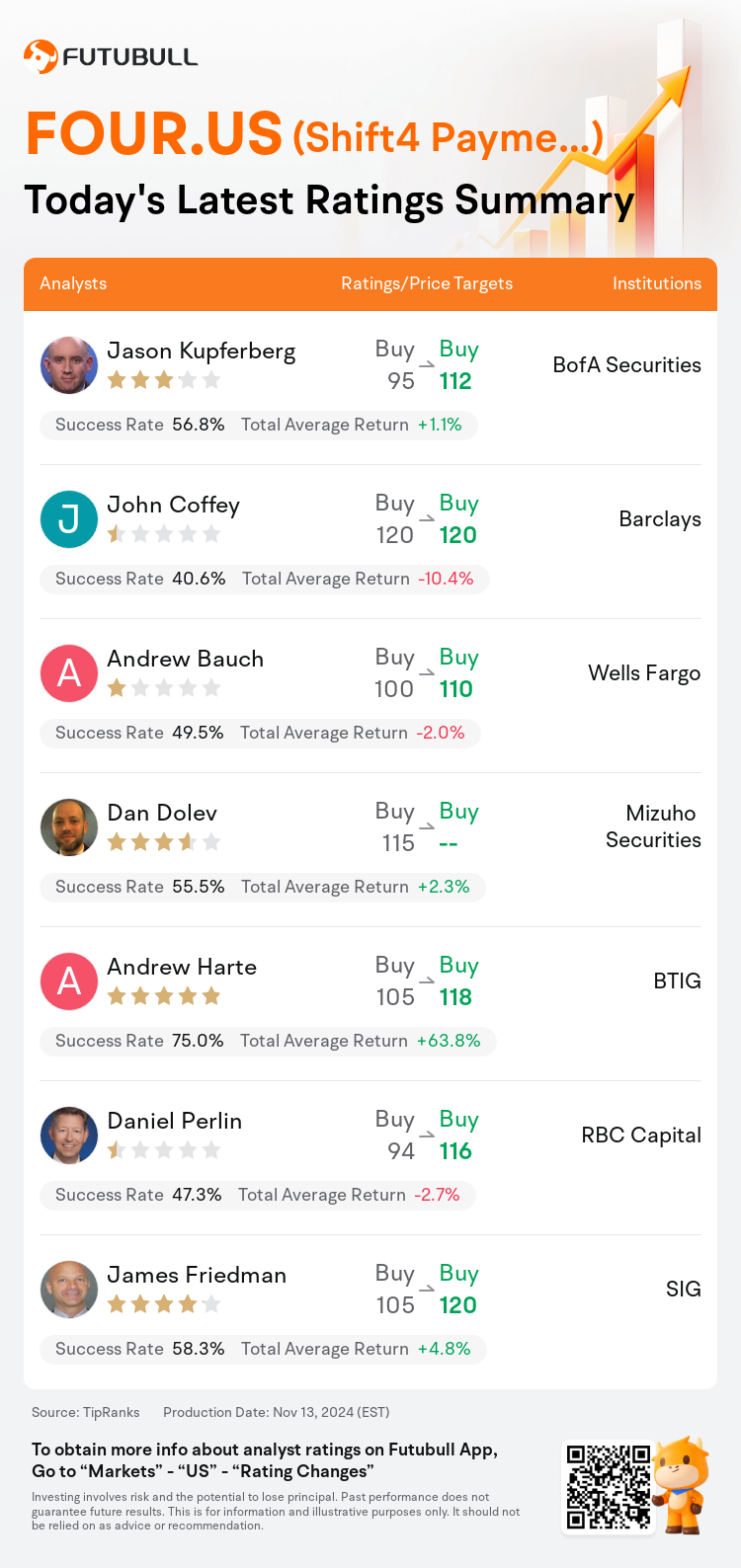

On Nov 13, major Wall Street analysts update their ratings for $Shift4 Payments (FOUR.US)$, with price targets ranging from $110 to $120.

