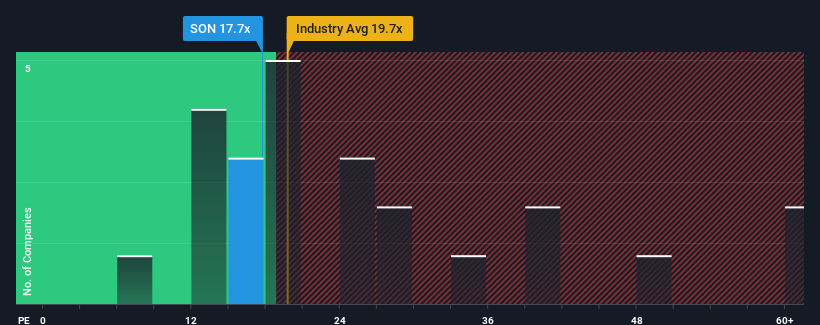

It's not a stretch to say that Sonoco Products Company's (NYSE:SON) price-to-earnings (or "P/E") ratio of 17.7x right now seems quite "middle-of-the-road" compared to the market in the United States, where the median P/E ratio is around 20x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Sonoco Products hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

NYSE:SON Price to Earnings Ratio vs Industry November 26th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Sonoco Products.

Does Growth Match The P/E?

In order to justify its P/E ratio, Sonoco Products would need to produce growth that's similar to the market.

Retrospectively, the last year delivered a frustrating 41% decrease to the company's bottom line. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next year should generate growth of 55% as estimated by the seven analysts watching the company. That's shaping up to be materially higher than the 15% growth forecast for the broader market.

In light of this, it's curious that Sonoco Products' P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Sonoco Products currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Sonoco Products (at least 1 which shouldn't be ignored), and understanding these should be part of your investment process.

If you're unsure about the strength of Sonoco Products' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a frustrating 41% decrease to the company's bottom line. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Retrospectively, the last year delivered a frustrating 41% decrease to the company's bottom line. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

回顧過去一年,公司的底線損失 frustrating 41%。這已經抹去了過去三年的任何盈利,EPS 幾乎沒有發生總體變化。因此,股東可能對不穩定的中期增長率並不滿意。

回顧過去一年,公司的底線損失 frustrating 41%。這已經抹去了過去三年的任何盈利,EPS 幾乎沒有發生總體變化。因此,股東可能對不穩定的中期增長率並不滿意。