CoreCard Corporation (NYSE:CCRD) shares have continued their recent momentum with a 30% gain in the last month alone. Unfortunately, despite the strong performance over the last month, the full year gain of 7.7% isn't as attractive.

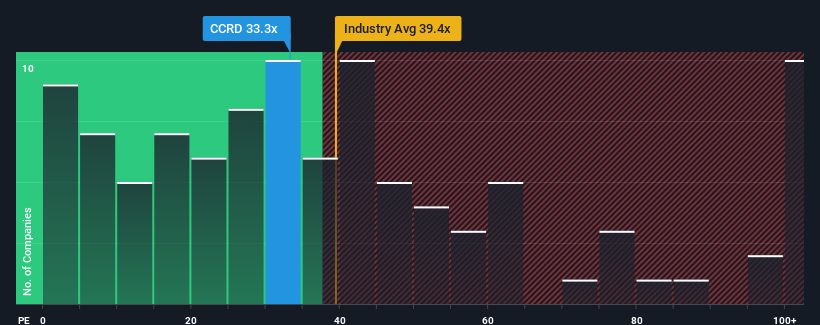

Following the firm bounce in price, given close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 19x, you may consider CoreCard as a stock to avoid entirely with its 33.3x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, CoreCard has been doing relatively well. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:CCRD Price to Earnings Ratio vs Industry November 9th 2024 Keen to find out how analysts think CoreCard's future stacks up against the industry? In that case, our free report is a great place to start.

Does Growth Match The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as CoreCard's is when the company's growth is on track to outshine the market decidedly.

If we review the last year of earnings growth, the company posted a worthy increase of 6.8%. Ultimately though, it couldn't turn around the poor performance of the prior period, with EPS shrinking 47% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Shifting to the future, estimates from the only analyst covering the company suggest earnings should grow by 66% over the next year. Meanwhile, the rest of the market is forecast to only expand by 15%, which is noticeably less attractive.

In light of this, it's understandable that CoreCard's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

The strong share price surge has got CoreCard's P/E rushing to great heights as well. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that CoreCard maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 1 warning sign for CoreCard you should be aware of.

If you're unsure about the strength of CoreCard's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The only time you'd be truly comfortable seeing a P/E as steep as CoreCard's is when the company's growth is on track to outshine the market decidedly.

The only time you'd be truly comfortable seeing a P/E as steep as CoreCard's is when the company's growth is on track to outshine the market decidedly.

只有當公司的增長明顯超過市場時,您才會真正舒適地看到像CoreCard這樣高的P/E。

只有當公司的增長明顯超過市場時,您才會真正舒適地看到像CoreCard這樣高的P/E。