MasterCraft Boat Holdings, Inc. (NASDAQ:MCFT) shares have had a really impressive month, gaining 27% after a shaky period beforehand. Looking further back, the 10% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

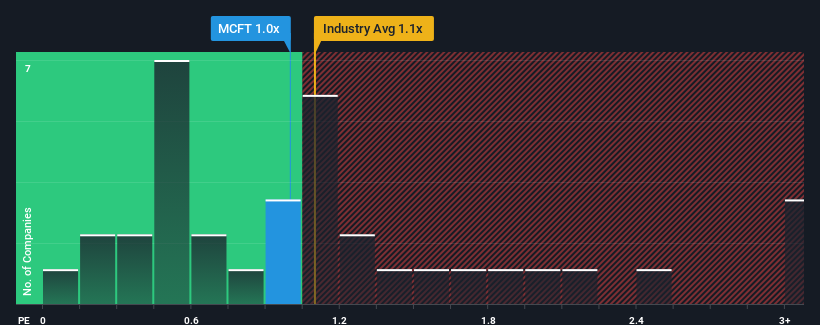

Even after such a large jump in price, you could still be forgiven for feeling indifferent about MasterCraft Boat Holdings' P/S ratio of 1x, since the median price-to-sales (or "P/S") ratio for the Leisure industry in the United States is also close to 1.1x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

NasdaqGM:MCFT Price to Sales Ratio vs Industry November 7th 2024

What Does MasterCraft Boat Holdings' Recent Performance Look Like?

Recent times haven't been great for MasterCraft Boat Holdings as its revenue has been falling quicker than most other companies. It might be that many expect the dismal revenue performance to revert back to industry averages soon, which has kept the P/S from falling. You'd much rather the company improve its revenue if you still believe in the business. If not, then existing shareholders may be a little nervous about the viability of the share price.

Keen to find out how analysts think MasterCraft Boat Holdings' future stacks up against the industry? In that case, our free report is a great place to start.

How Is MasterCraft Boat Holdings' Revenue Growth Trending?

In order to justify its P/S ratio, MasterCraft Boat Holdings would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a frustrating 45% decrease to the company's top line. As a result, revenue from three years ago have also fallen 21% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to slump, contracting by 22% during the coming year according to the seven analysts following the company. Meanwhile, the broader industry is forecast to expand by 0.6%, which paints a poor picture.

With this information, we find it concerning that MasterCraft Boat Holdings is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh on the share price eventually.

The Key Takeaway

MasterCraft Boat Holdings appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our check of MasterCraft Boat Holdings' analyst forecasts revealed that its outlook for shrinking revenue isn't bringing down its P/S as much as we would have predicted. When we see a gloomy outlook like this, our immediate thoughts are that the share price is at risk of declining, negatively impacting P/S. If the poor revenue outlook tells us one thing, it's that these current price levels could be unsustainable.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for MasterCraft Boat Holdings that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

In order to justify its P/S ratio, MasterCraft Boat Holdings would need to produce growth that's similar to the industry.

In order to justify its P/S ratio, MasterCraft Boat Holdings would need to produce growth that's similar to the industry.

爲了證明其市銷率,MasterCraft Boat Holdings需要產生與行業相似的增長。

爲了證明其市銷率,MasterCraft Boat Holdings需要產生與行業相似的增長。