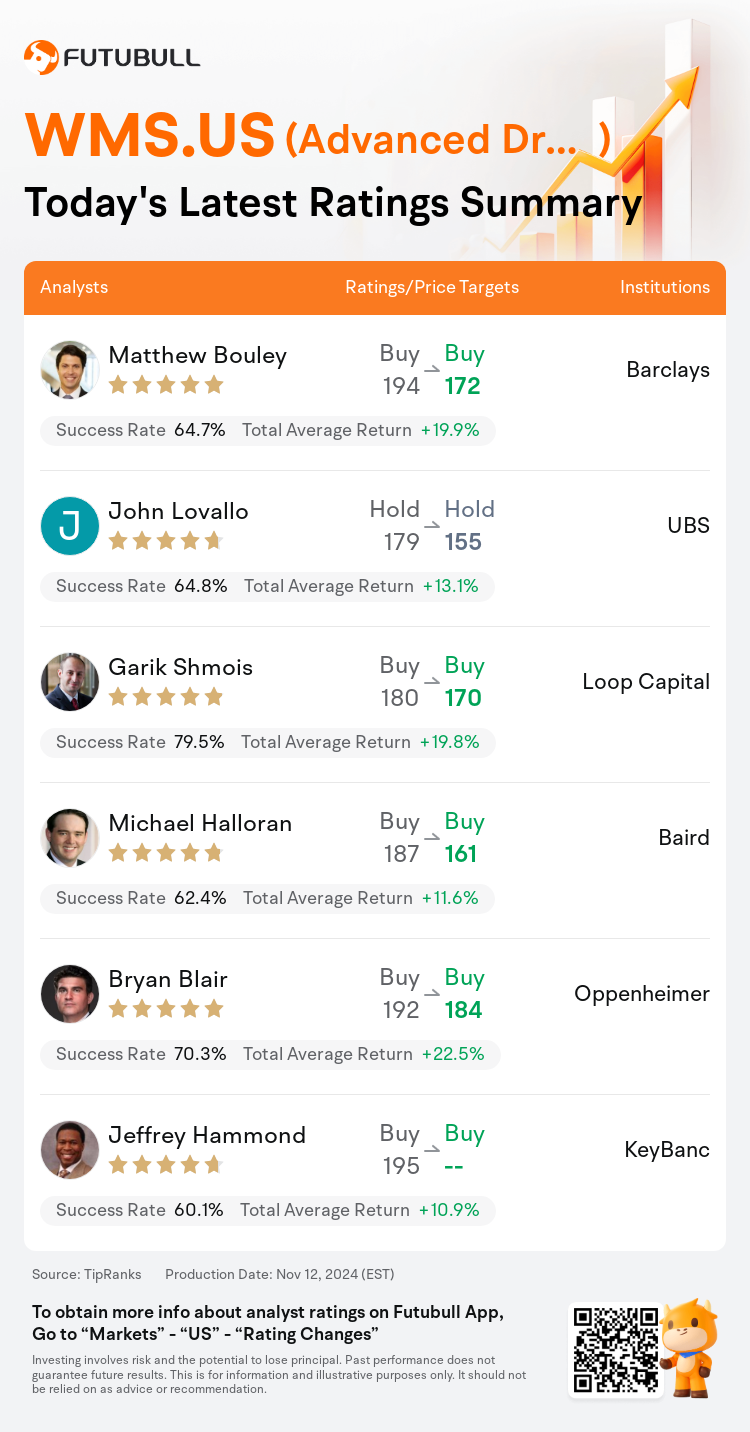

On Nov 12, major Wall Street analysts update their ratings for $Advanced Drainage (WMS.US)$, with price targets ranging from $155 to $184.

Barclays analyst Matthew Bouley maintains with a buy rating, and adjusts the target price from $194 to $172.

UBS analyst John Lovallo maintains with a hold rating, and adjusts the target price from $179 to $155.

Loop Capital analyst Garik Shmois maintains with a buy rating, and adjusts the target price from $180 to $170.

Loop Capital analyst Garik Shmois maintains with a buy rating, and adjusts the target price from $180 to $170.

Baird analyst Michael Halloran maintains with a buy rating, and adjusts the target price from $187 to $161.

