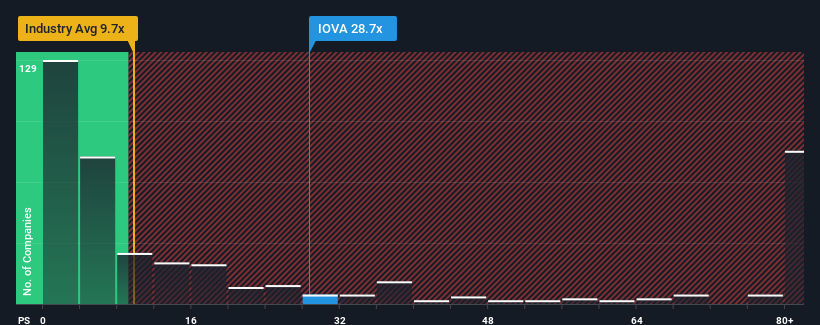

With a price-to-sales (or "P/S") ratio of 28.7x Iovance Biotherapeutics, Inc. (NASDAQ:IOVA) may be sending very bearish signals at the moment, given that almost half of all the Biotechs companies in the United States have P/S ratios under 9.6x and even P/S lower than 3x are not unusual. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

NasdaqGM:IOVA Price to Sales Ratio vs Industry November 24th 2024

How Has Iovance Biotherapeutics Performed Recently?

With revenue growth that's superior to most other companies of late, Iovance Biotherapeutics has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. If not, then existing shareholders might be a little nervous about the viability of the share price.

Keen to find out how analysts think Iovance Biotherapeutics' future stacks up against the industry? In that case, our free report is a great place to start.

Is There Enough Revenue Growth Forecasted For Iovance Biotherapeutics?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Iovance Biotherapeutics' to be considered reasonable.

Taking a look back first, we see that the company's revenues underwent some rampant growth over the last 12 months. Although, its longer-term performance hasn't been anywhere near as strong with three-year revenue growth being relatively non-existent overall. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Turning to the outlook, the next three years should generate growth of 118% per annum as estimated by the analysts watching the company. That's shaping up to be similar to the 118% per annum growth forecast for the broader industry.

With this in consideration, we find it intriguing that Iovance Biotherapeutics' P/S is higher than its industry peers. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for disappointment if the P/S falls to levels more in line with the growth outlook.

The Final Word

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Analysts are forecasting Iovance Biotherapeutics' revenues to only grow on par with the rest of the industry, which has lead to the high P/S ratio being unexpected. When we see revenue growth that just matches the industry, we don't expect elevates P/S figures to remain inflated for the long-term. Unless the company can jump ahead of the rest of the industry in the short-term, it'll be a challenge to maintain the share price at current levels.

Plus, you should also learn about this 1 warning sign we've spotted with Iovance Biotherapeutics.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company's revenues underwent some rampant growth over the last 12 months. Although, its longer-term performance hasn't been anywhere near as strong with three-year revenue growth being relatively non-existent overall. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Taking a look back first, we see that the company's revenues underwent some rampant growth over the last 12 months. Although, its longer-term performance hasn't been anywhere near as strong with three-year revenue growth being relatively non-existent overall. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

先回顧一下,我們可以看到該公司的營業收入在過去12個月內經歷了一段猛烈增長。儘管在較長時間內,該公司的表現並不強勁,三年的營業收入增長基本上不存在。因此,可以說該公司的營業收入增長最近並不一致。

先回顧一下,我們可以看到該公司的營業收入在過去12個月內經歷了一段猛烈增長。儘管在較長時間內,該公司的表現並不強勁,三年的營業收入增長基本上不存在。因此,可以說該公司的營業收入增長最近並不一致。