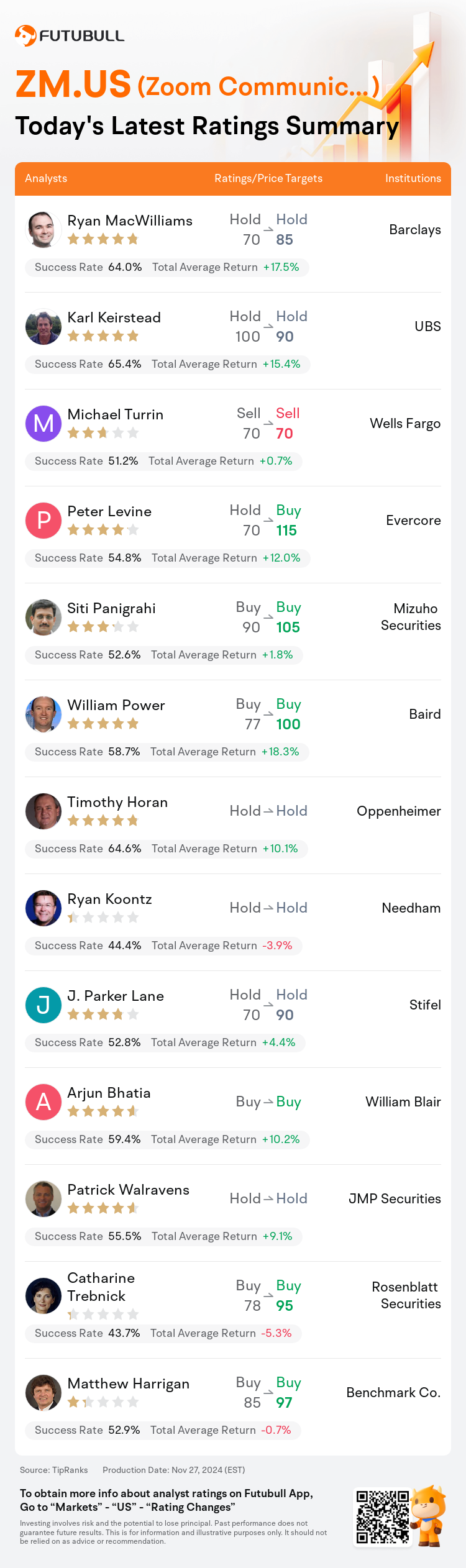

On Nov 27, major Wall Street analysts update their ratings for $Zoom Communications (ZM.US)$, with price targets ranging from $70 to $115.

Barclays analyst Ryan MacWilliams maintains with a hold rating, and adjusts the target price from $70 to $85.

UBS analyst Karl Keirstead maintains with a hold rating, and adjusts the target price from $100 to $90.

Wells Fargo analyst Michael Turrin maintains with a sell rating, and maintains the target price at $70.

Wells Fargo analyst Michael Turrin maintains with a sell rating, and maintains the target price at $70.

Evercore analyst Peter Levine upgrades to a buy rating, and adjusts the target price from $70 to $115.

Mizuho Securities analyst Siti Panigrahi maintains with a buy rating, and adjusts the target price from $90 to $105.

Furthermore, according to the comprehensive report, the opinions of $Zoom Communications (ZM.US)$'s main analysts recently are as follows:

Investors are more confident that Zoom Communications has found stabilization within its core business, although there remains a desire for a stronger revenue or operational margin improvement in Q3.

Zoom Communications has indicated an emphasis on speeding up growth, yet it remains uncertain if the Q3 results will instill confidence in a significant acceleration for fiscal year 2026. The projection of a 3% revenue growth for Q4, and the mention of this figure as an initial 'placeholder' for FY26 growth projections, may not support arguments for a substantial growth pivot, despite a cautious stance from the company.

Zoom Communications' recent Q3 report was noted for its predictability, continuing to focus on expanding the platform to boost customer value and engagement, which remains a critical strategic priority. This strategy aims to facilitate re-accelerated growth, supported by stability in the Online segment and enhanced Enterprise upsell opportunities.

After Q3 results surpassed expectations, Zoom Video's forward outlook included Q4 revenue expectations slightly above consensus. Initial guidance for FY26 showing a 2.7% revenue growth falls below broader market expectations of 3.2%. This conservative projection could potentially set a baseline for the performance expected of the new CFO.

Zoom Communications reported strong Q3 results, continuing to deliver "best-in-class" profitability and cash flow as the management drives towards revenue reacceleration. It is expected that the company will return to mid-single-digit growth due to stabilization in the core platform and growth impetus from emerging products.