Oppenheimer analyst Bryan Blair maintains with a buy rating, and adjusts the target price from $192 to $184.

Furthermore, according to the comprehensive report, the opinions of $Advanced Drainage (WMS.US)$'s main analysts recently are as follows:

The company's outlook has been adjusted due to a combination of factors including the non-residential sector, weather-related challenges, and rising input costs.

The company's Q2 earnings fell short of expectations, and subsequent guidance revision came unexpectedly as the quarter appeared to be aligning well despite the erratic non-residential environment. Sales did not meet forecasts due to storm-related impacts and adverse price-to-cost conditions. Nonetheless, the period's highlights were bolstered by robust infrastructure and residential sales.

The firm observed that shares declined by 14.3% following the company's Q2 performance, which fell short of expectations, and its subsequent reduction in FY25 guidance. This adjustment was made to account for ongoing volatility in non-residential demand, delays in projects due to hurricanes, and persisting challenges with pricing and costs. In light of the results from the first half of the year and prevailing business trends, the company has revised its FY25 sales forecast. Despite the disappointing results and lowered guidance, the opinion is that the risks for the second half of the year have been significantly mitigated. The firm suggests that the market's reaction may have been excessive and sees this as an opportune moment for investors to consider engaging with this unique water management asset.

The reduction in margins was anticipated due to well-known inconsistencies within the Non-Residential sector. The impression is that the investor concerns largely centered around the extent of margin pressures resulting from pricing strategies. However, this seems primarily linked to elevated input costs rather than a weakening of top-line pricing. Despite a more cautious outlook on end-market and margin trends, the view is that the current decline in share price presents an opportunity to invest in a robust narrative that is bolstered by material conversion drivers and numerous opportunities for sustained margin improvement.

Apart from reducing estimates and adjusting for lower non-residential expectations, the primary concern is centered on the challenge of increasing prices to counterbalance rising material costs, which is essentially a cyclical debate. However, pricing remains stable on a sequential basis, and it is anticipated to recover alongside demand. Moreover, the absolute margin levels remain noteworthy.

Here are the latest investment ratings and price targets for $Advanced Drainage (WMS.US)$ from 6 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