BofA Securities analyst Jason Kupferberg maintains with a buy rating, and adjusts the target price from $95 to $112.

Barclays analyst John Coffey maintains with a buy rating, and maintains the target price at $120.

Wells Fargo analyst Andrew Bauch maintains with a buy rating, and adjusts the target price from $100 to $110.

Wells Fargo analyst Andrew Bauch maintains with a buy rating, and adjusts the target price from $100 to $110.

Mizuho Securities analyst Dan Dolev maintains with a buy rating.

BTIG analyst Andrew Harte maintains with a buy rating, and adjusts the target price from $105 to $118.

Furthermore, according to the comprehensive report, the opinions of $Shift4 Payments (FOUR.US)$'s main analysts recently are as follows:

Shift4 Payments' volumes came in below expectations and the forward guidance was adjusted downwards, influenced by a decrease in consumer spending within the restaurant and hospitality sectors, adverse weather conditions, and a slower pace of growth internationally than anticipated. Despite the shares experiencing only a modest decline after a significant run, this could be attributed to a marginal increase in the lower end of the fourth quarter revenue and adjusted EBITDA guidance, a volume backlog that rose by 32% from the previous quarter, and an annualized fourth quarter adjusted EBITDA that aligns with the 2025 consensus. Additionally, there's a current market tilt towards small and mid-cap names.

Shift4 Payments' Q3 outcomes fell short in terms of net revenues, gross profit, and end-to-end volumes, attributed to diminished consumer expenditure. Despite the less-than-ideal quarter, it is believed that through strategic ventures and beneficial acquisitions, the company is positioned to sustain over 20% organic revenue growth for several years.

Shift4 Payments' Q3 volume and net revenue fell below Street expectations. Analysts point out that although no explicit fiscal 2025 guidance was provided, there were indications of management's confidence in the company's prospects. It is believed that investors will retain a positive perspective on Shift4's growth potential despite the modest Q3 performance. The company continues to be viewed favorably in terms of its growth outlook.

Here are the latest investment ratings and price targets for $Shift4 Payments (FOUR.US)$ from 7 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

