Here's Why Central Garden & Pet (NASDAQ:CENT) Can Manage Its Debt Responsibly

Here's Why Central Garden & Pet (NASDAQ:CENT) Can Manage Its Debt Responsibly

Zooming in on the latest balance sheet data, we can see that Central Garden & Pet had liabilities of US$515.4m due within 12 months and liabilities of US$1.48b due beyond that. Offsetting this, it had US$753.6m in cash and US$326.2m in receivables that were due within 12 months. So it has liabilities totalling US$916.1m more than its cash and near-term receivables, combined.

Zooming in on the latest balance sheet data, we can see that Central Garden & Pet had liabilities of US$515.4m due within 12 months and liabilities of US$1.48b due beyond that. Offsetting this, it had US$753.6m in cash and US$326.2m in receivables that were due within 12 months. So it has liabilities totalling US$916.1m more than its cash and near-term receivables, combined. Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Central Garden & Pet Company (NASDAQ:CENT) does have debt on its balance sheet. But is this debt a concern to shareholders?

霍華德·馬克斯說得很好,與其擔心股價波動,不如關心永久性損失的可能性…我認識的每位實踐投資者都很擔心這一點。因此,明智的投資者知道,債務是破產時通常涉及的一個非常重要的因素,當評估公司的風險時。我們注意到中央花園與寵物公司(NASDAQ:CENT)的資產負債表上確實有債務。但這些債務會讓股東感到擔憂嗎?

When Is Debt A Problem?

什麼時候負債才是一個問題?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

債務是幫助企業增長的工具,但如果企業無力償還債權人,那麼企業就處於他們的掌控之下。資本主義的重要組成部分之一是「創造性破壞」的過程,失敗的企業被銀行家無情地清算。然而,更頻繁的(但仍然代價高昂的)情況是,一家公司必須以低廉的價格發行股票,永久性地稀釋股東權益,以此來支撐其資產負債表。當然,債務可以是企業的重要工具,特別是對於資本密集型企業來說。在考慮公司的債務水平時,第一步是將其現金和債務合併考慮。

How Much Debt Does Central Garden & Pet Carry?

中央花園與寵物公司攜帶多少債務?

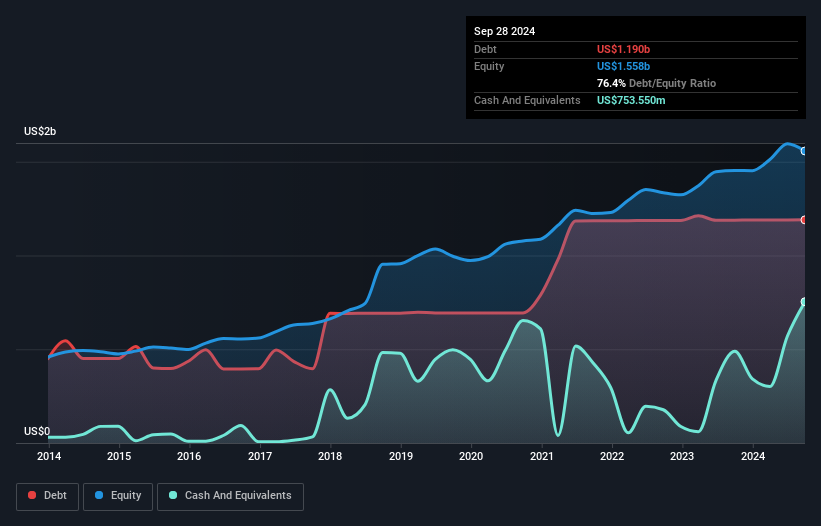

The chart below, which you can click on for greater detail, shows that Central Garden & Pet had US$1.19b in debt in September 2024; about the same as the year before. On the flip side, it has US$753.6m in cash leading to net debt of about US$436.5m.

下面的圖表顯示,中央花園與寵物公司在2024年9月有11.9億美元的債務;與前一年大致相同。另一方面,其現金爲75360萬美元,淨債務約爲43650萬美元。

How Strong Is Central Garden & Pet's Balance Sheet?

中央花園與寵物的資產負債表有多強?

