Barinthus Biotherapeutics plc (NASDAQ:BRNS) shareholders won't be pleased to see that the share price has had a very rough month, dropping 35% and undoing the prior period's positive performance. For any long-term shareholders, the last month ends a year to forget by locking in a 66% share price decline.

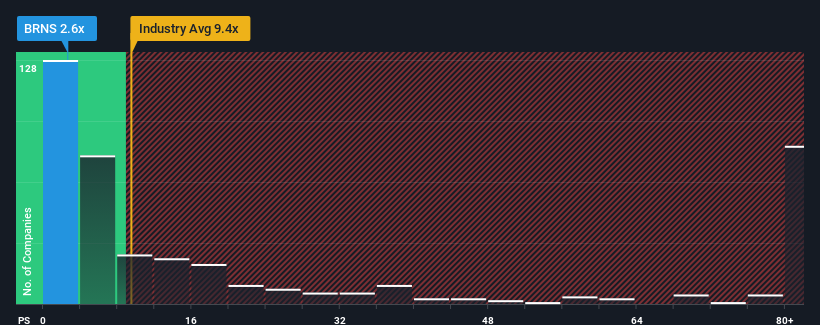

After such a large drop in price, Barinthus Biotherapeutics may look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 2.6x, considering almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 9.4x and even P/S higher than 61x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

NasdaqGM:BRNS Price to Sales Ratio vs Industry November 26th 2024

What Does Barinthus Biotherapeutics' P/S Mean For Shareholders?

Barinthus Biotherapeutics could be doing better as it's been growing revenue less than most other companies lately. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Barinthus Biotherapeutics.

Is There Any Revenue Growth Forecasted For Barinthus Biotherapeutics?

The only time you'd be truly comfortable seeing a P/S as depressed as Barinthus Biotherapeutics' is when the company's growth is on track to lag the industry decidedly.

Retrospectively, the last year delivered an exceptional 106% gain to the company's top line. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 83% as estimated by the three analysts watching the company. That's not great when the rest of the industry is expected to grow by 80%.

In light of this, it's understandable that Barinthus Biotherapeutics' P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Bottom Line On Barinthus Biotherapeutics' P/S

Having almost fallen off a cliff, Barinthus Biotherapeutics' share price has pulled its P/S way down as well. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

With revenue forecasts that are inferior to the rest of the industry, it's no surprise that Barinthus Biotherapeutics' P/S is on the lower end of the spectrum. As other companies in the industry are forecasting revenue growth, Barinthus Biotherapeutics' poor outlook justifies its low P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

There are also other vital risk factors to consider and we've discovered 5 warning signs for Barinthus Biotherapeutics (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The only time you'd be truly comfortable seeing a P/S as depressed as Barinthus Biotherapeutics' is when the company's growth is on track to lag the industry decidedly.

The only time you'd be truly comfortable seeing a P/S as depressed as Barinthus Biotherapeutics' is when the company's growth is on track to lag the industry decidedly.

只有在公司增長明顯落後於行業板塊時,您才會對巴林圖斯生物治療公司的市銷率如此低感到真正舒適。

只有在公司增長明顯落後於行業板塊時,您才會對巴林圖斯生物治療公司的市銷率如此低感到真正舒適。