Here are the latest investment ratings and price targets for $Zoom Communications (ZM.US)$ from 13 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

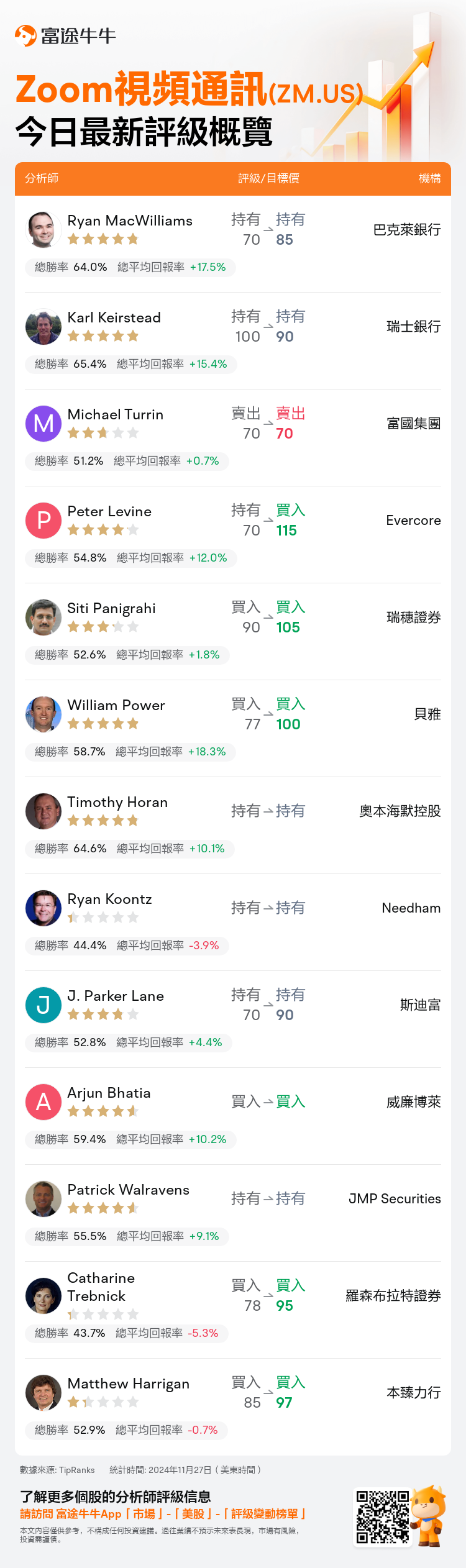

美東時間11月27日,多家華爾街大行更新了$Zoom視頻通訊 (ZM.US)$的評級,目標價介於70美元至115美元。

巴克萊銀行分析師Ryan MacWilliams維持持有評級,並將目標價從70美元上調至85美元。

瑞士銀行分析師Karl Keirstead維持持有評級,並將目標價從100美元下調至90美元。

富國集團分析師Michael Turrin維持賣出評級,維持目標價70美元。

富國集團分析師Michael Turrin維持賣出評級,維持目標價70美元。

Evercore分析師Peter Levine上調至買入評級,並將目標價從70美元上調至115美元。

瑞穗證券分析師Siti Panigrahi維持買入評級,並將目標價從90美元上調至105美元。

此外,綜合報道,$Zoom視頻通訊 (ZM.US)$近期主要分析師觀點如下:

投資者對Zoom通信在其核心業務中找到穩定性更加信心十足,儘管仍然希望在第三季度能有更強的營業收入或運營利潤改善。

Zoom通信已表示將重點加速增長,但第三季度的結果是否能增強對2026財年顯著加速的信心仍然不確定。第四季度3%的營業收入增長預期,以及將該數據作爲2026財年增長預期的初步「佔位符」的提及,可能無法支持對顯著增長轉變的論點,儘管公司採取了謹慎的態度。

Zoom通信最近的第三季度報告因其可預測性而引人注目,繼續專注於擴大平台以提升客戶價值和參與度,這仍然是一個關鍵的策略優先事項。該策略旨在促進重新加速的增長,得益於在線領域的穩定和增強的企業增銷機會。

在第三季度的結果超出預期後,Zoom視頻的前瞻性展望包括第四季度營業收入預期略高於市場共識。2026財年初步指引顯示2.7%的營業收入增長,低於市場普遍預期的3.2%。這一保守預測可能爲新任首席財務官預計的業績設定了基準。

Zoom通信報告了強勁的第三季度業績,繼續實現「最佳同行」的盈利能力和現金流,因爲管理層推動營業收入重新加速。預計公司將在覈心平台穩定及新興產品推動下恢復中等個位數的增長。

以下爲今日13位分析師對$Zoom視頻通訊 (ZM.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。