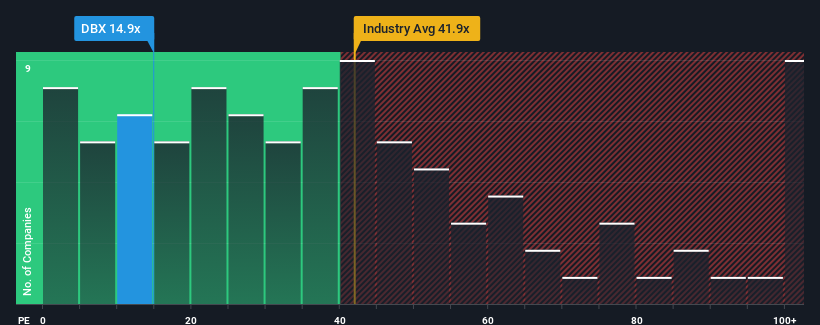

With a price-to-earnings (or "P/E") ratio of 14.9x Dropbox, Inc. (NASDAQ:DBX) may be sending bullish signals at the moment, given that almost half of all companies in the United States have P/E ratios greater than 20x and even P/E's higher than 35x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With earnings growth that's superior to most other companies of late, Dropbox has been doing relatively well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

NasdaqGS:DBX Price to Earnings Ratio vs Industry November 15th 2024 Keen to find out how analysts think Dropbox's future stacks up against the industry? In that case, our free report is a great place to start.

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Dropbox's to be considered reasonable.

If we review the last year of earnings growth, the company posted a worthy increase of 9.6%. Although, the latest three year period in total hasn't been as good as it didn't manage to provide any growth at all. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Shifting to the future, estimates from the ten analysts covering the company suggest earnings growth is heading into negative territory, declining 3.3% per annum over the next three years. Meanwhile, the broader market is forecast to expand by 11% per year, which paints a poor picture.

With this information, we are not surprised that Dropbox is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Dropbox's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for Dropbox (2 make us uncomfortable) you should be aware of.

If you're unsure about the strength of Dropbox's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of earnings growth, the company posted a worthy increase of 9.6%. Although, the latest three year period in total hasn't been as good as it didn't manage to provide any growth at all. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

If we review the last year of earnings growth, the company posted a worthy increase of 9.6%. Although, the latest three year period in total hasn't been as good as it didn't manage to provide any growth at all. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

如果我們回顧一下過去一年的盈利增長,公司的增長率爲9.6%。然而,最近三年的整體表現並不好,因爲沒有任何增長。因此可以公平地說,公司的盈利增長最近一直不穩定。

如果我們回顧一下過去一年的盈利增長,公司的增長率爲9.6%。然而,最近三年的整體表現並不好,因爲沒有任何增長。因此可以公平地說,公司的盈利增長最近一直不穩定。