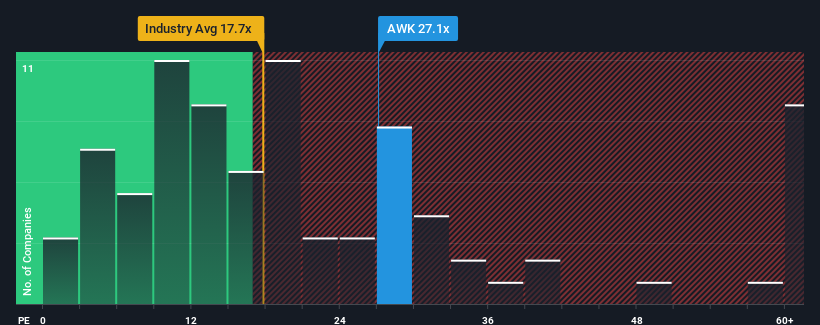

With a price-to-earnings (or "P/E") ratio of 27.1x American Water Works Company, Inc. (NYSE:AWK) may be sending bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 18x and even P/E's lower than 11x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Recent times have been advantageous for American Water Works Company as its earnings have been rising faster than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

NYSE:AWK Price to Earnings Ratio vs Industry November 19th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on American Water Works Company.

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, American Water Works Company would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 3.7% last year. The latest three year period has also seen a 20% overall rise in EPS, aided somewhat by its short-term performance. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 8.1% per annum during the coming three years according to the eleven analysts following the company. That's shaping up to be materially lower than the 11% each year growth forecast for the broader market.

In light of this, it's alarming that American Water Works Company's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that American Water Works Company currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for American Water Works Company (1 shouldn't be ignored) you should be aware of.

If you're unsure about the strength of American Water Works Company's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 3.7% last year. The latest three year period has also seen a 20% overall rise in EPS, aided somewhat by its short-term performance. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 3.7% last year. The latest three year period has also seen a 20% overall rise in EPS, aided somewhat by its short-term performance. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

回顧過去,我們看到公司去年的每股收益增長了3.7%。最近三年期間,每股收益整體上升了20%,這在一定程度上得益於其短期表現。因此,我們可以首先確認公司在這段時間內的盈利增長做得不錯。

回顧過去,我們看到公司去年的每股收益增長了3.7%。最近三年期間,每股收益整體上升了20%,這在一定程度上得益於其短期表現。因此,我們可以首先確認公司在這段時間內的盈利增長做得不錯。