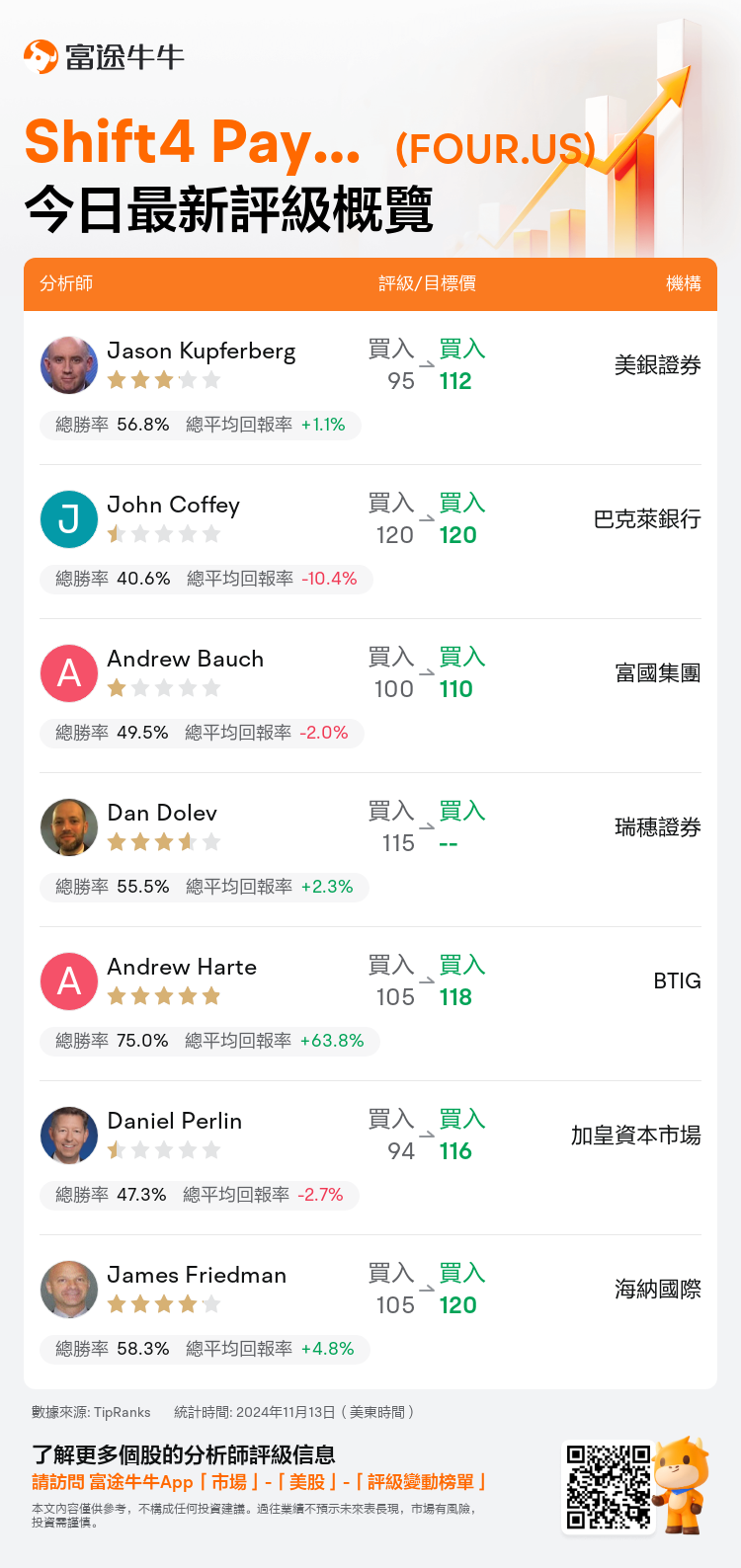

美東時間11月13日,多家華爾街大行更新了$Shift4 Payments (FOUR.US)$的評級,目標價介於110美元至120美元。

美銀證券分析師Jason Kupferberg維持買入評級,並將目標價從95美元上調至112美元。

巴克萊銀行分析師John Coffey維持買入評級,維持目標價120美元。

富國集團分析師Andrew Bauch維持買入評級,並將目標價從100美元上調至110美元。

富國集團分析師Andrew Bauch維持買入評級,並將目標價從100美元上調至110美元。

瑞穗證券分析師Dan Dolev維持買入評級。

BTIG分析師Andrew Harte維持買入評級,並將目標價從105美元上調至118美元。

此外,綜合報道,$Shift4 Payments (FOUR.US)$近期主要分析師觀點如下:

shift4 payments 的成交量低於預期,前瞻性指引也向下調整,受餐飲和酒店行業消費減少、不利天氣條件及國際增長速度低於預期的影響。儘管在經過一輪顯著的上漲後,股價僅小幅下跌,這可以歸因於第四季度營業收入和調整後的 EBITDA 指引的低端小幅增長,以及與前一季度相比,上升了 32% 的成交量積壓,還有與 2025 年共識一致的年化第四季度調整後 EBITDA。此外,目前市場偏向小型和中型公司的趨勢。

shift4 payments 的第三季度結果在淨營業收入、毛利潤和端到端成交量方面未達到預期,歸因於消費支出減少。儘管這一季度並不理想,但相信通過戰略投資和有利的收購,公司有望在未來幾年內實現超過 20% 的有機營業收入增長。

shift4 payments 的第三季度成交量和淨營業收入未達到市場預期。分析師指出,儘管沒有提供明確的 2025 財年指引,但管理層對公司前景的信懇智能仍有跡象。儘管第三季度業績平平,但投資者仍可能對 shift4 的增長潛力保持積極看法。公司在其增長前景方面繼續受到好評。

以下爲今日7位分析師對$Shift4 Payments (FOUR.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。