Prestige Consumer Healthcare Inc. (NYSE:PBH) Released Earnings Last Week And Analysts Lifted Their Price Target To US$85.29

Prestige Consumer Healthcare Inc. (NYSE:PBH) Released Earnings Last Week And Analysts Lifted Their Price Target To US$85.29

Of course, another way to look at these forecasts is to place them into context against the industry itself. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 3.9% growth on an annualised basis. That is in line with its 4.3% annual growth over the past five years. Compare this with the broader industry (in aggregate), which analyst estimates suggest will see revenues grow 10% annually. So although Prestige Consumer Healthcare is expected to maintain its revenue growth rate, it's forecast to grow slower than the wider industry.

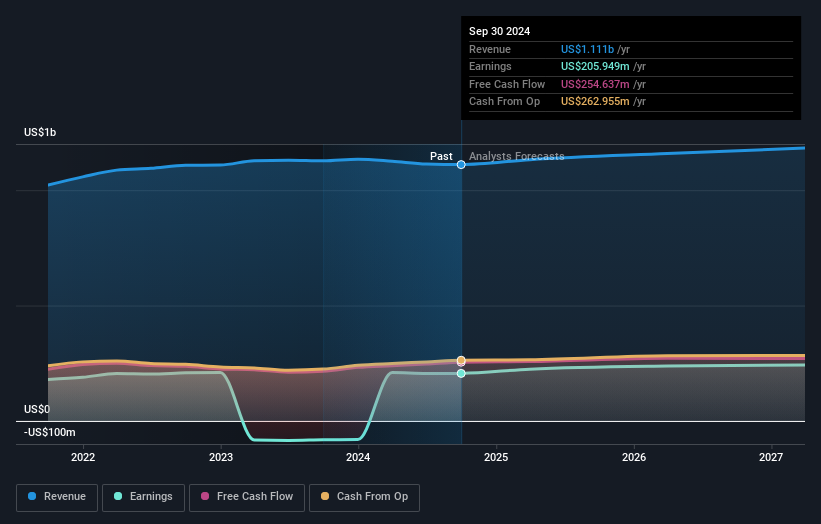

Of course, another way to look at these forecasts is to place them into context against the industry itself. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 3.9% growth on an annualised basis. That is in line with its 4.3% annual growth over the past five years. Compare this with the broader industry (in aggregate), which analyst estimates suggest will see revenues grow 10% annually. So although Prestige Consumer Healthcare is expected to maintain its revenue growth rate, it's forecast to grow slower than the wider industry. It's been a good week for Prestige Consumer Healthcare Inc. (NYSE:PBH) shareholders, because the company has just released its latest second-quarter results, and the shares gained 8.5% to US$80.37. Results were roughly in line with estimates, with revenues of US$284m and statutory earnings per share of US$1.09. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

普雷斯蒂奇消費保健公司股東度過了一個不錯的一週,因爲公司剛剛發佈了最新的第二季度業績,股價上漲了8.5%,達到80.37美元。結果與預期大致相符,營業收入爲28400萬美元,每股收益爲1.09美元。對投資者來說,這是一個重要時刻,他們可以通過報告追蹤公司的業績,了解專家們對明年的預測,並查看業務預期是否有任何變化。我們彙總了最新的預測數據,以查看分析師是否根據這些結果調整了其盈利模型。

Following last week's earnings report, Prestige Consumer Healthcare's eight analysts are forecasting 2025 revenues to be US$1.13b, approximately in line with the last 12 months. Per-share earnings are expected to increase 7.6% to US$4.49. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.13b and earnings per share (EPS) of US$4.48 in 2025. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

在上週的業績報告之後,普雷斯蒂奇消費保健的八位分析師預測2025年的營收將達到11.3億美元,與過去12個月大致相符。每股收益預計將增長7.6%,達到4.49美元。然而,在最新業績公佈之前,分析師們預計2025年的營收將達到113億美元,每股收益(EPS)爲4.48美元。因此,儘管分析師已更新其估算,但根據最新結果來看,業務預期並沒有發生重大變化。

The consensus price target rose 7.4% to US$85.29despite there being no meaningful change to earnings estimates. It could be that the analystsare reflecting the predictability of Prestige Consumer Healthcare's earnings by assigning a price premium. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Prestige Consumer Healthcare analyst has a price target of US$95.00 per share, while the most pessimistic values it at US$70.00. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

儘管盈利預期沒有發生實質性變化,共識價格目標上漲了7.4%,達到85.29美元。分析師可能反映了普雷斯蒂奇消費保健的盈利可靠性,因此給予了價格溢價。然而,固守單一價格目標可能是不明智的,因爲共識目標實際上是分析師價格目標的平均值。因此,一些投資者喜歡查看估算範圍,以查看對公司估值是否存在不同意見。最樂觀的普雷斯蒂奇消費保健分析師設定了每股95.00美元的價格目標,而最悲觀者將其價值定爲70.00美元。估算範圍較窄可能表明該業務的未來相對容易估值,或者分析師對其前景有着明確看法。

Of course, another way to look at these forecasts is to place them into context against the industry itself. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 3.9% growth on an annualised basis. That is in line with its 4.3% annual growth over the past five years. Compare this with the broader industry (in aggregate), which analyst estimates suggest will see revenues grow 10% annually. So although Prestige Consumer Healthcare is expected to maintain its revenue growth rate, it's forecast to grow slower than the wider industry.

當然,審視這些預測的另一種方法是將它們放在行業本身的背景下。根據分析師的說法,截至2025年底的時期帶來了更多相同的情況,預計營業收入將以年均3.9%的增長率進行顯示。這與過去五年裏其4.3%的年均增長率相一致。將這與更廣泛的行業(總體)進行比較,分析師的估計表明,營收將以年均10%的速度增長。因此,儘管預斯蒂奇預計將保持其營收增長速度,但預計增速將低於更廣泛的行業板塊。

The Bottom Line

最重要的事情是分析師增加了它對下一年每股虧損的估計。令人欣慰的是,營收預測未發生重大變化,業務仍有望比整個行業增長更快。共識價格目標穩定在28.50美元,最新估計不足以對價格目標產生影響。

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that Prestige Consumer Healthcare's revenue is expected to perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

最重要的是,可以得出的結論是,市場情緒沒有發生重大變化,分析師再次確認業務表現與之前的每股收益預估相符。幸運的是,分析師還重申了他們的營收預估,暗示它正按照預期跟蹤。儘管我們的數據表明,預斯蒂奇的營收預計將低於更廣泛的行業。我們注意到了價格目標的提升,暗示分析師認爲企業的內在價值可能會隨時間提升。

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Prestige Consumer Healthcare going out to 2027, and you can see them free on our platform here..

話雖如此,公司盈利的長期軌跡比明年更重要得多。在Simply Wall St上,我們提供了截至2027年的預斯蒂奇消費者保健的全套分析師預測,您可以在我們的平台上免費查看。

And what about risks? Every company has them, and we've spotted 1 warning sign for Prestige Consumer Healthcare you should know about.

那風險呢?每家公司都會有風險,我們發現了一條警示,您應該知道普雷斯蒂奇消費者保健。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。