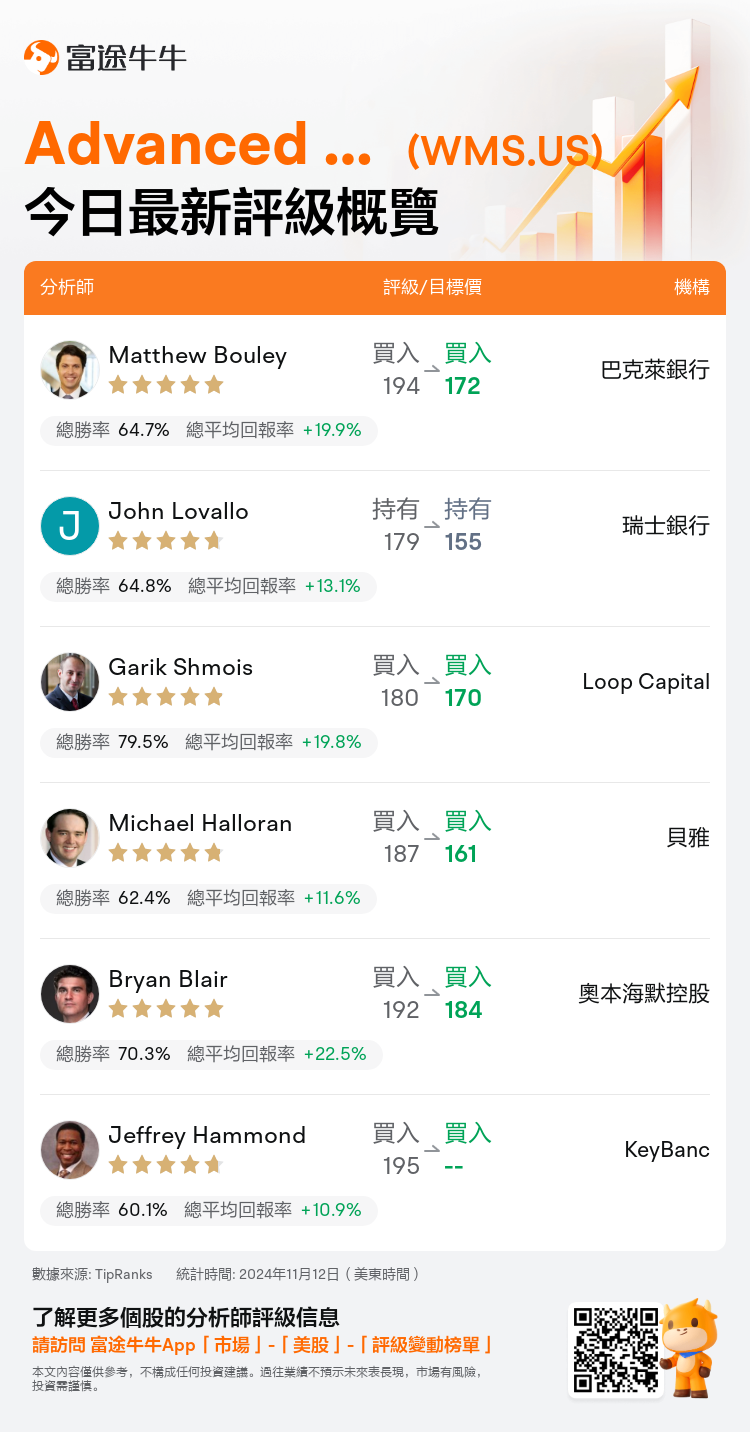

美東時間11月12日,多家華爾街大行更新了$Advanced Drainage (WMS.US)$的評級,目標價介於155美元至184美元。

巴克萊銀行分析師Matthew Bouley維持買入評級,並將目標價從194美元下調至172美元。

瑞士銀行分析師John Lovallo維持持有評級,並將目標價從179美元下調至155美元。

Loop Capital分析師Garik Shmois維持買入評級,並將目標價從180美元下調至170美元。

Loop Capital分析師Garik Shmois維持買入評級,並將目標價從180美元下調至170美元。

貝雅分析師Michael Halloran維持買入評級,並將目標價從187美元下調至161美元。

奧本海默控股分析師Bryan Blair維持買入評級,並將目標價從192美元下調至184美元。

此外,綜合報道,$Advanced Drainage (WMS.US)$近期主要分析師觀點如下:

由於包括非住宅部門、與天氣有關的挑戰以及不斷上漲的原材料成本等因素的綜合影響,公司的展望已經調整。

公司的第二季度收益低於預期,並且隨後的引導修訂出乎意料,因爲儘管非住宅環境不穩定,該季度似乎進展順利。由於暴風雨相關影響和不利的價格成本條件,銷售未達到預期。儘管如此,該時期的亮點得到了強勁的基礎設施和住宅銷售的支撐。

公司觀察到,隨着公司第二季度業績低於預期、FY25指導後的股價下跌了14.3%。這一調整是爲了考慮到非住宅需求持續波動、由於颶風導致項目延遲以及定價與成本持續存在挑戰。鑑於上半年的結果和當前業務趨勢,公司已修訂了FY25年銷售預測。儘管結果令人失望並降低了指導,但看法是下半年的風險已得到顯著減輕。公司表示,市場反應可能過度,認爲現在是投資者考慮參與這項獨特的水利資產的絕佳時機。

由於非住宅業務內部的已知不一致性,利潤率的降低是可以預料的。投資者關注的主要集中在利潤率壓力程度上。然而,這似乎主要與高昂的原材料成本有關,而不是營收定價的下滑。儘管對終端市場和利潤率趨勢持更爲謹慎的觀點,但認爲目前股價下跌提供了一個投資機會,該觀點得到實質性的轉化驅動和許多持續提高利潤率的機會的支撐。

除了降低預測和調整非住宅預期外,主要關注點集中在應對上升的原材料成本,以提高價格以抵消上漲成本的挑戰,這實質上是一個週期性的討論。然而,定價在按順序的基礎上保持穩定,預計隨着需求的提高而恢復。此外,絕對利潤率水平仍然值得關注。

以下爲今日6位分析師對$Advanced Drainage (WMS.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。