Interface, Inc. (NASDAQ:TILE) shareholders have had their patience rewarded with a 47% share price jump in the last month. The annual gain comes to 166% following the latest surge, making investors sit up and take notice.

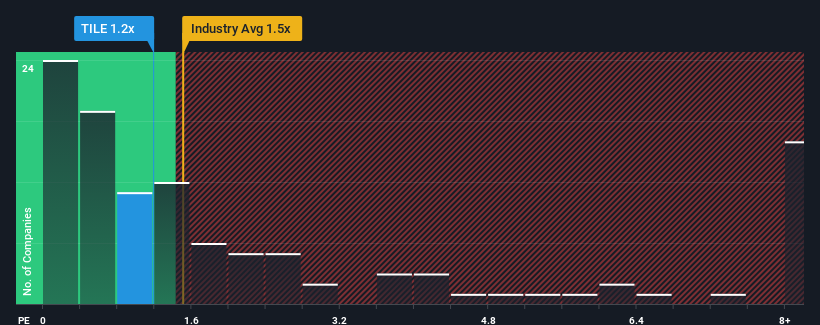

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Interface's P/S ratio of 1.2x, since the median price-to-sales (or "P/S") ratio for the Commercial Services industry in the United States is also close to 1.5x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

NasdaqGS:TILE Price to Sales Ratio vs Industry November 26th 2024

How Interface Has Been Performing

With revenue growth that's inferior to most other companies of late, Interface has been relatively sluggish. One possibility is that the P/S ratio is moderate because investors think this lacklustre revenue performance will turn around. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Interface.

Is There Some Revenue Growth Forecasted For Interface?

The only time you'd be comfortable seeing a P/S like Interface's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a decent 2.6% gain to the company's revenues. The solid recent performance means it was also able to grow revenue by 15% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 3.9% as estimated by the three analysts watching the company. That's shaping up to be materially lower than the 8.7% growth forecast for the broader industry.

In light of this, it's curious that Interface's P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

The Bottom Line On Interface's P/S

Its shares have lifted substantially and now Interface's P/S is back within range of the industry median. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Given that Interface's revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Before you settle on your opinion, we've discovered 3 warning signs for Interface that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Interface, Inc. (納斯達克:TILE) 的股東在過去一個月中因其股價上漲了 47% 而感到滿意。最新的上漲使得年度收益達到了 166%,讓投資者不得不注意。

The only time you'd be comfortable seeing a P/S like Interface's is when the company's growth is tracking the industry closely.

The only time you'd be comfortable seeing a P/S like Interface's is when the company's growth is tracking the industry closely.

只有在公司增長與行業板塊密切相關時,你才會覺得看到Interface這樣的市銷率會比較安心。

只有在公司增長與行業板塊密切相關時,你才會覺得看到Interface這樣的市銷率會比較安心。