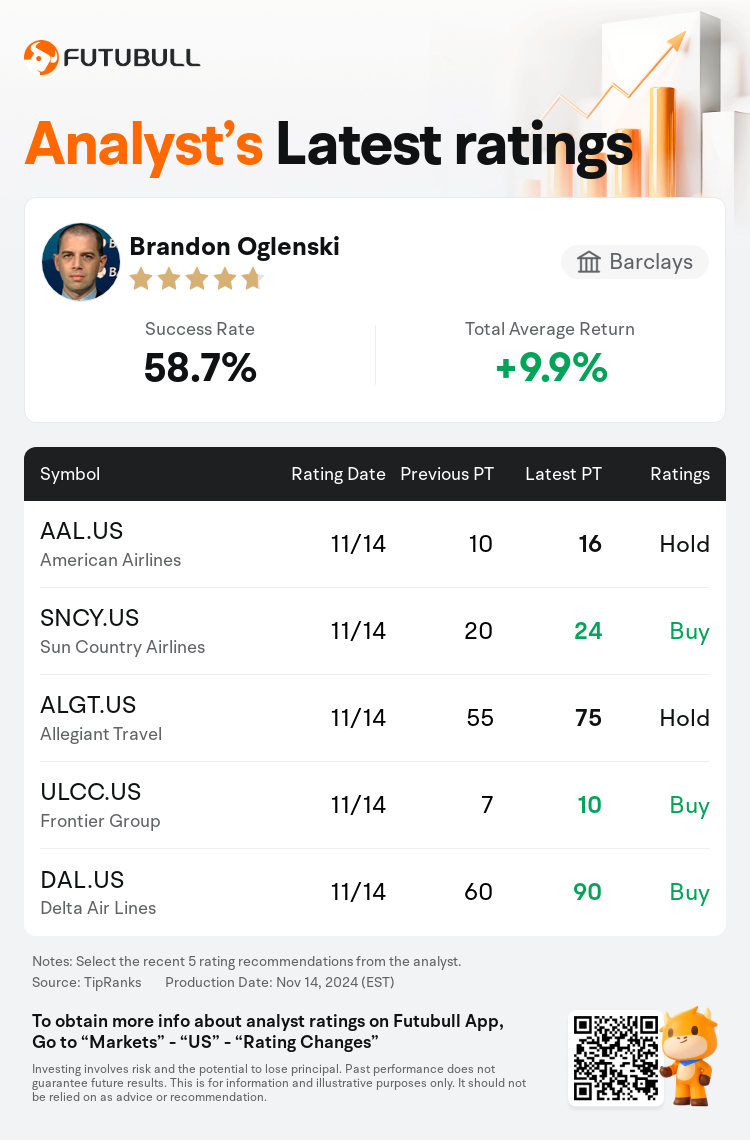

Barclays analyst Brandon Oglenski maintains $Delta Air Lines (DAL.US)$ with a buy rating, and adjusts the target price from $60 to $90.

According to TipRanks data, the analyst has a success rate of 58.7% and a total average return of 9.9% over the past year.

Furthermore, according to the comprehensive report, the opinions of $Delta Air Lines (DAL.US)$'s main analysts recently are as follows:

Furthermore, according to the comprehensive report, the opinions of $Delta Air Lines (DAL.US)$'s main analysts recently are as follows:

The outlook for airline fundamentals is expected to improve markedly by 2025, which could lead to a substantial reevaluation by the market and potentially allow for considerable appreciation in share prices for leading companies in the sector such as Delta, United, and Alaska. This improvement, along with a shift in investor sentiment, might contribute to a robust surge in airline stocks as we look to the next year. It's anticipated that the companies currently leading will continue to do so. There is a significant opportunity for upside as airline capacity growth is anticipated to decelerate in 2025, the competitive landscape among low-cost carriers undergoes changes, and the advantageous positions of industry leaders become more entrenched.

Airline stocks have shown strong performance since the recent election, with a significant uptick in a relevant airlines index. This positive trend is understandable given that airline equities typically have high volatility in response to market changes. The current industry fundamentals are promising, with a noted slowdown in domestic capacity growth, and the election outcomes are deemed to be generally favorable for industry fundamentals and earnings.

The firm expects Delta Air Lines to provide guidance for FY25 metrics and new long-term targets focused on loyalty/co-brand card and non-ticket revenue opportunities during its upcoming investor day. Anticipated topics of discussion may include the company's hub/partner strategy, methods of engaging with customers throughout their lifecycle, margin improvements from fleet renewal, the role of TechOps, potential cost efficiency levers, and capital allocation strategies.

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

巴克萊銀行分析師Brandon Oglenski維持$達美航空 (DAL.US)$買入評級,並將目標價從60美元上調至90美元。

根據TipRanks數據顯示,該分析師近一年總勝率為58.7%,總平均回報率為9.9%。

此外,綜合報道,$達美航空 (DAL.US)$近期主要分析師觀點如下:

此外,綜合報道,$達美航空 (DAL.US)$近期主要分析師觀點如下:

到2025年,航空公司基本面前景預計會顯著改善,這可能會導致市場對領先公司的股價進行重大重新評估,並可能爲達美、聯合和阿拉斯加等行業領軍公司的股價帶來相當大的升值。隨着投資者情緒的轉變,這種改善可能會促使航空股票在下一年迎來強勁上漲。預計目前領先的公司將繼續保持領先地位。隨着2025年航空公司容量增長預計放緩,廉價航空公司之間的競爭格局發生變化,以及行業領導者的有利地位更加鞏固,存在重大上行機會。

自最近的選舉以來,航空股表現強勁,相關航空指數有顯著上升。考慮到航空股通常對市場變化具有高波動性,這種積極趨勢是可以理解的。目前行業基本面向好,國內容量增長放緩,選舉結果被認爲一般對行業基本面和盈利有利。

公司預計達美航空將在即將舉行的投資者日上就FY25指標和新的着重於忠實/合作品牌卡和非票務收入機會的長期目標提供指引。討論的話題可能包括公司的樞紐/合作伙伴策略,與客戶在整個生命週期中互動的方法,來自機隊更新的利潤改善,技術運營的作用,潛在的成本效率槓桿以及資本配置策略。

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。