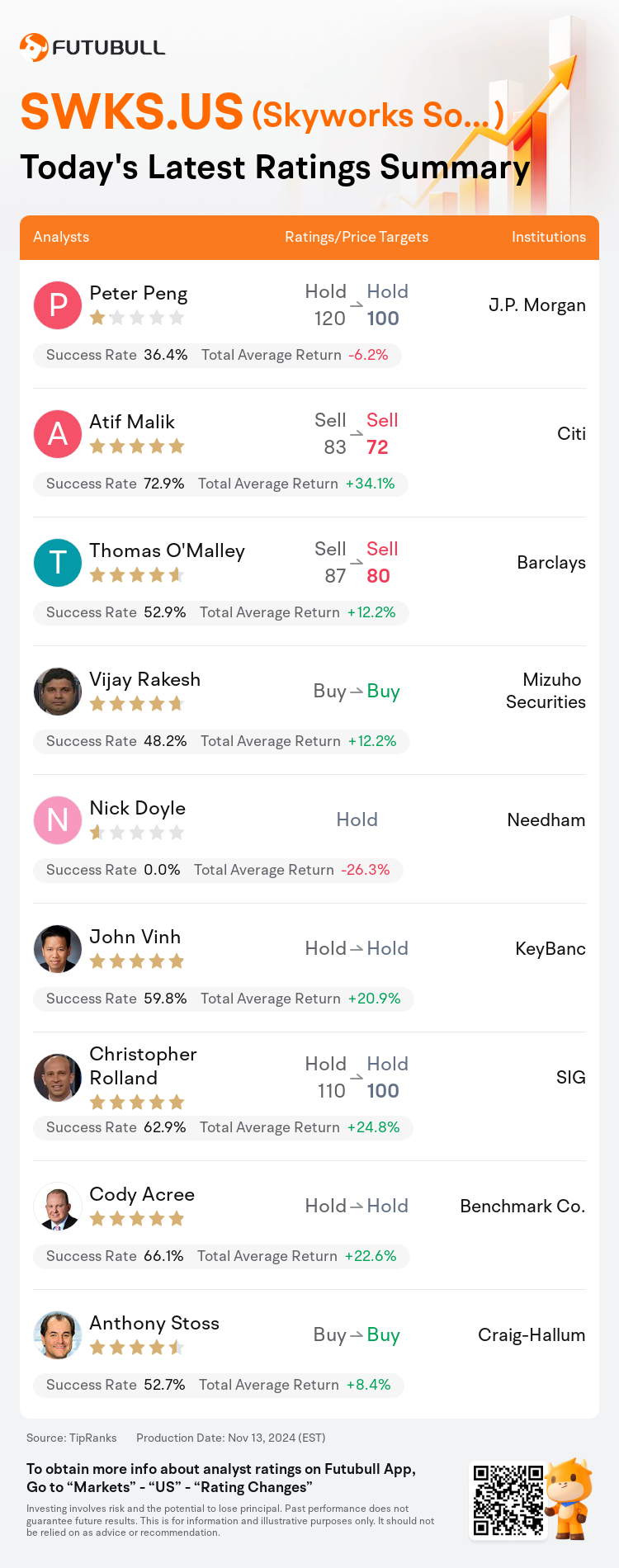

On Nov 13, major Wall Street analysts update their ratings for $Skyworks Solutions (SWKS.US)$, with price targets ranging from $72 to $100.

J.P. Morgan analyst Peter Peng maintains with a hold rating, and adjusts the target price from $120 to $100.

Citi analyst Atif Malik maintains with a sell rating, and adjusts the target price from $83 to $72.

Barclays analyst Thomas O'Malley maintains with a sell rating, and adjusts the target price from $87 to $80.

Barclays analyst Thomas O'Malley maintains with a sell rating, and adjusts the target price from $87 to $80.

Mizuho Securities analyst Vijay Rakesh maintains with a buy rating.

Needham analyst Nick Doyle initiates coverage with a hold rating.

Furthermore, according to the comprehensive report, the opinions of $Skyworks Solutions (SWKS.US)$'s main analysts recently are as follows:

The expectation is set for subdued growth in Broad Markets by 2025, due to persistently high inventory levels in the automotive, industrial, and wireless infrastructure sectors. Additionally, increased operating expenses are anticipated to exert pressure on earnings for that year. Despite recent underwhelming content performance related to Apple, there is a sentiment of hopeful anticipation for a recovery in the following year. The potential for value recovery hinges on the ability to regain Apple content, although its feasibility is yet to be confirmed.

Skyworks' September quarter results were marginally above projections, but its revenue guidance for the December quarter showed a 4% sequential increase, which was somewhat under the anticipated consensus. Despite this, the performance was more robust than expected, largely due to sustained vigor from its primary customer, Apple.

The company's forecast for the December quarter was set below expectations, predominantly due to a recovery in the broad market that was slower than anticipated. This led to a revision of the earnings estimates for 2024 and 2025, reflecting weaker broad market conditions, reduced gross margins, and increased operating expenses.

Skyworks is going through an elongated transitional phase in its core Mobile business and Broad Markets, which may result in a delay in topline growth until FY26. The company's earnings projections have been significantly adjusted, with a notable downward revision of the pro-forma EPS for FY25 and FY26.

Here are the latest investment ratings and price targets for $Skyworks Solutions (SWKS.US)$ from 9 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

美東時間11月13日,多家華爾街大行更新了$思佳訊 (SWKS.US)$的評級,目標價介於72美元至100美元。

摩根大通分析師Peter Peng維持持有評級,並將目標價從120美元下調至100美元。

花旗分析師Atif Malik維持賣出評級,並將目標價從83美元下調至72美元。

巴克萊銀行分析師Thomas O'Malley維持賣出評級,並將目標價從87美元下調至80美元。

巴克萊銀行分析師Thomas O'Malley維持賣出評級,並將目標價從87美元下調至80美元。

瑞穗證券分析師Vijay Rakesh維持買入評級。

Needham分析師Nick Doyle首次給予持有評級。

此外,綜合報道,$思佳訊 (SWKS.US)$近期主要分析師觀點如下:

由於汽車、工業和無線基礎設施行業的庫存水平持續偏高,預計到2025年廣泛市場將保持溫和增長。此外,預計營業費用的增加將對當年的收益施加壓力。儘管與蘋果相關的內容表現近期不盡如人意,但人們對明年復甦的情緒仍充滿希望。價值恢復的潛力取決於重新獲得蘋果內容的能力,儘管其可行性尚待確認。

Skyworks九月季度的業績略高於預期,但其對十二月季度的營業收入指引顯示出4%的環比增長,稍低於預期共識。儘管如此,這一表現仍比預期強勁,主要得益於其主要客戶蘋果的持續活力。

該公司對十二月季度的預測低於預期,主要是因爲廣泛市場的復甦速度低於預期。這導致了對2024年和2025年的每股收益預測進行修訂,反映出較弱的廣泛市場條件、降低的毛利率和增加的營業費用。

Skyworks在其核心移動業務和廣泛市場經歷了較長的過渡階段,這可能導致上行增長推遲到2026財年。公司的收益預測已進行了重大調整,2025財年和2026財年的每股收益預期顯著下調。

以下爲今日9位分析師對$思佳訊 (SWKS.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。