Zooming in on the latest balance sheet data, we can see that Central Garden & Pet had liabilities of US$515.4m due within 12 months and liabilities of US$1.48b due beyond that. Offsetting this, it had US$753.6m in cash and US$326.2m in receivables that were due within 12 months. So it has liabilities totalling US$916.1m more than its cash and near-term receivables, combined.

深入了解最新的資產負債表數據,我們可以看到,中央花園與寵物在未來12個月內有51540萬美元的負債,而12個月後到期的負債爲14.8億美元。 抵消這一點,它擁有75360萬美元的現金和32620萬美元的應收賬款,這些應收賬款在未來12個月內到期。 因此,它的負債總額超過現金和短期應收賬款合計91610萬美元。

This deficit isn't so bad because Central Garden & Pet is worth US$2.30b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

這個赤字並不太糟糕,因爲中央花園與寵物價值23億美元,因此如果有需要,可能可以籌集足夠的資金來穩固其資產負債表。 但很明顯,我們肯定需要仔細檢查它是否能夠在不稀釋股權的情況下管理債務。

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

我們通過將公司的淨債務與其息稅折舊攤銷前利潤(EBITDA)相除,並計算其息稅前利潤(EBIT)如何覆蓋其利息費用(利息覆蓋率)來衡量公司的債務負擔相對於其盈利能力。因此,我們同時考慮債務的絕對數量以及所支付的利率。

Central Garden & Pet's net debt is sitting at a very reasonable 1.5 times its EBITDA, while its EBIT covered its interest expense just 5.1 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. The bad news is that Central Garden & Pet saw its EBIT decline by 16% over the last year. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Central Garden & Pet can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

中央花園與寵物的淨負債帳戶很合理地爲其EBITDA的1.5倍,而其稅前利潤僅爲去年的5.1倍。 雖然這些數字並沒有引起我們的警覺,但值得注意的是公司債務成本確實產生了實質影響。 不好的消息是,中央花園與寵物的稅前利潤在過去一年中下降了16%。 如果收入繼續以這個速度下降,那麼處理債務就會比帶着三個5歲以下的孩子去一個花哨的餐廳更困難。 毫無疑問,我們從資產負債表上可以了解大部分關於債務的信息。 但最終業務的未來盈利能力將決定中央花園與寵物是否能夠隨着時間加強其資產負債表。 所以,如果您想知道專業人士的看法,您可能會發現分析師盈利預測的免費報告很有趣。

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Central Garden & Pet recorded free cash flow worth 77% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

最後,企業需要有足夠的自由現金流來償還債務;會計利潤並不能解決問題。 因此,我們總是檢查EBIT中有多少被轉化爲自由現金流。 在過去三年中,中央花園與寵物的自由現金流佔其EBIT的77%,這是正常水平,考慮到自由現金流不包括利息和稅金。 這筆實打實的現金意味着它可以在需要時減少債務。

Our View

我們的觀點

On our analysis Central Garden & Pet's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. To be specific, it seems about as good at (not) growing its EBIT as wet socks are at keeping your feet warm. When we consider all the factors mentioned above, we do feel a bit cautious about Central Garden & Pet's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 1 warning sign with Central Garden & Pet , and understanding them should be part of your investment process.

根據我們的分析,中央園林與寵物將EBIt轉化爲自由現金流,這表明公司在償還債務方面可能不會遇到太多困難。然而,我們的其他觀察結果並不那麼令人振奮。具體而言,公司在EBIt的增長方面表現似乎和溼襪子保暖腳一樣好。 考慮到以上提到的所有因素,我們對中央園林與寵物公司的債務使用感到有些謹慎。雖然債務在潛在回報率方面有其優勢,但我們認爲股東們肯定應該考慮債務水平可能如何使股票更具風險。毫無疑問,我們從資產負債表上了解債務情況最多。但最終,每家公司都可能存在超出資產負債表範圍的風險。 我們已經發現了中央園林與寵物公司的一個警示信號,理解它們應該是您投資過程的一部分。

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

如果在所有這些之後,您更感興趣的是具有堅實資產負債表的快速增長公司,那麼不要拖延,查看我們的淨現金增長股票列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。