Mammoth Energy Services, Inc. (NASDAQ:TUSK) shares have had a horrible month, losing 26% after a relatively good period beforehand. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 21% in that time.

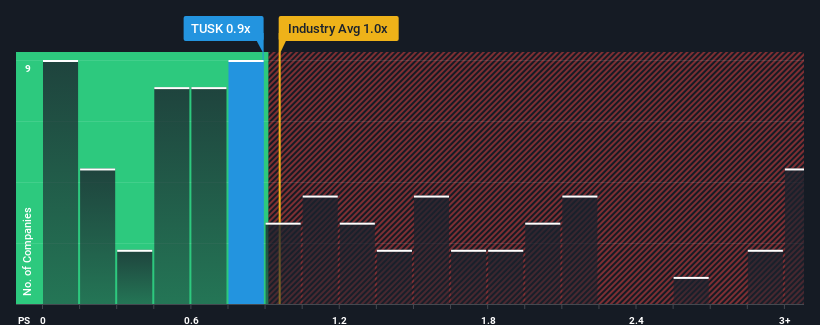

In spite of the heavy fall in price, there still wouldn't be many who think Mammoth Energy Services' price-to-sales (or "P/S") ratio of 0.9x is worth a mention when the median P/S in the United States' Energy Services industry is similar at about 1x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

NasdaqGS:TUSK Price to Sales Ratio vs Industry November 13th 2024

How Mammoth Energy Services Has Been Performing

For example, consider that Mammoth Energy Services' financial performance has been poor lately as its revenue has been in decline. It might be that many expect the company to put the disappointing revenue performance behind them over the coming period, which has kept the P/S from falling. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Mammoth Energy Services' earnings, revenue and cash flow.

Is There Some Revenue Growth Forecasted For Mammoth Energy Services?

In order to justify its P/S ratio, Mammoth Energy Services would need to produce growth that's similar to the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 48%. As a result, revenue from three years ago have also fallen 27% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 6.3% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

In light of this, it's somewhat alarming that Mammoth Energy Services' P/S sits in line with the majority of other companies. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

What We Can Learn From Mammoth Energy Services' P/S?

With its share price dropping off a cliff, the P/S for Mammoth Energy Services looks to be in line with the rest of the Energy Services industry. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We find it unexpected that Mammoth Energy Services trades at a P/S ratio that is comparable to the rest of the industry, despite experiencing declining revenues during the medium-term, while the industry as a whole is expected to grow. When we see revenue heading backwards in the context of growing industry forecasts, it'd make sense to expect a possible share price decline on the horizon, sending the moderate P/S lower. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

The company's balance sheet is another key area for risk analysis. You can assess many of the main risks through our free balance sheet analysis for Mammoth Energy Services with six simple checks.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mammoth Energy Services公司(納斯達克股票代碼:TUSK)股票在過去一個月中表現糟糕,此前的表現相對較好,跌幅達到26%。過去30天的跌幅爲股東們度過了艱難的一年,股價在此期間下跌了21%。

儘管股價大幅下跌,但仍然沒有太多人認爲Mammoth Energy Services的市銷率(或「P/S」)0.9倍值得一提,因爲美國能源服務行業的中位數市銷率約爲1倍。雖然這可能不會引起任何人的注意,但如果市銷率沒有合理性,投資者可能會錯過一個潛在機會,或者忽視即將到來的失望。

納斯達克股票代碼TUSK市銷率與行業比較 2024年11月13日

Mammoth Energy Services的表現如何

例如,考慮到Mammoth Energy Services最近的財務表現較差,營業收入一直在下滑。許多人可能期望該公司能在未來一段時間內擺脫營收表現低迷的局面,這也是導致市銷率沒有下跌的原因。如果你喜歡這家公司,至少希望情況是這樣,這樣你就有可能在股票尚未受到青睞時購買一些股票。

我們沒有分析師預測,但您可以查看我們免費報告,了解最近的趨勢如何爲Mammoth Energy Services未來鋪平道路,包括營業收入和現金流。

隨着其股價的暴跌,Mammoth Energy Services的市銷率似乎與其他能源服務行業板塊保持一致。雖然市銷率不應該是確定是否買入股票的關鍵因素,但它是營業收入預期的相當可靠的晴雨表。

我們發現讓人意想不到的是,儘管在中期經歷營業收入下降,與整個行業預期增長相比,Mammoth Energy Services交易的市銷率仍與行業其他公司可比。當我們看到營業收入在增長行業預測的背景下回落時,預計未來可能會有股價下跌的跡象,將市銷率降至適中水平。除非最近的中期條件有了明顯改善,投資者將很難接受當前的股價作爲公允價值。

公司的資產負債表是風險分析的另一個關鍵領域。您可以通過我們爲Mammoth Energy Services提供的免費資產負債表分析來評估許多主要風險,包括六項簡單檢查。

In order to justify its P/S ratio, Mammoth Energy Services would need to produce growth that's similar to the industry.

In order to justify its P/S ratio, Mammoth Energy Services would need to produce growth that's similar to the industry.

爲了證明其市銷率,猛獁能源服務公司需要產生與行業相似的增長。

爲了證明其市銷率,猛獁能源服務公司需要產生與行業相似的增長。