On Nov 20, major Wall Street analysts update their ratings for $Valvoline (VVV.US)$, with price targets ranging from $42 to $46.

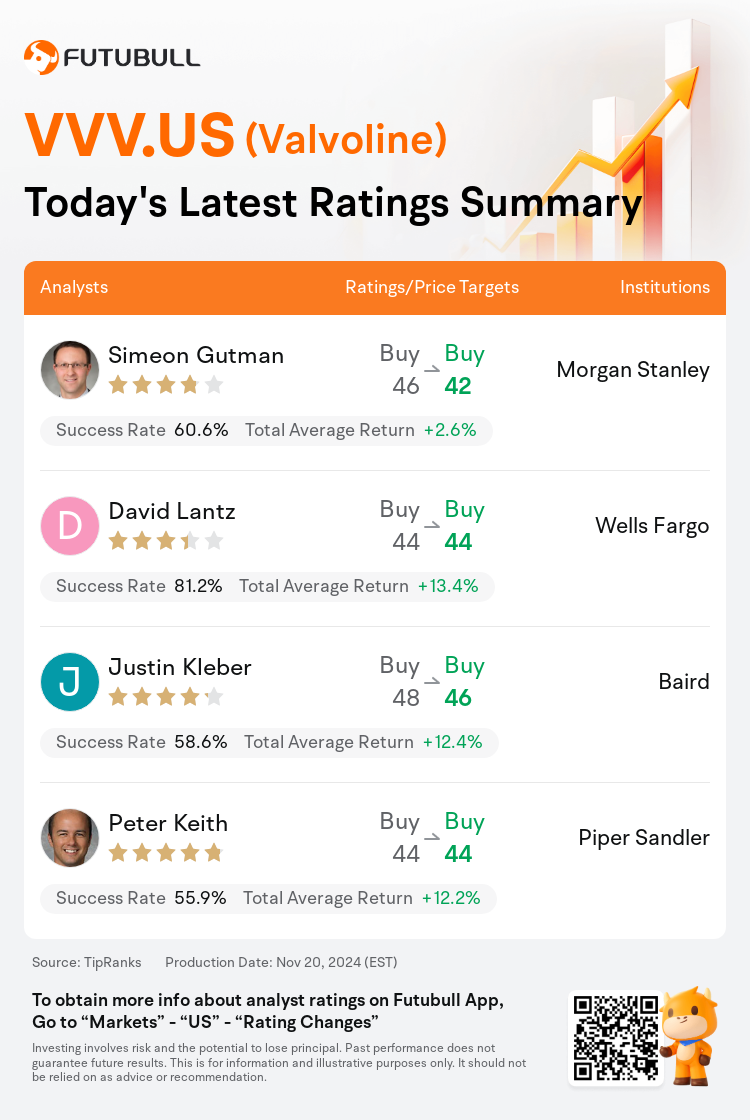

Morgan Stanley analyst Simeon Gutman maintains with a buy rating, and adjusts the target price from $46 to $42.

Wells Fargo analyst David Lantz maintains with a buy rating, and maintains the target price at $44.

Baird analyst Justin Kleber maintains with a buy rating, and adjusts the target price from $48 to $46.

Baird analyst Justin Kleber maintains with a buy rating, and adjusts the target price from $48 to $46.

Piper Sandler analyst Peter Keith maintains with a buy rating, and maintains the target price at $44.

Furthermore, according to the comprehensive report, the opinions of $Valvoline (VVV.US)$'s main analysts recently are as follows:

The firm maintains a positive outlook on Valvoline due to its steady and scarce growth combined with valuation upside. Despite this, the anticipated magnitude of EPS growth experienced a decline following the FY25 sales and adjusted EBITDA guidance, which were approximately 7% below the Street's expectations at the midpoint.

The underlying business of Valvoline is considered healthy despite directionally slowing comps and potential risks to the long-term algorithm, likely causing the shares to remain rangebound in the near term. While the shares are viewed as undervalued, there are not many anticipated near-term catalysts to propel their value, according to insights shared with investors.

Valvoline's solid finish to FY24 was somewhat overshadowed by a softer profit outlook, driven by cost uncertainties and an increase in IT expenditure. Furthermore, there was a notable rise in promotional activities from tire and repair shops.

While Q4 largely met expectations, the underperformance of the stock is understandable as projections for FY25 appear less optimistic, and the long-term outlook requires careful monitoring. Despite near-term uncertainties, a constructive view is maintained for the long-term.

Here are the latest investment ratings and price targets for $Valvoline (VVV.US)$ from 4 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

美東時間11月20日,多家華爾街大行更新了$勝牌 (VVV.US)$的評級,目標價介於42美元至46美元。

摩根士丹利分析師Simeon Gutman維持買入評級,並將目標價從46美元下調至42美元。

富國集團分析師David Lantz維持買入評級,維持目標價44美元。

貝雅分析師Justin Kleber維持買入評級,並將目標價從48美元下調至46美元。

貝雅分析師Justin Kleber維持買入評級,並將目標價從48美元下調至46美元。

派傑投資分析師Peter Keith維持買入評級,維持目標價44美元。

此外,綜合報道,$勝牌 (VVV.US)$近期主要分析師觀點如下:

由於勝牌持續穩定和稀缺的增長以及估值上漲,該公司對勝牌持樂觀態度。儘管如此,在FY25銷售和調整後的EBITDA指導方面經歷了EPS增長預期的下降,這大約比市場預期低7%。

儘管勝牌的基礎業務在方向上有所放緩,可能對長期算法構成潛在風險,但被認爲健康,可能導致股價在短期內保持區間波動。雖然股票被視爲被低估,但根據與投資者分享的見解,預計近期內沒有太多預期的催化劑來推動其價值。

勝牌在FY24年的良好結算在一定程度上被較柔和的利潤展望所掩蓋,這是由成本不確定性和IT支出增加驅動的。此外,輪胎和維修店的促銷活動明顯增加。

雖然Q4基本符合預期,但股票的表現不佳可以理解,因爲FY25的預測顯得不太樂觀,而長期展望需要仔細監控。儘管近期存在不確定性,但對長期保持建設性觀點。

以下爲今日4位分析師對$勝牌 (VVV.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。