Drilling Tools International's (NASDAQ:DTI) Anemic Earnings Might Be Worse Than You Think

Drilling Tools International's (NASDAQ:DTI) Anemic Earnings Might Be Worse Than You Think

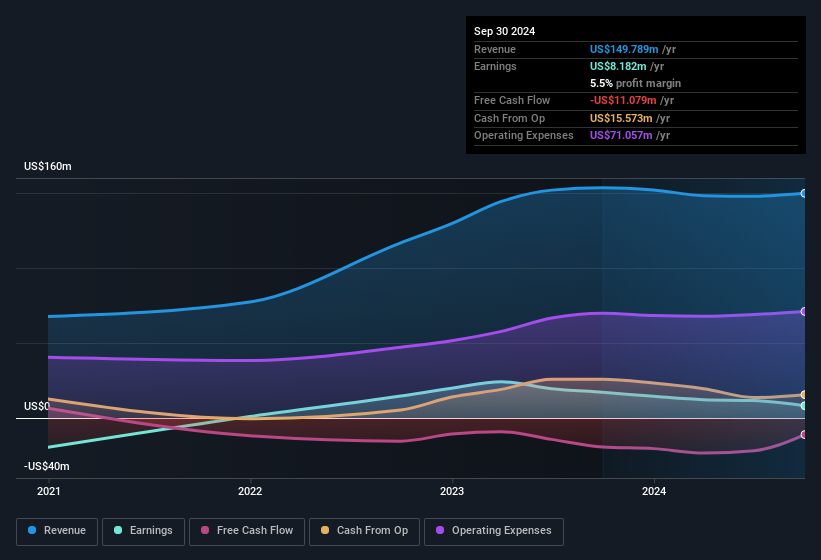

In the long term, if Drilling Tools International's earnings

In the long term, if Drilling Tools International's earnings A lackluster earnings announcement from Drilling Tools International Corporation (NASDAQ:DTI) last week didn't sink the stock price. However, we believe that investors should be aware of some underlying factors which may be of concern.

上週,來自納斯達克公司(DTI)的鑽井工具國際公司發佈了一份平淡的收益公告,並未使股價下跌。然而,我們認爲投資者應該注意一些潛在的令人擔憂的因素。

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. As it happens, Drilling Tools International issued 17% more new shares over the last year. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of Drilling Tools International's EPS by clicking here.

評估收益質量的一個重要方面是看一家公司對股東的稀釋程度。事實上,鑽井工具國際在過去一年中發行了更多的新股,比去年增加了17%。這意味着其收益分配給了更多的股東。每股指標如EPS有助於我們了解實際股東從公司利潤中受益的程度,而淨收入水平則幫助我們更好地了解公司的絕對規模。點擊這裏,您可以看到鑽井工具國際的EPS圖表。

How Is Dilution Impacting Drilling Tools International's Earnings Per Share (EPS)?

稀釋對鑽井工具國際的每股收益(EPS)有何影響?

Drilling Tools International was losing money three years ago. And even focusing only on the last twelve months, we see profit is down 52%. Sadly, earnings per share fell further, down a full 74% in that time. Therefore, the dilution is having a noteworthy influence on shareholder returns.

三年前,鑽井工具國際曾虧損。即使僅關注過去十二個月,我們也看到利潤下降了52%。遺憾的是,每股收益進一步下降,該時間段下降了整整74%。因此,稀釋對股東回報產生了顯著影響。

In the long term, if Drilling Tools International's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

從長期來看,如果鑽井工具國際的每股收益能夠增加,股價也應該隨之增長。但另一方面,我們將對了解即使利潤在提高(但EPS沒有)感到遠不如以前激動。因此,您可以說在長期內,EPS比淨利潤更爲重要,假設目標是評估公司的股價是否可能增長。

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

這可能會讓您想知道分析師對未來盈利能力的預測。幸運的是,您可以單擊此處查看基於其估計的未來盈利能力的互動圖表。

Our Take On Drilling Tools International's Profit Performance

關於Drilling Tools International的利潤表現我們的觀點

Drilling Tools International issued shares during the year, and that means its EPS performance lags its net income growth. Because of this, we think that it may be that Drilling Tools International's statutory profits are better than its underlying earnings power. Sadly, its EPS was down over the last twelve months. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Case in point: We've spotted 2 warning signs for Drilling Tools International you should be aware of.

Drilling Tools International在本年度發行股份,這意味着其每股收益表現落後於淨利潤增長。由於這一點,我們認爲Drilling Tools International的法定利潤可能優於其潛在盈利力。遺憾的是,其每股收益在過去十二個月內下降。這篇文章的目標是評估我們能否依靠法定收益反映公司潛力,但還有很多需要考慮的因素。考慮到這一點,如果你想對該公司進行更多分析,了解所涉風險非常重要。舉例說明:我們發現Drilling Tools International存在兩個警示信號,您應該注意。

Today we've zoomed in on a single data point to better understand the nature of Drilling Tools International's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

今天我們聚焦於單一數據點,以更好地了解Drilling Tools International的利潤性質。但如果您有能力專注於細微之處,還有更多可以發現的內容。有些人認爲高股本回報率是質量企業的良好標誌。因此,您可能希望查看這些擁有高股本回報率的公司的免費收藏,或者這些擁有高內部持股比例的股票清單。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。